Off-grid energy, long the focus of nonprofits and governments, is becoming the next massive investment opportunity for the world’s biggest energy players, with hundreds of millions of dollars going into solar home systems and other energy solutions for the billions of people who lack access to reliable grid power, or any power at all.

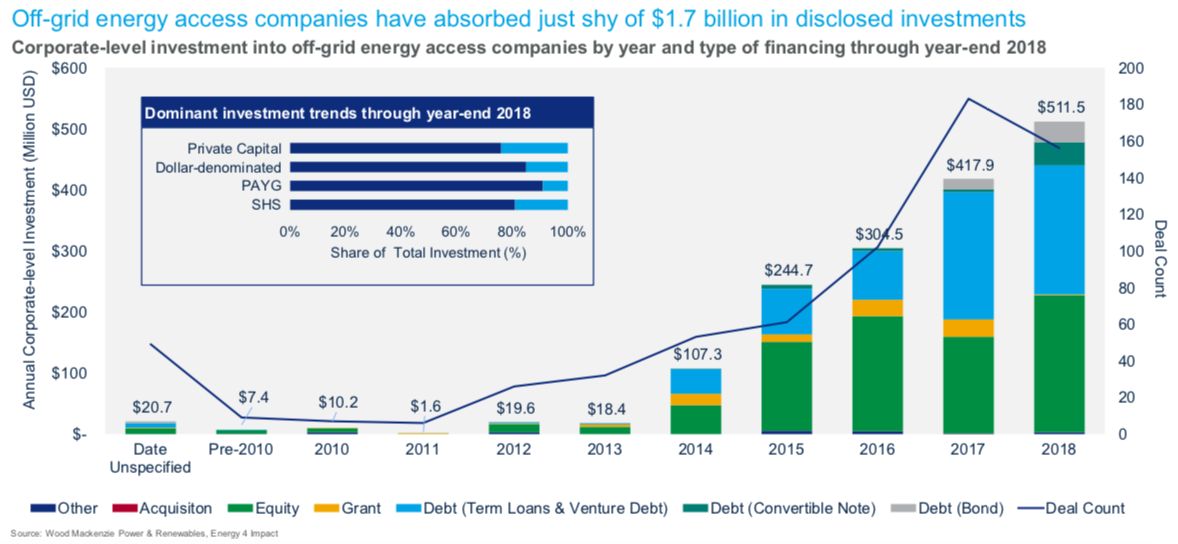

That’s the conclusion of a new report from Wood Mackenzie Power & Renewables and Energy4Impact, detailing the spectacular rise in investment in the off-grid energy access sector. From nearly nothing prior to 2010, spending on the category — which includes businesses that sell solar panels to power lights, cellphones and other household devices, up to microgrids that power entire communities — rose to a total of nearly $1.7 billion at the end of 2018.

More than $1.2 billion of that was invested since 2016. In 2018, annual investment in the sector broke the $500 million mark.

The biggest investments in this sector have occurred over the past two years, and the nature of these investments indicate that the sector, while still in a nascent and uncertain phase of development, is also entering a new stage of maturity, the report noted.

Year-on-year transaction volume grew 37 percent from 2016 to 2017, and total capital composition by volume shifted to over 50 percent debt, indicating a willingness on the part of investors to scale up. In 2018, total transaction volumes grew another 22 percent, average equity investments doubled, and debt increased more than fivefold compared to the previous year.

