The “solar singularity” is the point where solar becomes so cheap in a majority of countries around the world that it is established as the default new power source. This piece is my second annual followup to my original article on the solar singularity from early 2015. My 2016 update is here. (I also made the solar singularity concept the centerpiece of my 2015 book, Solar: Why Our Energy Future Is So Bright.)

As before, I’ll cover not only solar, but also battery storage, electric vehicles and self-driving cars, which together constitute the parallel and intertwined revolutions that are set to transform our energy system worldwide. With these four technologies developing steadily, we can reasonably expect to see, by 2035 to 2040, a world powered predominantly with renewable electricity -- not only homes and businesses, but also transportation and industrial processes.

The short summary of 2017 so far is that we are progressing at an even more rapid pace toward the solar singularity and the related energy revolutions just described than initially expected. Many key goals are being met earlier than anticipated. Some key challenges remain, however, particularly with a new Republican administration that's generally perceived to be very pro-fossil fuel and anti-renewables. But it’s likely that even a highly fossil-fuel oriented White House won’t do much at all to slow down the solar singularity.

How close is the solar singularity?

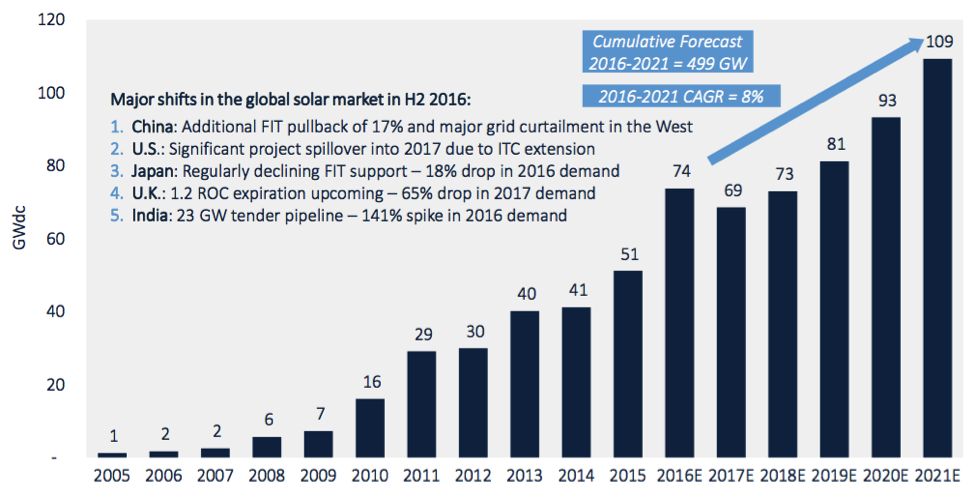

Global solar demand rose a massive 45 percent to 74 gigawatts in 2016, according to a GTM Research estimate. The U.S. was the second-largest market, with a record-breaking 14.6 gigawatts, almost double the 2015 figures. China was, however, far and away the biggest market, with 34.5 gigawatts, more than twice the size of the U.S. market. As a telling comparison: The entire world installed just 30 gigawatts of solar in 2012, a short four years ago.

The world’s installed solar capacity is projected now to be about 700 gigawatts by 2020, with a little more than 300 gigawatts installed at the end of 2016. That 700 gigawatts of solar is enough power to supply about one-third of current U.S. electricity demand. That’s substantial.

FIGURE: Annual Global Solar Demand Projections

Source: GTM Research

In terms of costs, I wrote in last year’s update: “We’re headed to $1/watt as an all-in cost in the next five to 10 years.” Wow, what a difference just a year can make. According to GTM data, utility-scale solar projects recently met the U.S. Department of Energy SunShot Initiative's $1/watt all-in cost goal (minus developer profit of perhaps 10 percent additional cost) three years early! The DOE has not officially met its goal, but it is astounding to be here in early 2017 and looking at all-in costs for new solar plants at near $1/watt. Things can and do indeed change for the better.

