Texas is an interesting market for distributed energy resources (DERs) like solar PV, energy storage and demand response -- with the word “interesting” having positive and negative connotations in this context.

On the positive side, the state’s competitive energy market may make it a Wild West of opportunity and innovation for distributed energy like rooftop solar, behind-the-meter batteries and flexible demand. But on the negative side, Texas is also a center of the fossil fuel industry, which holds a lot of sway over how DERs can, or can’t, find their way into grid markets.

For evidence of this, just check out some of the recent action at the state’s grid operator, the Electric Reliability Council of Texas, or ERCOT. In the past two months, we’ve seen significant action on two big initiatives aimed at bringing distributed energy into the state’s fast-acting grid resources markets -- and neither of them have been particularly positive for the renewable energy crowd.

The first, dubbed the Future Ancillary Services Team, or FAST, initiative, sought to re-engineer the state’s antiquated system for fast-responding grid services, in ways that could open up opportunities for batteries and demand-side resources. But after years of being blocked by generators in ERCOT’s stakeholder voting committees, the FAST effort was voted down for the last time in May, forcing its backers to return to the table with alternative plans.

The second, dubbed the Distributed Resource Energy and Ancillaries Market, or DREAM, is still rolling along -- but not in quite the form that some thought it would. Launched last year, the DREAM effort put together a task force to hash out how DERs might be aggregated as resources available to ERCOT’s energy markets, similar to initiatives underway in California and New York.

When the DREAM task force disbanded in May, many market observers worried that it meant the end of the effort. Instead, it marked the start of a new phase of development, in which market participants could start proposing actual ERCOT rule changes.

But as with any change to Texas’ energy market, these proposals will have to gain the support of stakeholders, including the representatives of the major power generation companies, in order to succeed.

These factors have guided the development of the first proposal coming out of the DREAM initiative -- a relatively limited proposal, aimed more toward enabling energy market participation by backup generators at facilities the state’s hurricane-vulnerable Gulf Coast, and less at creating a new class of energy resources from aggregated DERs.

At Greentech Media’s Grid Edge World Forum conference last month in San Jose, we heard our fair share of complaints about these ERCOT developments from solar and energy storage players and environmental groups. At the same time, however, they may well be the best bet for distributed renewable energy resources to gain a foothold in the Texas market, given the resistance that the generators have offered to more aggressive proposals.

Moving the DREAM forward in ‘baby steps’ toward DERs in energy markets

Back in May, we talked to Chad Blevins, a senior consultant with Austin, Texas-based law firm The Butler Firm and chair of ERCOT’s Emerging Technologies Working Group. He’s also one of the members of the DREAM task force, the group that refined the broad set of concepts around distributed energy as grid market players in preparation for the next step of turning them into real-world rule changes.

That’s done through something called a nodal protocol revision request, or NPRR -- and there have been several NPRRs related to DREAM submitted so far this year. Those include one, NPRR 751, which would have changed the definition of distributed generation in ways that would have supported aggregated DERs, which was recently rejected by an ERCOT committee -- a fact that caused some industry observers to worry that the DREAM effort had come to an end.

But that NPRR “was put forward as a placeholder, to get definitional work done,” and withdrawn without expectation of being passed, Blevins explained in a July interview.

Instead, “We decided to take a different path forward,” he said, through NPRR 777, entitled “ERCOT-Directed Dispatch of Price-Responsive Distributed Generation,” proposed by Shell Energy North America.

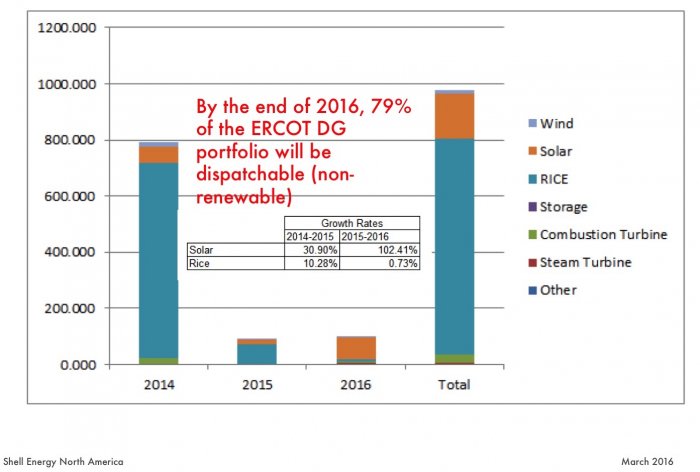

The fundamental idea of NPRR 777, as laid out in a May presentation (PDF), is to create a new way for distributed generation resources that already exist to become integrated into ERCOT’s real-time energy market, known as its Security Constrained Economic Dispatch, or SCED. For the most part, these consist of fairly large-scale, but under 10-megawatt, natural-gas or diesel-fired backup generators, installed to help keep critical infrastructure running in the wake of hurricanes.

