Texas, despite being one of the country’s largest and sunniest energy markets, has not seen a lot of growth of distributed solar power. Beyond low energy prices, one big reason is that the Texas deregulated energy market, which covers about three-fourths of the state, doesn’t allow for net metering rules like those in place in California, Hawaii and 41 other states, which dramatically improve the economics for owners and aggregators of rooftop PV.

But perhaps the state’s competitive market could be re-jiggered to give distributed solar -- and all sorts of other customer-sited distributed energy resources (DERs) -- a chance to earn more money, if they can be aggregated and located in places where it’s more costly to deliver grid power to end customers.

Over the past few months, Texas grid operator ERCOT has been quietly crafting a proposal that could set up just this kind of regime for distributed energy. The ideas in play include allowing aggregated DERs to earn a broad, averaged-out wholesale price for the energy they export to the grid, opening up access to payments based on the cost of wholesale power at specific points on the grid, or even creating opportunities to play in ERCOT’s lucrative energy and ancillary services markets.

That’s not the same as mandating that DERs get paid the retail price for electricity they export to the grid, as most net metering regimes do. But it could provide a path for aggregated DERs located in higher-priced parts of the state’s grid to bring significant amounts of energy to the market -- and to make a lot more money.

“[W]e’re not going to the PUC... [and] the wires companies and saying, ‘We are going to mandate that you include such-and-such distributed energy resource in your plan,’” said Chad Blevins, senior consultant with Austin, Texas-based law firm The Butler Firm and chairman of ERCOT’s Emerging Technologies Working Group. “This is a world in which the independent power producers, the independent developers of projects, are going out there and trying to make deals happen.”

ERCOT held a workshop on the proposal last month, and is planning two more meetings this month and next to “get the broad concepts out in front of the market,” Paul Wattles, market design senior analyst for the Texas grid operator, said in an interview last month. A full concept paper is expected to be ready in or around September. In other words, this is very much still a work in progress and isn’t an official proposal yet, he said.

Changes to Texas’ energy market can take years to move from concept to completion, and face plenty of opportunities for being derailed along the way, as we've noted in our coverage of the slow development of demand response in Texas, or the stalled attempt to pass legislation to allow utility Oncor to own distributed energy storage assets.

Even so, ERCOT’s proposal aligns with its goals to bolster grid stability, lower overall power costs, and provide more visibility into how distributed energy could play a role in supporting the grid at large, Wattles said.

This visibility will become increasingly important as Texas starts to see the same growth in DERs as has happened in bellwether states like Hawaii, California and New York. “In the past, there have not been that many distributed energy resources” in the state, according to Ken Ragsdale, market design principal at ERCOT. “But on the horizon, we see the potential for more rooftop solar, more batteries, more natural-gas backup generators.”

So how might ERCOT’s proposal change the DER game in Texas? Here’s a brief breakdown, based on the three key classifications the grid operator is considering -- DER Minimal, DER Light, and DER Heavy.

From business-as-usual to more pinpointed DER pricing

All three of the proposals include the ability for DERs to be aggregated into larger blocks of energy. The groundwork for this was laid last year, when ERCOT created its Aggregate Load Resource (ALR) classification that allows individually metered demand-response sites to be aggregated for participation in the state’s grid markets.

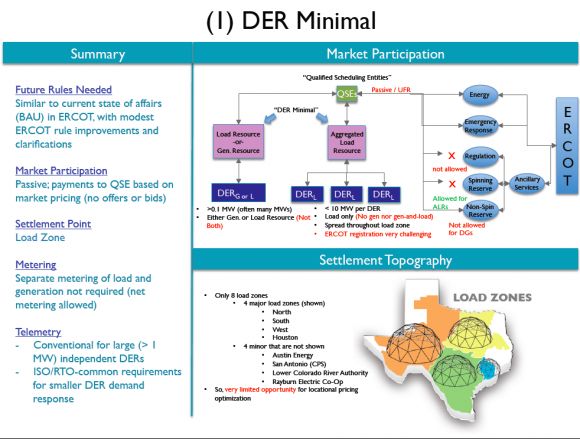

But in terms of how much resources would get paid for that aggregated energy, “DER Minimal is pretty much business as usual,” Wattles said of the first option that ERCOT is exploring. That means that what they can earn is based on the Load Zone Settlement Point price -- an average price for whichever of the state’s four “load zones” the DER happens to be sited. Here’s a graphic from The Butler Firm that lays out the key facts for DER Minimal.

