Energy efficiency professionals are increasingly looking to the success of third-party financing in the solar industry as a model for attracting large investors and growing deal flow quickly. Is it working?

If a new survey of hundreds of project developers is any indication, the efficiency industry still hasn't found the same financing momentum that carried the solar PV industry.

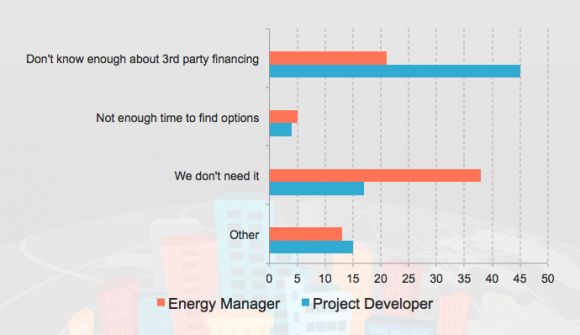

In an update to a survey from last year, Noesis Energy released its latest findings about what is holding back efficiency project development in the U.S. Unsurprisingly, one of the chief factors is a lack of financing options -- or a lack of knowledge about those options.

Among both internal energy managers and outside developers, Noesis found that two-thirds of all projects fail because of a lack of funds. That's a third-party financing problem, argues Noesis.

"It’s still one of the main reasons why projects don't get done. Over the next couple of years, those numbers have to get better," said Noesis CEO Scott Harmon.

Nearly half of the energy managers surveyed said they never include third-party financing in their proposals. Three-quarters of independent developers said they only rarely include those options or never include them at all. Why is that the case?

Energy managers funding projects internally on a balance sheet may not need them. But developers pitching projects to customers simply aren't educated about what's out there, as the results shown in the chart below indicate.

This is the reason why Noesis itself has shifted from a software-centric company tracking building energy performance to a financing provider that uses software to close deals. Over the last fifteen months, the company has built relationships with financiers and closed a $30 million fund to support efficiency projects through shared savings agreements. The company is also targeting equipment leases for small retrofit projects in commercial and industrial buildings.

"Our model has basically inverted. The software is there to accelerate the financing we have," said Harmon. "It's a much bigger market and revenue opportunity."

Another intelligent efficiency company, SCIenergy, is making a similar shift in an attempt to leverage its analytical software to close managed energy services agreements (MESAs), an emerging third-party model in the commercial sector.

But as these latest survey results clearly show, that opportunity hasn't fully materialized yet. Despite a lot of talk about creating third-party models and a small surge in activity, the efficiency industry is still many steps behind solar.

A lack of education in the market, an overly complicated closing process and distrust of the claimed savings are the three big obstacles preventing a surge in deal flow. Harmon said that lenders are actually seeking out Noesis for funding opportunities, but project developers aren't comfortable describing new financing arrangements to customers.

"These numbers have to get better," said Harmon. "We really need to see some of these indicators start to move."

However, based on current activity in the industry, some experts believe those numbers are ready to move. New funds for efficiency worth hundreds of millions of dollars are drawing in large investors; the state-level policy environment for efficiency is helping a handful of third-party financing models creep across the country; new underwriting standards in the works may help streamline financing; and deal volume is getting big enough to finally enable the securitization of projects.

"We seem to be making progress," said Brad Copithorne, a financial policy director at the Environmental Defense Fund. "I'm cautiously optimistic."

There are around a half dozen promising third-party financing models emerging in the U.S. They can be roughly separated into two categories: market enablers and project-level structures.

The market enablers include property-assessed clean energy (PACE) and on-bill repayment (OBR), which allow efficiency projects to be financed through property taxes or utility bills and are implemented through a policymaking process. Both structures have faced difficulties in implementation due to opposition from housing lenders and debates around program design, but they continue to spread.

Project-level structures include equipment leases, shared savings, MESAs and the metered energy efficiency transaction structure (MEETS). These structures build on the energy savings performance contracts traditionally delivered by energy service companies in the public sector. But they are only now making an impact in the private sector as companies develop better software to prove savings and attract more banks willing to back the projects.

According to Copithorne, advocates working on PACE and OBR programs want them to accommodate these different third-party financing options. There are currently no PACE programs that allow all those structures to qualify, but Hawaii may become the first state to do so in the commercial market. California and Connecticut are also considering similar allowances.

"In a perfect world, those platforms would be available for a wide variety of financing options. But we're not there yet," said Copithorne.

As more PACE and OBR programs allow different third-party structures to participate, "it's going to make a lot more projects pencil out," he said.

For now, no efficiency companies outside the ESCO market have created a scalable third-party model like SunEdison or SolarCity have done in solar.

"We've lacked a market infrastructure to connect the dots," said Pier LaFarge, the CEO of SparkFund, a crowd investment platform for efficiency. Those "dots" include policies that enable third-party financing, software tools that can quickly originate deals and accurately prove savings, and an industry capable of talking about finance.

"Solar has already put that infrastructure in place, and efficiency is just in the early stages of doing that," said LaFarge.

The enabling factors are indeed starting to align. It is unclear whether there will be a dominant financing structure -- for example, will the MEETS beat out the MESA? -- but the diversity of real estate and policies around the country will create room for all kinds of models to succeed.

"There are lots of differences in approach, but we are seeing new transactions get executed," said Copithorne. "I don't know for sure what the exact financing solution is, but we seem to be making progress."

41

41

15

15

9

9