At $1/watt, the levelized cost falls to just 5.7 cents per kilowatt-hour, well below cost parity with new natural gas plants, coal plants or nuclear plants. With two-axis trackers (which are becoming increasingly viable) and the best solar resources, increasing the solar capacity factor to as much as 32 percent, the $1/watt all-in cost of power falls to just 4.5 cents per kilowatt-hour.

I wrote in 2016:

Bloomberg New Energy Finance reported this summer that wind power was the cheapest source of power in the U.K. and Germany in 2015, even without subsidies. The article’s tagline is: “It has never made less sense to build fossil fuel power plants.” The same article highlights the positive feedback loop that solar and wind power have on reducing the cost-effectiveness of fossil fuel power plants due to the dispatch order of renewables versus fossil fuel plants.

The 2017 update is that a major new report from Lazard now shows that new solar and wind power projects can supply the lowest-cost electricity in many parts of the world.

The solar singularity is indeed near here in the U.S., and increasingly, around the world. I described previously that 1 percent of the market is halfway to solar ubiquity because 1 percent is halfway between nothing and 100 percent in terms of doublings (seven doublings from .01 percent to 1 percent and seven more from 1 percent to reach 100 percent). The U.S. reached the 1 percent solar milestone in 2016. We’re halfway to ubiquity. Buckle your seatbelts.

I wrote in 2016 with respect to wind power -- a highly complementary technology to solar power because it often produces the most power at night:

My expectation…is that wind power will grow extremely strongly through 2030 due to ongoing improvements in the technology that are making it more geographically viable around the world.

Indeed, wind power continues its path of strong growth, and perhaps the most encouraging news in the wind power sector is that offshore wind power prices have dropped by almost half in the last few years, bringing them into a more competitive range with onshore wind power and other competing power sources. The major benefits of offshore wind are reduced visual impacts compared to onshore turbines and, perhaps most significantly, reduced wildlife impacts and habitat loss, particularly for turbines located far offshore. Cost has always been the issue with offshore wind, so it is very encouraging to see significantly declining cost trends for offshore wind in recent years.

How close is economically viable battery storage?

Battery storage is key to deep penetration of solar power because, of course, solar power is variable and limited to daytime hours. We will eventually need massive amounts of storage (battery-based and other technologies also) to balance variable renewables like solar and wind.

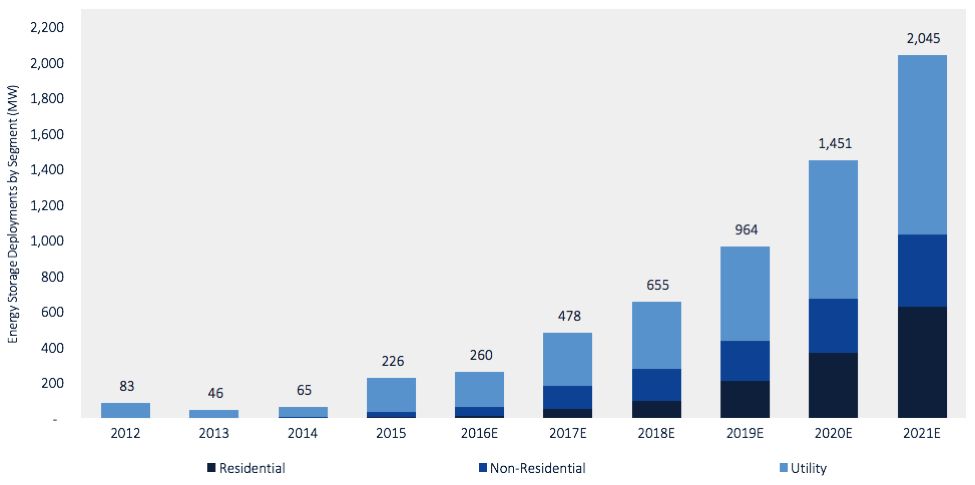

2016 was a good -- but not great -- year for the U.S. energy storage market. We saw over 300 megawatt-hours of storage installed in the U.S., just a little more than what was installed in 2015. According to GTM Research, however, the future looks bright for storage also, with more than 2,000 megawatt-hours to be installed annually by 2021, and utility-scale storage making up the largest sector.