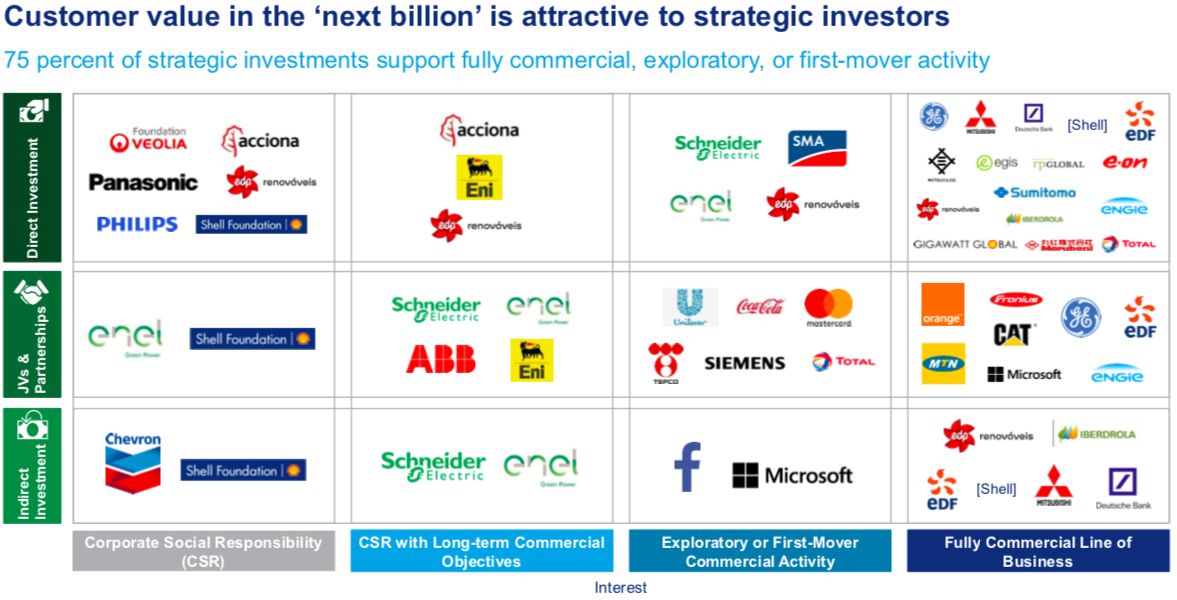

What’s more, the share of strategic investment in the sector is on the rise — from oil and gas majors like Shell and Total, European utilities like Engie and EDF, and energy technology providers like Schneider Electric, to name some of the big names.

At the end of 2018, the report tallied $383 million spent on more than 110 direct strategic investments in off-grid energy. Investments range from outright acquisitions such as Engie’s purchase of Fenix International, to equity and debt financing for solar home or microgrid developers. An additional $461 million in strategic funding has reached the sector via indirect fund investments.

And while roughly 25 percent of this corporate funding has come through corporate social responsibility initiatives and other sources not tied to the underlying business, the remaining 75 percent is commercial in nature, Ben Attia, Wood Mackenzie Power & Renewables analyst and lead author of the report, noted.

“There are a billion customers that have no access to electricity, and another billion that have access to unreliable electricity,” he said, citing data from sources including the World Bank and the International Monetary Fund. Companies that can serve them “have the opportunity to own the next billion customer relationships — and that includes all their evolving needs and all their data.”

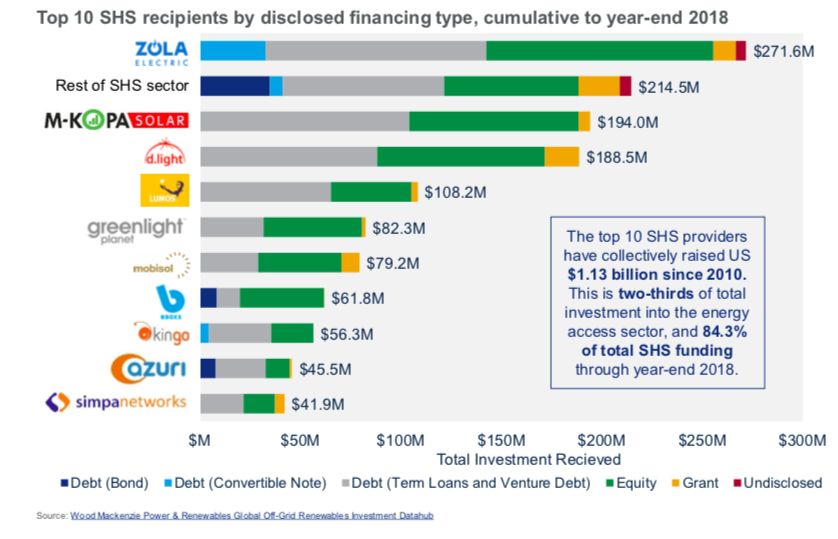

While the term “off-grid energy access” covers a wide variety of business models, more than 80 percent has gone into off-grid solar home systems providers, Attia noted. These companies may be unfamiliar to observers of the U.S. or European solar landscape, but they have raised significant sums to bring pay-as-you-go solar offerings to hundreds of thousands of customers without electricity.

