For a market that’s increasingly described as mature, the global wind industry still knows how to put up startlingly big numbers.

Wind developers placed orders for 31 gigawatts of turbines during the second quarter, the highest volume on record, and 79 gigawatts over the past 12 months, according to Wood Mackenzie’s quarterly analysis of the turbine market. The order surge comes as developers race to beat subsidy deadlines in the world’s two largest wind markets, China and the U.S.

Developers typically order turbines a year or so before building a project, to take advantage of the latest technology. The biggest year for wind construction so far was 2015, when around 64 gigawatts of new capacity came online around the world.

As is usually the case, China played the central role in the record-smashing quarter, with developers there ordering up 17 gigawatts of turbines, including more than 3 gigawatts destined for offshore projects.

“Some of the numbers are really quite staggering,” Luke Lewandowski, director for the Americas at Wood Mackenzie Power & Renewables, said in an interview.

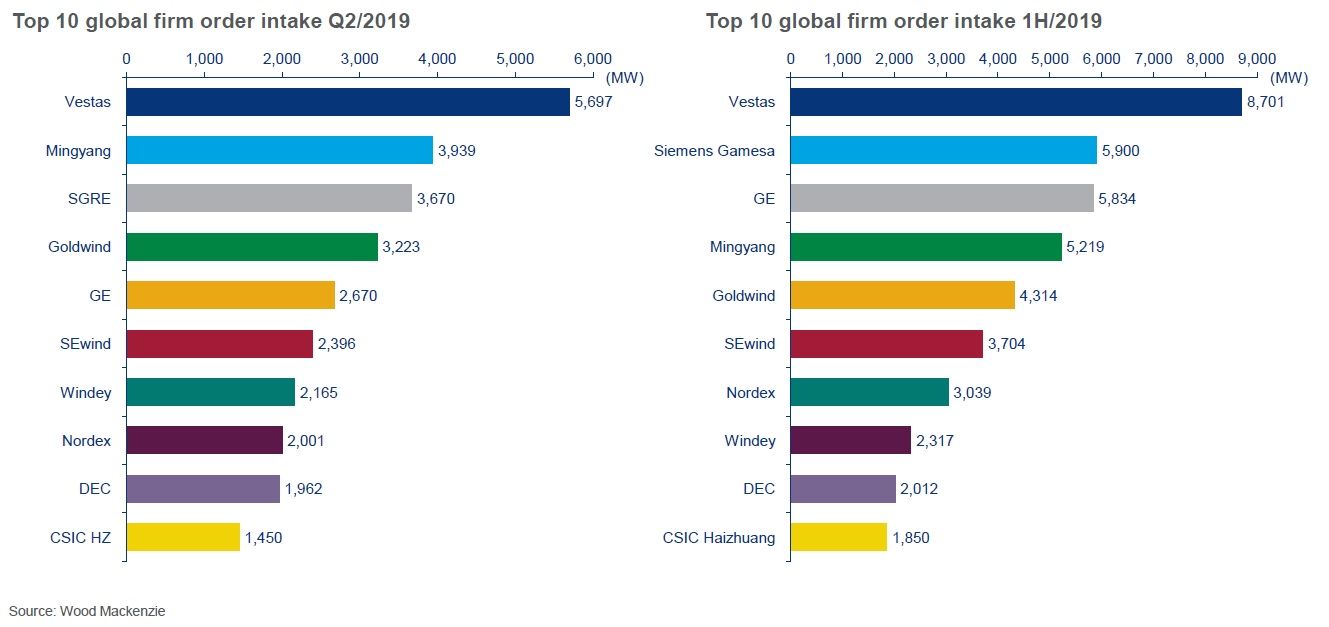

Demand in China resulted in an order bonanza for the country’s comparatively large number of wind manufacturers. Mingyang led the pack with 3.9 gigawatts' worth of orders thanks to strong demand from offshore developers in its native Guangdong province.

But a total of seven Chinese manufacturers clocked quarterly orders of more than 1 gigawatts, including Goldwind and SEwind, preventing the emergence a breakout leader. “There’s still a diversity of OEMs winning market share in China,” Lewandowski said.

Unlike the solar industry, China’s wind manufacturers have largely failed to make a dent outside their home market.

In contrast to the fragmented Chinese market, turbine manufacturers based in Europe and North America recently went through a period of intense industry consolidation, marrying Nordex with Acciona, Siemens Wind with Gamesa, and GE with parts of Alstom.

“Consolidation and contraction can still happen” outside China, Lewandowski said. “But I think the days of consolidation are mostly over.”

“There’s a demand and a need for technology to evolve,” he added. “If you don’t have strong financial backing or strong revenue, then you don’t have the R&D in place to keep up with the ever-changing technology landscape. It’s easy to fall behind and never really catch up.”

Denmark’s Vestas, the world’s largest turbine supplier, rode the wave of Q2 demand to capture the largest quarterly order intake for any wind manufacturer in history, at 5.7 gigawatts.

Vestas commanded dominant market shares above 40 percent across both the Americas and Europe, more than double Mingyang’s share in Asia-Pacific. GE came second in secured orders in the Americas, while Nordex took the silver in Europe.

WoodMac expects the global wind market to climb to new heights over the next few years, pushing past 70 gigawatts of annual installations in 2020 amid record construction in key markets like the U.S.

The global market is then predicted to slow down in the mid-2020s as it adjusts to a world with far fewer subsidies, before resuming growth later in the decade thanks in part to tailwinds from the expanding offshore sector.

***

To learn more about the order intake of global wind turbine suppliers in H1 and trends in market capacity, turbine size and pricing and future trends, explore the Wood Mackenzie report 'Global Wind Turbine Order Analysis: Q3 2019.'

41

41

15

15

9

9