These load zones cover broad parts of the state’s west, north, and south regions, as well as the Houston area. While certain locations within each zone might experience high prices during different times of the day, based on transmission and distribution constraints that make it more costly to serve load in that location, there’s no mechanism today for linking DER payments to these locational marginal pricing (LMP) nodes.

“The constraint about load zone average pricing is that it dilutes the value of placing distributed generation in places where it could have benefits,” Wattles said. “There are some that are in the system in locations that could be really beneficial to grid operations.”

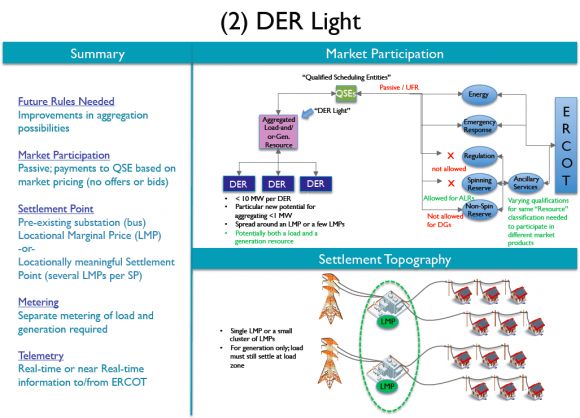

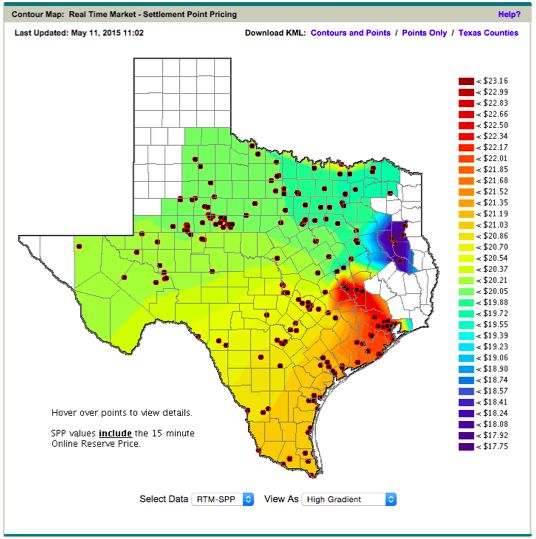

“That’s a major driver of our DER Light proposal,” he said, which would take the important step of allowing aggregated DERs to get paid the locational marginal price for the energy they export to the grid. That could be either higher or lower than the average zone price, but it has the virtue of more closely tying the value of the electricity the DERs are generating to its value for the local grid, at the time it’s being generated. (This real-time map of LMPs across Texas indicates how they can shift over the course of the day.)

That’s going to require some extra technology to make it work, however. “You may be able to export power, but if you are, we’re going to have to have that generator metered at all times,” he noted. That’s different from net metering, where the same meter tracks DER generation by subtracting it from whatever the building is consuming.

Complications arise in connecting LMP nodes, which are located at substations, to DERs that are located at endpoints on the distribution grid, he said. ERCOT is working on ways to simplify these metering requirements, building on its experience in aggregating demand response resources like household air conditioners, he said.

“We understand you can’t put a physical remote terminal unit on every air-conditioning unit -- that would be prohibitively expensive. You need to understand what’s going on with your resource, and create a telemetry signal that we can use in real-time operations. But that all falls apart if we can’t validate the telemetry.”

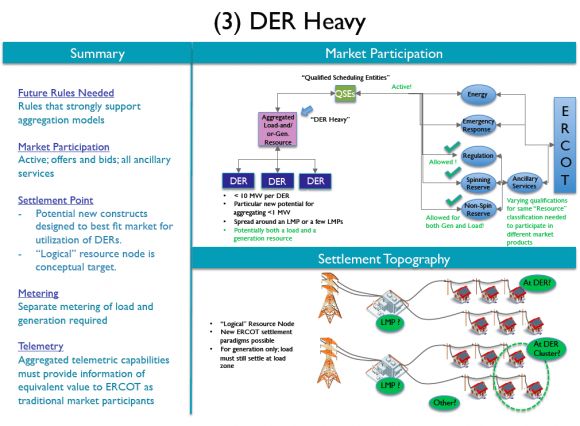

The “DER Heavy” proposal brings another layer of potential revenue streams to aggregated DERs, by allowing them to play into ERCOT’s energy and ancillary services markets. These offer more lucrative payments for resources that can respond to signals from ERCOT to supply or absorb power to balance fast-changing grid conditions, and would require the same kind of real-time communications links and metering that ERCOT requires of the big power plants or cogeneration facilities that serve these markets today, Ragsdale said.

