The forecast is for methane.

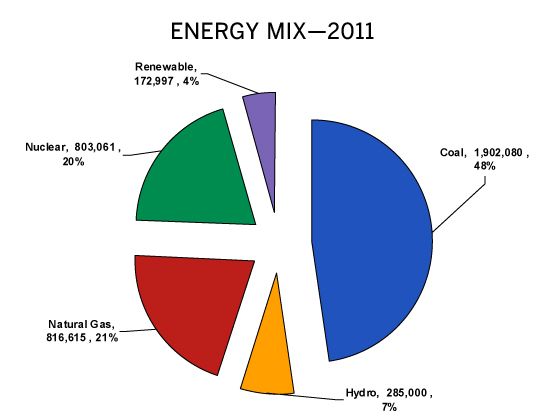

By 2035, natural gas turbines will be the largest source of electrical power in the U.S., jumping from 21 percent today to 40 percent, according to the year-end energy market forecast from Black & Veatch. Coal, meanwhile, will dip from around 48 percent to 22 percent as many older plants get retired, while nuclear will stay flat at around 21 percent.

"We are looking at a world over time that is switching to natural gas," said Mark Griffith, director of energy market perspective at the firm, in an interview. (Griffith also has a webinar on the subject here.)

Although natural gas is the big winner, new renewables like solar, wind and geothermal will see a jump as well, rising from four percent of the mix today to 11 percent by 2035.

If large-scale hydroelectric is added to the mix, the contributions to the U.S. electricity diet from all renewables will rise from 11 percent today to 17 percent of the total, or close to the levels of both coal and nuclear. Yes, renewables are in fourth place, but in the case of hydro, not by much.

During this same period, the installed capacity of new renewables will rise form 50 gigawatts today to around 175 gigawatts. Capacity increases faster than "market share" for renewables in this period because the U.S. annual energy diet will on average grow by 2.6 percent a year over the 2010-2035 period.

The outlook is the result of a variety of factors. Technology allowing fossil fuel companies to access shale gas deposits, combined with a proposed pipeline in Alaska that should kick into gear in the next decade, could keep the price of gas under the $8 per million BTU level through 2030. (It currently sells for a bit over $4 per million BTU, according to data from the firm.) Commodity prices always fluctuate, but rising supply could balance out rising demand to keep prices relatively calm over the next two decades. The Marcellus shale deposit that straddles the U.S.-Canadian border produced 200 million cubic feet a day in July 2008. Two years later, 1.4 billion cubic feet a day were being pumped out. Gulf Coast shale deposits will generate 15 billion cubic feet a day in 2030.

Capital costs for combined cycle plants are also comparatively inexpensive, hovering in the low $1,000-ish-per-kilowatt range.

Black & Veatch assumes that the U.S. will pass carbon regulations in 2016, but this too can help gas, at least when it comes to taking market share from coal. Coal plants in a carbon regime would likely need carbon sequestration, a relatively untested technology that carries a price tag.

"Economics is driving a move toward natural gas and away from coal," he said. "Natural gas as a fuel looks much more attractive."

The looming danger sign for gas may be in water regulations. Water issues could add 50 cents or more of additional cost per million cubic feet of gas. Election cycles can also make forecasts difficult. Last year, Black & Veach assumed that carbon regulations would arrive in 2014, but the recent election results prompted them to add two years to the forecast. The regulatory process could move forward before that date, but that would be an optimistic outlook. At this pace, the U.S. may not hit its carbon target (80 percent of 2005 levels) until 2070 instead of 2050, as was previously assumed.

The big problem for coal is in emissions regulations, as well as the anticipated implementation of carbon taxes. (Disclosure: yeah!) Over the next decade, 52 gigawatts' worth of existing coal plants could be retired, representing a sizeable 16 percent of the U.S. coal fleet, because the cost of retrofitting them to meet new emissions requirements will outweigh the benefits. Financial institutions, meanwhile, continue to remain skeptical about funding new coal plants. Carbon capture intrigues them as a concept, Griffith added, but few, if any, are showing interest in funding commercial carbon capture plants. (By contrast, EPRI is more optimistic about carbon capture.)

"It is not business as usual," he said, nonetheless adding that states in the coal belt will push for the commodity.

For wind and solar, cost will remain the Achilles' heel. "Wind costs aren't coming down any more," he said. Wind facilities cost around $2,000 a kilowatt but power is highly intermittent. If gas goes up to $8 and carbon regulations are passed, "wind would become more competitive," he said.

Solar, which costs more than wind, will remain challenged without feed-in tariffs or tax credits, he said, even if carbon regulations pass. (Second disclosure: solar advocates like to point to the rapid declines in the costs of panels and electronics and argue that the continuation of these trends will allow solar to become competitive without subsidies.)

Nuclear isn't standing still. It will just look like it is. Capacity could increase from 100 gigawatts to 140 gigawatts. Planning, cost, permitting, and financing are still big unknowns, however.

41

41

15

15

9

9