FIGURE: Annual Storage Installations and Projects in the U.S.

Source: GTM Research

We are still low on the energy-storage growth curve, and it is far less clear, when compared to the solar future, that we are on track for singularity-style growth for storage in the coming decade or two.

Globally, the storage market is likely to double in 2016, once the final numbers come in. IHS Energy projected in August that the global market would rise from 1.4 gigawatt-hours installed to 2.9 gigawatt-hours (compared to just 0.3 gigawatt-hours for the U.S. market in 2016). This is far stronger global growth than we’ve seen in the U.S. alone in 2016. The same report projects that the global energy storage market will grow as fast as solar PV has grown in recent years.

In 2015, a detailed report from Lazard found that battery storage could be economically viable in some limited situations (frequency regulation, for example) even without subsidies. The report’s team leader stated that “the energy storage industry appears to be at an inflection point, much like that experienced by the renewable energy industry” a few years ago.

Lazard is kind enough to release its energy storage costs annually, as it does with its levelized cost of electricity reports, so we can track how these costs are changing over time. Looking at one common storage technology, lithium-ion batteries on the transmission system, we see that costs fell from a range of $347 to $739 per kilowatt-hour in 2015 to $267 to $561 per kilowatt-hour in 2016, a decline of about 23 percent (on the lower end of the range) in just one year. That’s real progress.

Worth a mention is Elon Musk’s interesting Twitter pledge and discussion to supply 100 megawatts of Tesla batteries at $250 per kilowatt-hour for South Australia, with deployment guaranteed in just three months' time -- or the batteries will be free! Musk claims that this will be the same transparent pricing for all customers in 2017, marking further cost declines already below the Lazard price range just mentioned.

On the vehicle side, batteries are even cheaper. We have reports from General Motors, for example, that show a cost decline from $750 per kilowatt-hour for electric vehicle batteries five years ago, when GM first started producing the Chevy Volt, to just $145 per kilowatt-hour in 2016. I suspect the stationary storage market will rapidly catch up to the mobile market in terms of cost declines.

It does indeed look like the exponential learning curve improvements are kicking in for storage, and more rapidly than many expected. Storage deployments are still relatively small, but it seems clear that many markets are poised for explosive growth, and this growth will fuel the virtuous cycle of ongoing cost declines.

How soon will electric vehicles be economically viable?

A featured 2016 Bloomberg article highlighted the potential for electric vehicles to usher in the next oil crisis: “A shift is underway that will lead to widespread adoption of EVs in the next decade,” it states. The article adds: “Battery prices fell 35 percent [in 2015] and are on a trajectory to make unsubsidized electric vehicles as affordable as their gasoline counterparts in the next six years, according to a new analysis of the electric-vehicle market by Bloomberg New Energy Finance. That will be the start of a real mass-market liftoff for electric cars.”

Big changes are afoot in the transportation sector, as they are in the electricity sector.

An important driver for EV adoption is the ongoing reduction in vehicle battery costs, which have been falling faster than expected also, as mentioned above. One expert wrote in a recent article: “Back in 2010, the Department of Energy set a cost goal of $125 per kilowatt-hour for an EV battery pack by 2022, because that would make electric-propulsion systems equal to the cost of an internal-combustion engine. In addition to individual cells, the battery pack also includes the supporting structure, cooling mechanisms, and battery management systems.”

We know that GM is claiming costs of just $145 per kilowatt-hour already, down from $750 per kilowatt-hour not long ago. It seems that at this decline curve, we’ll see $100 per kilowatt-hour soon and then $80 per kilowatt-hour not long after. The $80 price brings EVs well below the threshold price needed for mass-market adoption, all else being equal.