These three options aren’t mutually exclusive, ERCOT's Blevins noted. “If we could move forward with a couple of registration pathways, when a resource enters the market, they could decide what works right for them,” he said.

Growing a competitive market for distributed energy

Plenty of questions remain about how these kinds of market reforms might affect the economics of rooftop solar, or solar paired with energy storage, or more complex combinations of on-site energy generation and management technologies. From the rooftop solar perspective, much will depend on whether the benefits of being able to access localized prices for exported energy outweigh the costs and complexities of aggregating and metering them in ways that would allow them to play in the new regime.

Texas does have more lucrative programs for rooftop solar, but they’re offered by the municipal utilities of Austin and San Antonio, as well as a limited program from Dallas area utility Oncor. As GTM Research pointed out in a 2014 report, more than 90 percent of all residential PV in the state was installed in those three utility service areas in 2013 and 2014.

Beyond those areas, whatever customers get paid for energy generated that exceeds their consumption “is totally the subject of a contract with the [local] retailer,” Wattles said. Retail energy providers own the relationships with Texas customers in the deregulated portions of the state, and have to manage the cost of the power they’re delivering across the wires of utilities like Oncor, CenterPoint and AEP against the deals they offer their customers.

So far, “only a small number of retailers have solar programs going, where they’ll actually pay you for kilowatt-hours that go to the grid,” he noted. There are a few of these programs underway, such as SolarCity’s new partnership with Texas energy retailer MP2 to offer a net-metering-like deal to certain customers in the Dallas-Fort Worth area.

But just how those partnerships make money offering customers retail prices for their exported power, while being paid only the zone settlement wholesale price on their end, remains an open question. Presumably, they’re targeting customers in locations where local grid prices are predictably high during times when solar generation is at its peak, allowing them to reduce their need to pay for power being delivered to their customers when it’s most expensive.

The kinds of changes being considered in ERCOT’s DER Light and DER Heavy proposals could open these economic options not just for retail energy providers, but for independent DER project developers, or even individual customers with large enough power needs to make it worth their while.

Bringing in the ability to aggregate DERs for play in the state’s energy and ancillary services markets could open even more potential for solar-plus-storage systems, which can “bank” their power to inject it into the grid when grid prices spike. These price spikes tend to happen more frequently in Texas, which has no capacity market mechanism to pay for generators to be built to meet future grid peak demands -- and studies indicate that the state may fall below its target reserve margin by 2017, which could lead to even more price volatility in years to come.

It may be difficult to justify the economics of building massive new power plants on the chance that they’ll have enough opportunities to sell their power into the market during price peaks to cover their long-term capital and operating costs. But DERs can be installed one by one, making them a far more flexible tool to meet capacity needs -- if they can be aggregated to respond as a single unit at the times they’re needed.

Blevins noted that “there are resources being installed in the commercial and industrial world, largely for doing demand charge management,” or limiting expensive spikes in on-site electricity demand. “That can be a compelling value stream to get some storage, or micro-turbines, or similar energy management systems, in place in a commercial facility.”

In the future, “if that same asset could have an easy path to participating in the wholesale market, then you could bring in additional revenue, which could make installing that resource much more compelling.”

As we’ve been covering in some detail, utilities, grid operators and regulators in California, Hawaii, New York and other states are grappling with the right way to create mandates and markets to encourage this kind of decentralized approach to meeting broader energy goals.

But Texas’ deregulated energy regime will make its approach much different from these other states.

***

Grid Edge Live will bring together an emerging ecosystem of power industry thought leaders, including utilities, innovators, regulators and policymakers in San Diego, California from June 23-25. Attendees will discuss and debate the latest issues and opportunities impacting tomorrow’s distributed energy system, and examine the latest trends and innovation happening at the grid edge. Register here.

41

41

15

15

9

9