Paul Wattles, ERCOT market design senior analyst, noted during a panel at last month’s Grid Edge World Forum in San Jose, Calif. that about 80 percent of distributed generation in ERCOT is self-dispatched diesel, natural gas or landfill gas.

“The reason for that is, we have hurricanes,” Wattles said in a July interview. Specifically, after 2008’s Hurricane Ike laid waste to the Texas Gulf Coast, the state legislature passed a law strongly encouraging critical infrastructure, including oil and gas facilities, to provide for their own backup electricity.

“What I don’t think anybody foresaw was, what about the hours when we don’t have a hurricane?” he said. According to ERCOT estimates, there may be as much as 1 gigawatt of these types of resources in place in Texas -- a significant amount of emergency resource.

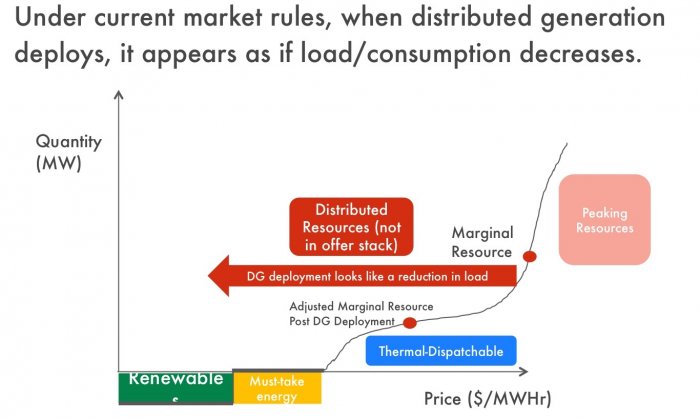

Today, these generators can, and do, start up when grid electricity prices are high enough to make it worthwhile to their owner-operators, he said. But because they aren’t “mapped” to ERCOT’s SCED dispatch system, “they’re invisible to the market,” and appear only in the form of suddenly reduced loads at the sites where they’re located, he said.

The main idea behind NPRR 777 is to turn those self-dispatched generators into “mapped distributed resources,” or MDRs -- an important first step in allowing them to become dispatchable resources under ERCOT’s SCED, he said. “Mapping would be important for us. […] To be able to qualify them as a new resource type, they have to be mapped to the grid.”

That’s a similar approach to the way that ERCOT now dispatches much of the distributed load resources available to it under its Responsive Reserve Service, or RRS, he noted. According to GTM Research, as of the end of 2015, there were 242 load resources registered under RRS, offering about 3,400 megawatts in aggregated capacity, of which about half is available during any particular operating hour to respond to 30-minute or 10-minute dispatch.

The limits of NPRR 777: Where it doesn’t go yet

As Blevins pointed out, mapping distributed generators alongside distributed load will be important for discovering the relationship between real-time energy prices and self-dispatch. “One of the reasons you want this is that it helps lead to price formation,” he said. “Generally, I have heard market participants in many categories being supportive of the idea of resources putting in what their offers are, so that the market can settle more efficiently.”

What NPRR 777 doesn’t do, at least explicitly, is take on the question of how to deal with smaller distributed generation resources, he said. That could include aggregations of rooftop solar PV, or behind-the-meter batteries, or fleets of charging electric vehicles.

NPRR 777 also doesn’t push for allowing DERs to be paid the nodal price for electricity, as measured at the thousands of individual points where the transmission system connects to the distribution grid, he said. Instead, it would use the far more broad “zonal” prices for electricity, which are calculated across four broad regions of Texas under its competitive market.

While that would prevent DERs from participating in prices based on local congestion, it’s also a far more simple approach that could make it much easier to carry out. Indeed, according to Texas market players, sticking to zonal pricing instead of the more discrete nodal pricing might actually be a better deal for DERs.

