Despite coronavirus-related setbacks, 2020 will be one of the biggest years for solar demand in Latin America. The period 2020-2025 will see utility-scale solar grow in many countries in the region, led by Mexico, Brazil and Chile, with distributed solar expanding most rapidly in Brazil.

But despite falling system costs, growth in the region will be fairly constrained, particularly in Mexico, where bottlenecks are slowing the pace of renewable energy development. Developers in the region will also face increased competitiveness in the market due to lower system costs and reduced power prices.

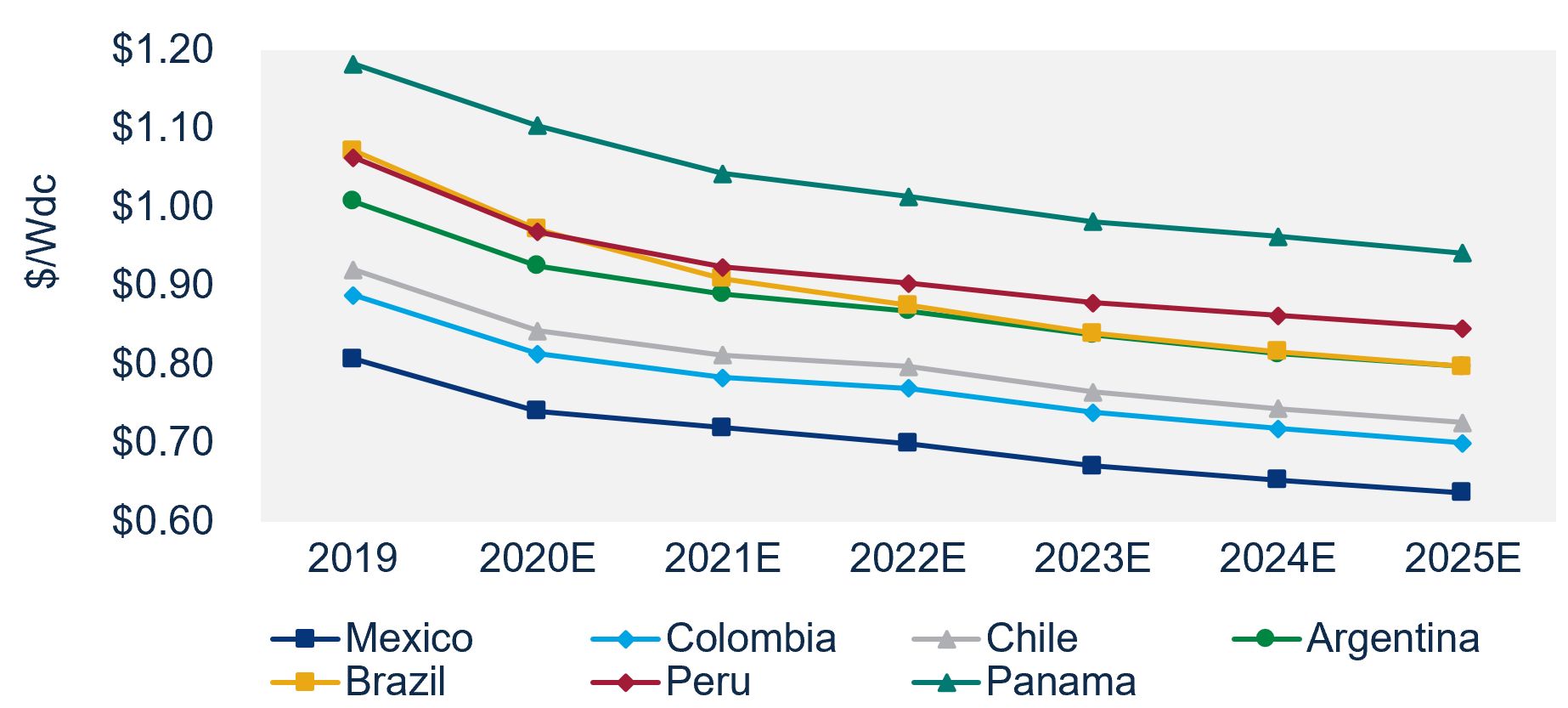

Country demand and system cost trends

As utility-scale solar demand climbs in 2020, system costs will fall. According to new research from Wood Mackenzie, average utility-scale system costs in major Latin American countries are expected to decline 9 percent from 2019 to 2020.

