As many of our readers know, Greentech Media’s sixth annual Solar Summit will be held this year on April 22-24 in Phoenix, Arizona. One of the highlights of the conference in recent years has been the debate session, a 30-minute back-and-forth discussion on a question or theme that is particularly controversial or divisive. In previous years, topics have ranged from the relative usefulness of centralized versus distributed solar, whether crystalline silicon technology can drive grid-parity economics, and the impact of import tariffs in the U.S. market.

This year, Martin Hermann from 8minutenergy and Conrad Burke from DuPont Innovalight will face off to settle the heated issue of whether or not modules are a commodity. It is a question that has been fiercely contested since 2008, when China began to upstage “high-tech” regions such as Germany and Japan as the leading PV module-producing region. Almost half a decade later, the dust has yet to settle. Predictably, the answer depends on who you ask: those on the supply side of the value chain (equipment, material and component suppliers) argue that product performance and reliability vary widely across producers, while many developers and financiers see crystalline silicon modules at least as plug-and-play goods, with brand and bankability taking a back seat to price in determining vendor selection.

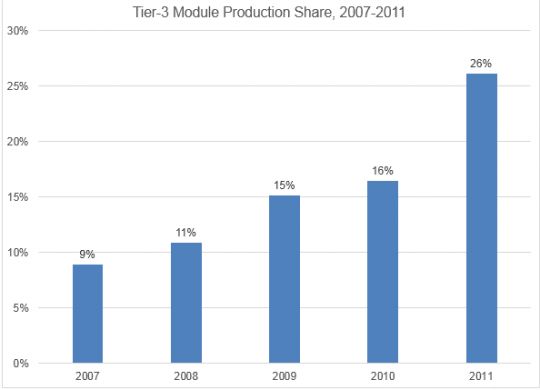

What does the data tell us about the market’s perception? On one hand, the rapid gains in market share of relatively unknown (mostly Chinese) module manufacturers at the expense of established European and Japanese suppliers in recent years certainly attest to increasing commoditization. As shown by the chart below, the production share of what GTM would classify as non-brand-name suppliers (admittedly a subjective determination) has increased from just 9 percent in 2007 to 26 percent in 2011.

Source: GTM Research Competitive Intelligence Tracker

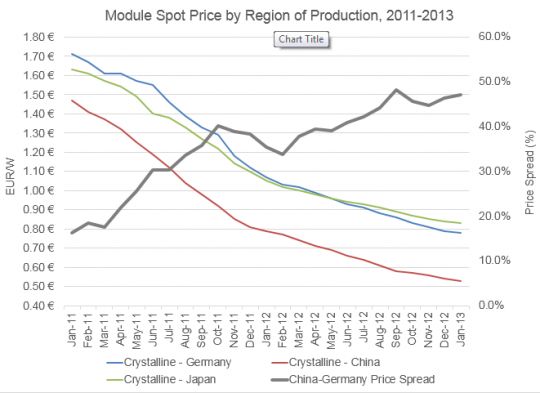

What about pricing data? Historically, Japanese and European-made modules have enjoyed a 15 percent to 20 percent price premium over Chinese-made modules. With increasing commoditization, one would also expect price differentials between brand-name and lesser-known modules to contract over time.

However, the data points in the exact opposite direction. As seen in the graph below, SolarServer’s monthly module price index shows that the price premium between German and Chinese-made modules has increased steadily over the past two years, from 16 percent in January 2011 to 47 percent in January 2013. And two weeks ago, a large EPC on the East Coast informed GTM Research that modules from a large U.S./European module vendor were quoted at $0.89/W versus $0.55/W for tier-1 Chinese modules for Q2 delivery -- a premium of 61 percent. For modules with similar power rating and efficiency, this is an astonishing disparity. It is almost as if the two firms are selling completely different products.

Source: SolarServer/pvXchange

How do we make sense of this? In all likelihood, a key driver is costs: the regional manufacturing cost gap between China and Europe/Japan has continued to expand to the point where being even somewhat price-competitive is simply not feasible (as this article points out, the same is not true of manufacturers in the rest of Asia, where the cost gap with China has actually diminished).

As a consequence, Western and Japanese vendors have effectively ceded that segment of the market that is even the slightest bit price-sensitive to the Chinese, and are for most part no longer competing with Chinese vendors for the same customers. At the same time, there remains a segment that still views modules as a relatively high-tech good where materials selection and process flow play a large role in influencing performance, and that values quality, brand and bankability (although it is debatable, given their financial troubles, how bankable leading European pure-play manufacturers such as Isofoton and SolarWorld are today). The Japanese residential market, which shows a strong preference for domestic brands despite their relatively high cost, is an example of this; the rapid growth of the FIT-fueled Japanese market in 2012 has been a welcome source of relief for domestic producers such as Sharp and Solar Frontier.

For European and U.S. firms, however, the piece of the demand pie that does not view modules as a commodity has at best flattened, and at worst has contracted, especially as FIT reductions in Western Europe have forced once brand and quality-sensitive installers and developers to become increasingly price-sensitive. The only sustainable path forward for these firms, in my mind, is to differentiate heavily on the product or business-model front. As it stands, these firms are in the position of hoping that a few well-publicized recalls might lead the market to becoming more aware of quality differences across suppliers. The problem with this point of view, to paraphrase John Maynard Keynes, is that the solar market can stay irrational longer than producers can stay solvent.

Greentech Media's sixth annual Solar Summit will be held from April 22-24 in Phoenix. For more information, click here.

Update: Watch the debate at Solar Summit

41

41

15

15

9

9