According to Maura Yates, VP of sustainable solutions for Texas energy retailer and renewable energy developer MP2 Energy, in the discussions around the DREAM initiative, “No energy developer, no solar developer, found a situation where going nodal is beneficial for that DG customer.” That’s because taking nodal prices would require retailers to cover congestion costs, as well as manage the risks of those prices changing over time -- factors which don’t come into play with zonal pricing.

“In our eyes, we think where DREAM landed is a good starting point,” she said. “Getting ERCOT more visibility into the resources on the grid is really useful. There’s going to be a lot of distributed generation on the grid -- in fact, it’s going to be the primary new resource.”

As Blevins noted, “These are all baby steps, so that we can see what resources can do, what’s there on the distribution system -- but moving toward being integrated with the ERCOT-wide market.”

The fate of FAST -- or, how to avoid the wrath of the generators

Why have the backers of the DREAM initiative taken this go-slow approach? One might look at the fate of the FAST initiative as a lesson in what can happen when would-be rule changes, no matter how important for making the state’s grid markets more efficient in the eyes of ERCOT, can face backlash from generators seeking to preserve market power.

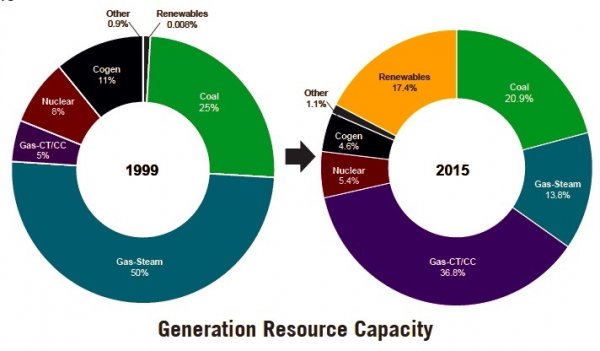

The Future Ancillary Services Team, or FAST, was launched in 2013 as an attempt to rework the state’s antiquated markets for a specialized set of grid services that are needed to keep it stable during times of crisis. According to an ERCOT presentation (PDF), since existing rules were created in the 1990s, new developments such as the increasing penetration of distributed and utility-scale intermittent wind and solar power, as well as the evolution of fast-acting storage devices and sophisticated smart grid technologies, have opened up opportunities for an “unbundling” of services that could make the system work more efficiently.

Specifically, ERCOT said that the proposed changes would cost about $12 million to $15 million to implement, and would save about $20 million from the roughly $500 million per year it spends on the ancillary services under consideration, if one assumes that natural gas prices stood at about $4.35 per million BTUs. Even if gas prices fell to about half that price, the annual savings would add up to between $11 million and $16 million, according to a Brattle Group study.

But the FAST effort has faced an uphill battle from the get-go against the companies that operate the power plants that provide the majority of ancillary services under the state’s existing rules. NPRR 667, which codified ERCOT’s plan to split up ancillary services into four new categories, was tabled in 2014, and then rejected in a vote by ERCOT’s Protocol Revision Subcommittee in early May. ERCOT appealed that decision, a very rare step for the grid operator, but that appeal was voted down in a May 26 meeting of the ERCOT Technical Advisory Committee, and ERCOT has decided not to pursue further appeals.

Lenae Shirley, senior director of technology innovation and market adoption for the Environmental Defense Fund, told me in a July interview that generators opposed NPRR 667 on the grounds that it wasn’t cost-effective, and didn’t include the costs that market participants would have to bear to set up resources to play under the new rules.

But underlying those arguments are the simple facts that coal-fired generators in Texas today are struggling to remain profitable, and may well want to preserve their ability to offer ancillary services under existing rules, she said. “Prices have been at rock-bottom, and we have enough demand response so that when they do creep up, demand response brings them back down again.”

At the same time, “we don’t want to keep old plants alive just to provide reliability -- we want to see a role for distributed generation and energy efficiency,” she said. The same stakeholders that were driving the FAST effort are now regrouping to come up with alternative proposals to bring ERCOT’s ancillary services regime into alignment with today’s market conditions and new technologies, she said.

As Blevins noted, “Even some market participants who voted to reject NPRR 667 agreed that the ancillary services products could be updated in a way that does disaggregate some of the faster-responding frequency products from the slower contingency-type products.”

“They think there could be a simpler, smaller step that could achieve many of the same benefits, without introducing more...complexity or costs of market implementation,” he said.

In other words, when trying to make changes in Texas’ energy market, baby steps have a greater chance of bringing new concepts to maturity -- a tactic that’s part of the current push to bring the state’s DREAM concepts to reality.