Editor's note: This story previously only mentioned Suniva as a petitioner in the trade case. We added SolarWorld, which is a co-petitioner. Both parties are referenced in the actual research report. Also, since publication of this article, Suniva has clarified that its intent for the interaction of the minimum price and import tariff would be inclusive, rather than additive. Thus, our $0.78/W minimum price modeled scenario best represents Suniva's intended requested remedy.

Suniva's and SolarWorld's new trade dispute would strike a devastating blow to the U.S. solar market, erasing two-thirds of installations expected to come on-line over the next five years.

If the petition is successful, shockwaves will be felt across all segments of U.S. solar. Utility-scale solar is most at risk, with more than 20 gigawatts already at risk of cancellation if module prices fall back to 2012 levels.

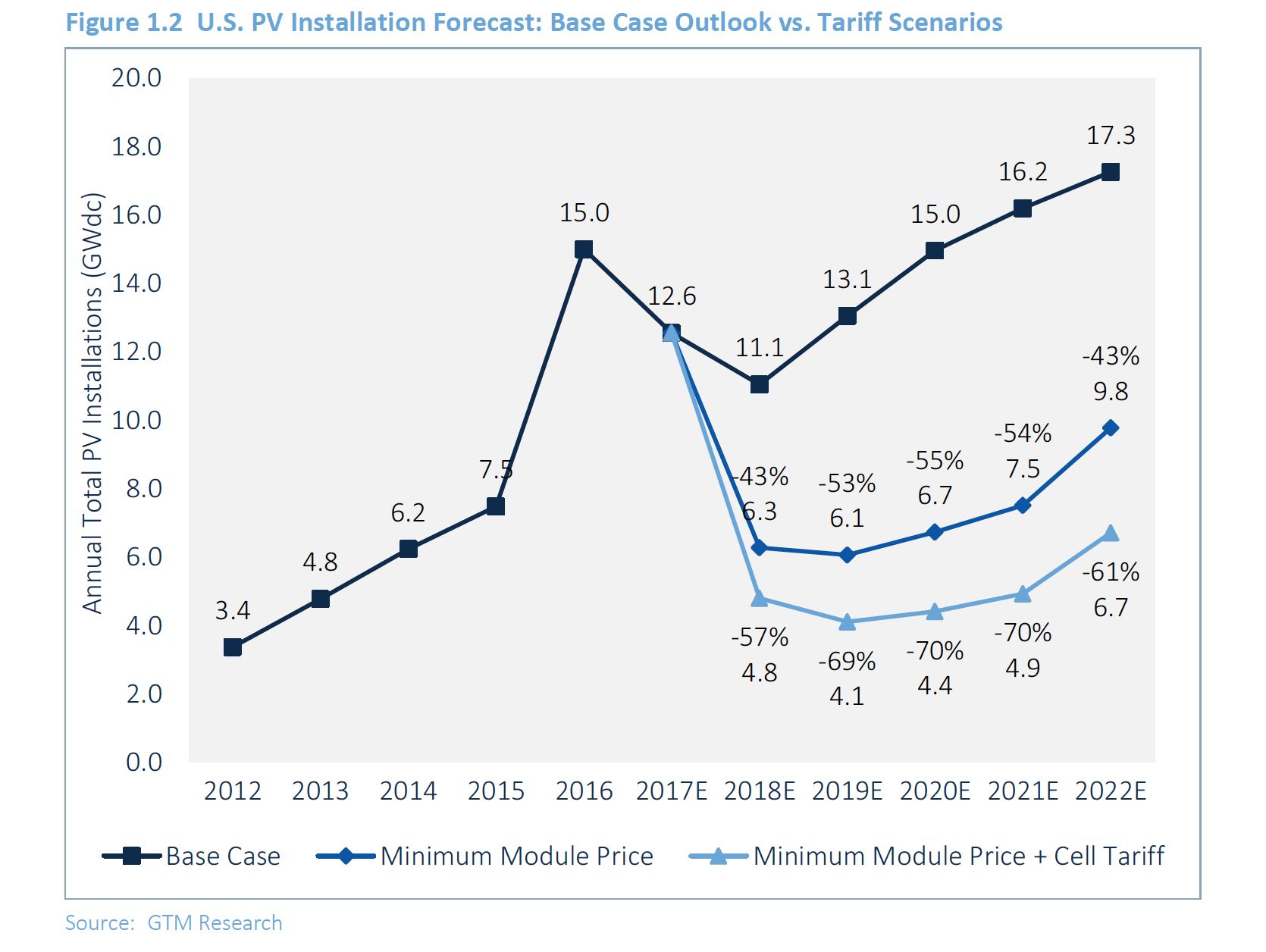

GTM Research crunched the numbers based on Suniva's and SolarWorld's requested penalties for imported solar equipment ($0.40/watt tariff for cells and a floor price of $0.78/watt on modules) and found that they would cause unprecedented demand destruction.

Source: GTM Research's U.S. Solar Outlook Under Section 201

If Suniva's and SolarWorld's proposal is approved by the U.S. International Trade Commission and President Trump, there will be a new minimum price on imported crystalline silicon solar modules and a new tariff on imported cells. Put together, the U.S. could miss out on more than 47 gigawatts of solar installations. That's more than what the U.S. solar market has brought on-line to date.

In our latest report, we found that between 2018 and 2022, total U.S. solar installations would fall from 72.5 gigawatts cumulatively to just 36.4 gigawatts under a $0.78 per watt minimum module price scenario. Even more dramatic, with a $1.18 per watt minimum price, representing a $0.40 per watt cell tariff on top of a $0.78 per watt minimum module price, cumulative installations would plummet to 25 gigawatts.

Source: GTM Research's U.S. Solar Outlook Under Section 201

The utility-scale PV segment is expected to see the largest downward revisions to its base-case forecast.

A majority of utility PV procurement now hinges on solar being cost-competitive with natural gas alternatives, with nearly three-fourths of the utility PV pipeline procured outside renewable portfolio standards. Under both tariff scenarios, most of that pipeline is at risk of cancellation unless PPA prices are renegotiated. That could wipe out a number of state markets altogether under either tariff scenario.

Residential PV is the least sensitive segment to the introduction of tariffs. On one hand, the number of residential state markets at grid parity would fall from 43 to 35 under the minimum module price only scenario (and from 43 to 26 with the cell tariff added to the minimum module price). However, on the other hand, the top six state markets, which drive a majority of the base-case outlook, would continue to offer more than 10 percent annual net savings.

Over the next several years, residential PV can still rely on California and the major Northeast state markets to remain above the tipping point under both tariff scenarios.

Meanwhile, the non-residential PV segment is likely to be more sensitive to new tariffs than residential PV, given that 40 to 50 percent of the base-case outlook depends on large C&I customers with challenging rate structures, plus the nascent community solar segment riddled with project development and financing risks.

Uncertainty looms over the U.S. solar market and the trade dispute itself. Our latest report outlines how the trade case might or might not come to fruition, and if it does, how it will impact each market segment through 2022.

The full report is available to GTM Research solar subscribers or for purchase here.

Trying to understand the Suniva and SolarWorld trade case? We break it down in a recent episode of The Interchange podcast.

41

41

15

15

9

9