Overall, the solar home system market has raised more than $1.1 billion through 2018. Some of the biggest, in terms of capital raised through the end of 2018, include Zola Electric (formerly Off Grid Electric) with $261 million, M-Kopa Solar with $194 million, D.Light with $188.5 million, Lumos with $108 million, Greenlight Planet with $82 million, and Mobisol with $79 million.

Of the companies in this sector, more than 90 percent are using a pay-as-you-go model, built on the same mobile device payment infrastructure that’s enabling all manner of e-commerce in countries where cellphone networks have far outpaced traditional communications infrastructure. These lease-to-own models offer far more affordable customer entry than cash sales, and allow companies to make money on financing as well. But they also require companies to carry that consumer debt on their balance sheets, and seek regular injections of working capital to cover the associated costs.

But the long-term relationship of a pay-as-you-go model could allow these companies to build “value-stacking” on top of the core solar proposition, Attia said. It’s a simple proposition: Once a household has electricity, it’s going to want all of the products and services that come with it, and the companies doing off-grid solar home systems see themselves as the natural provider of them.

“Households don’t demand kilowatt-hours — they demand the ability to turn the lights on, or have a fan, or a radio, or a TV, or Wi-Fi in their house,” he said.

Attia also pointed out that the concentration of investment among energy access companies, many of them competing in the same markets, presents short-term risks for the parties involved. Concentration is apparent in several ways. For instance, the report finds that the top 10 deals represent $564 million, or one-third of total investment to date.

There's also geographic concentration. Of the regions covered by the report, Africa drew nearly 80 percent of the total capital raised, compared to about 15 percent for India and Southeast Asia and about 5 percent in Latin America. These low showings are largely due to the presence of large-scale public programs that limit the market for private off-grid solutions, compared to Africa, where the ubiquity of “mobile money” payment systems has allowed private-sector players to compete more effectively.

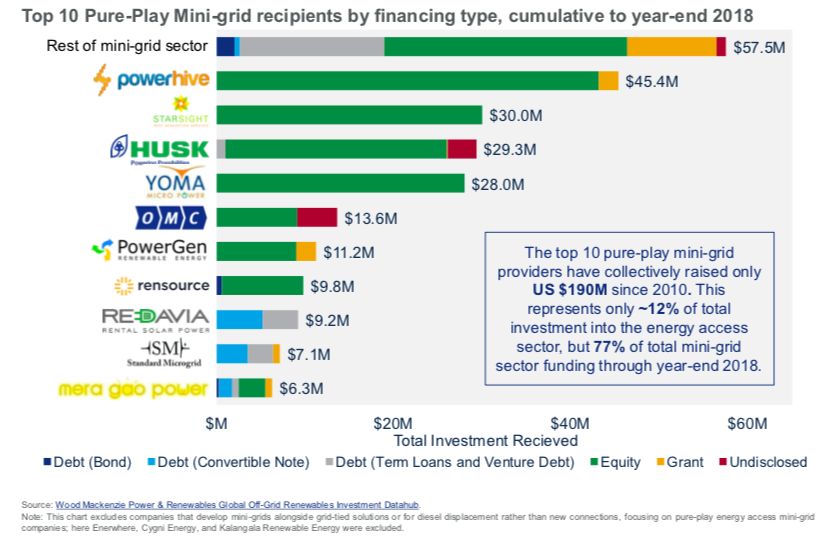

Wood Mackenzie’s report also tracks investment in the so-called “mini-grid” sector — a category meant to differentiate the smaller-scale projects involved from the broader world of “microgrids,” which can include big industrial, commercial and government facilities. The report tracked $190 million raised through the end of 2018 in the top 10 mini-grid companies, including $45 million for Powerhive, $30 million for Starsight, $29 million for Husk, and $28 million for Yoma Micro Power.

In another sign of capital concentration, the top 10 pure-play mini-grid providers have raised 77 percent of total mini-grid funding through year-end 2018.

"This represents an outsized risk to the sector as it may cause heightened investor caution, particularly given the shortage of successful exits to date," Attia wrote in a recent LinkedIn post.

41

41

15

15

9

9