The Chevy Bolt, with a stellar 238 miles of range and a cost of only $35,000 before tax credits and rebates, went on sale in late 2016, but it is selling poorly. Over 1,100 units were sold in January, which is considered a strong start. But sales dropped in February, and some dealers are already offering steep discounts. By all accounts it’s a great car -- indeed, it was named Motor Trend’s Car of the Year. But it still suffers from a perceived lack of appeal. That honor falls to Tesla’s Model 3, which is slated for production earlier than originally proposed -- initial production is now set for about mid-year, with 5,000 Teslas set to roll off of the assembly line each week by the end of 2017, and twice that in 2018.

Will affordable long-range EVs allow the EV market to truly take off? GTM's parent company Wood Mackenzie forecasts that won't happen in Europe until after 2025. So time will tell, but the fact that the long-awaited generation of affordable and long-range EVs is either here now or about to be here is very exciting. And the roughly 400,000 Model 3 reservation holders will look forward to receiving their vehicles in the next two years.

If Tesla’s production of the Model 3 goes smoothly, and if the car is actually as solid as it appears to be, it seems likely that we’ll see EV sales ramp up strongly in the next few years. And it won’t just be Tesla and Chevy selling these cars. It will involve many other manufacturers, old and new, who smell serious opportunity in this massive new sales niche.

So this category is still a “we’ll have to wait and see a bit longer” in terms of progress toward a singularity-like takeoff. The Trump administration’s recent announcement that they will revisit the 2022-2025 CAFE standards that Obama’s EPA set will not help EV sales. But nor is it likely to do much to slow them down.

How close are self-driving cars?

Tesla is again the biggest newsmaker in the area of self-driving cars, announcing last October that full self-driving (FSD) hardware will be included in all new Teslas and that FSD software will be coming “very soon.” A robust discussion about how and when FSD will actually arrive can be found here at Tesla’s forum.

Many other companies are ramping up their autonomous driving efforts, including Uber, GM, Lyft and a ton of others. It’s also too soon to say how quickly self-driving cars will arrive and how quickly they will become widespread. There are indications FSD vehicles could be on the road as soon as 2021. My best estimate, however, is that we’ll see self-driving cars rapidly become ubiquitous in the 2025-2035 timeframe.

The Trump administration monkey wrench

It’s still too early to say how the Trump administration will affect the new energy economy. It is very apparent that this administration is pro-coal and pro-oil and gas, but it is not as apparent how it will treat existing or new incentives for renewables. The new administration has already announced or is set to announce massive changes to Obama’s climate legacy. But as bad as those changes will be symbolically and in terms of setting back international leadership on climate-change mitigation, I’m not convinced at this point that these changes from the White House will do much, if anything, to slow down the various energy revolutions described in this piece.

My feeling is that Trump’s political strategy is generally to make a calculation about the level of passion on any particular issue and to weigh in strongly on the side where he sees the most passion. Since his constituency is focused mostly in the Rust Belt and the South, it is no surprise that he sees the most passion in reviving the fossil fuel industry, which, as with the coal industry, has been increasingly hurting in recent years. Trump has pledged to revive the industry, but it may not be revivable.

At the same time, it's clear that Trump very supportive of keeping or creating jobs here in the U.S. Companies like Tesla and SpaceX, which have created thousands of new energy economy jobs in the U.S., may sway Trump’s generally old-school perspective. He may “see the light” in terms of how many American jobs can be created or maintained in the new energy economy and act accordingly. Or, at least, maybe he will not do anything to harm those jobs, such as prematurely killing off the federal Production Tax Credit and Investment Tax Credit for wind and solar, respectively.

The future is indeed -- still -- bright, particularly for solar, wind and storage. We’re still not over the hump yet for EVs and self-driving cars, but we should gain far more clarity on these related energy revolutions in the next year or two.

***

Tam Hunt is a lawyer and owner of Community Renewable Solutions LLC, a renewable energy project development and policy advocacy firm based in Santa Barbara, California and Hilo, Hawaii, co-founder of Solar Trains LLC, and author of the book, Solar: Why Our Energy Future Is So Bright.

Correction: This story was updated to reflect that the Department of Energy has not officially announced meeting the SunShot Initiative goal of $1/watt of solar PV.

41

41

15

15

9

9