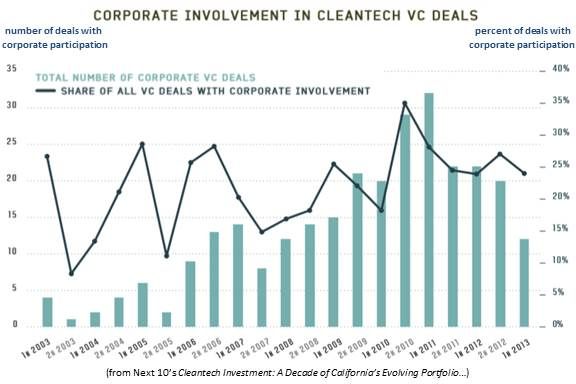

“Of the $2.6 billion of cleantech venture capital investment in 2012 in California, $1.45 billion included corporate investors,” according to Cleantech Investment: A Decade of California’s Evolving Portfolio, a survey of California greentech investing between 2003 and 2013 from Next 10, an independent California greentech advocate. That corporate portion was 56 percent of 2012 VC investment.

“Recent trends show that while early-stage venture capital ebbed after a surge in experimentation, later-stage investments have increased in the last five years.” Corporate money has been focused on those later-stage investments. (This is a topic that was extensively addressed at GTM's recent NextWave Greentech Investing event.)

In 2010, corporate participation in VC investment was only $1.28 billion of the $3.2 billion total, or 40 percent. In 2008, corporations put up $1 billion of the $3.47 billion VC investment, 29 percent. In 2005, it was $100 million of $520 million, only 19 percent.

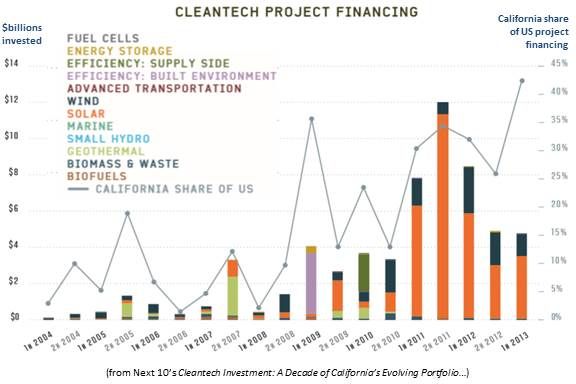

Greentech “development and growth” investment fell 44 percent from H2 2012 to 1H 2013, from $1.5 billion to $870 million, as investors fled greentech. But later stage project deployment financing, according to the report, fell only 3 percent, from $4.9 billion to $4.8 billion, in the same period. The study defines “deployment and growth” as any direct investment in companies that helps scale and commercialize greentech, according to report author Renae Steichen of Collaborative Economics. “Deployment” is project financing aimed at implementing technologies.

Early on, “deployment and growth” investing was more dominant, and it was undertaken more frequently by VCs because of their higher tolerance for risk, explained Next 10 President Noel Perry. With the maturity of the technologies, corporations have begun to participate.

The entry of more corporate, bank, and institutional money helped hold deployment financing steady in the last year. VCs, probably because of their familiarity with innovation, were the steadiest investors in “development and growth,” which dropped only 22 percent, falling from $870 million to $680 million.

VCs highlighted in the report as leaders both in the ten-year trend and the recent shift include Kleiner Perkins Caufield & Byers, Khosla Ventures, VantagePoint Capital Partners, Draper Fisher Jurvetson, Silver Lake, DBL Investors, The Westly Group, and CalCEF.

As factors including California’s AB 32 climate change law, its 33 percent Renewables Standard, and its pro-greentech policies drove demand for renewable energy and energy efficiency, corporate investors like Google Ventures, Intel Capital, General Electric, Siemens Venture Capital, Waste Management, BMW i Ventures, Toyota and Aster Capital have shifted their emphasis, Next 10 reports.

There is a dramatic shift from greentech “development and growth” investment to “deployment” investment. For 1H 2013, “development and growth” investment was $870 million, three times 1H 2003’s $280 million. But “deployment” investment went from $250 million in 1H 2004 to nearly $4.8 billion in 1H 2013.

Innovations in financing just being developed, including real estate investment trusts, master limited partnerships, crowd investing, and securitization are expected to bring in more marketplace money and drive California’s greentech sector further forward, the Next 10 report concludes.

41

41

15

15

9

9