Mexico will have the lowest system costs of all the major markets analyzed, with Colombia and Chile close behind. Falling module prices, along with heightened competition among developers and engineering, procurement and construction (EPC) providers, will contribute to reduced system costs. Increasing module power density will also drive down costs.

All-in utility-scale PV system costs by country in Latin America, 2019-2025E ($/Wdc)

Source: Wood Mackenzie

However, while falling costs will be a driver of future solar demand, major Latin American countries will face headwinds that will stunt market growth over the next five years.

Wood Mackenzie estimates solar PV installations in Mexico will grow by only 7 percent this year compared to 2019, a slowdown that is linked to increasing political and regulatory uncertainty and high development costs due to pandemic-related delays.

The slowdown will continue into the 2020s. No new auctions are planned in the foreseeable future due to an unfavorable shift in policy from Mexico’s government and new measures that don’t encourage private investment in the renewable electricity sector.

Brazil’s growing utility-scale pipeline faces a somewhat different set of challenges. Although Brazil's pipeline of utility-scale projects keeps growing, these projects' operational and economic feasibility hinges on an increase in energy demand, which in turn could jeopardize their operational timelines. Capacity additions will slow by around 2023 when the government is expected to remove transmission rate subsidies for renewable energy projects.

On the other hand, Brazil has incentivized growth in its distributed solar segment, which grew 266 percent between 2018 and 2019. Net metering and low-interest-rate financing from private and public banks are expected to fuel further growth through 2025.

Chile's solar market will experience unprecedented growth in 2020 and 2021, driven in part by its Pequeños Medios de Generación Distribuida (PMGD) regime and a sound policy framework targeted toward renewable energy investments. The PMGD scheme guarantees developers a stable price for projects up to 9 megawatts (AC). However, this pricing framework is expected to change in the first half of 2022, when developers are subject to fluctuating prices.

Challenges to solar growth

Power oversupply and a decrease in demand in both Brazil and Chile have challenged solar project economics and increased the competitiveness of bilateral power-purchase agreements. Delays and difficulties in obtaining governmental permits have become an additional burden for developers in countries like Brazil and Mexico. In Mexico, the process of obtaining proper permitting and interconnection agreements has become increasingly challenging for developers under the current government, and the COVID-19 pandemic has only made matters worse.

Developers in Mexico face other challenges, including securing financing and long-term power-purchase agreements, due to the risks associated with regulatory uncertainty. The Mexican government also requires a social impact assessment for new project development, which can increase developer costs. Social consult requirements have also been a cause for setbacks in Colombia, especially in the north where local communities have significant influence and are crucial in the development of projects. Depending on their level of experience operating in Colombia, developers may opt to hire external consultants to navigate the local processes and variables, which can increase costs.

Brazil faces some of the highest system costs in Latin America, in part due to local content requirements and import tariffs. Even though the import tariffs on solar components were removed earlier this year, system costs remain higher than average.

Brazil also experiences volatile foreign exchange rates, and developers may hold off on procuring equipment if rates negatively impact a project’s profitability. Like Brazil, Argentina also prefers local content, which can increase system costs. Further, the political and economic uncertainty in Argentina has created an unfavorable environment for new solar development.

If solar demand slows year-over-year, system costs may fall at a slower rate due to reduced EPC and developer competition.

Beyond 2020

Even as utility-scale solar growth is hindered in some countries beyond 2021, system costs are still expected to fall. High demand for bifacial module technology will continue to drive down soft costs; the same trend could materialize with system costs as these module prices become competitive with monofacial module prices. Furthermore, total solar demand in these major Latin American countries will also be driven by the distributed generation segment as prices continue to drop, particularly in Brazil and Chile.

Chile’s new PMGD price framework, slated to roll out in 2022, will likely heighten demand for projects to be completed before that time but might hinder growth after the rollout, given the fluctuations baked into the new price scheme.

Regarding residential solar, Chile, Mexico and Brazil all have promising outlooks. Mexico maintains the lowest average residential system prices at $1.04/Wdc in 2020, while many projects report total prices well under $1.00/Wdc. Both Mexico and Brazil have low barriers to entry for residential installers, which increases competition and will contribute to future residential price declines.

Sound financial positions and local knowledge will be crucial for new market entrants as markets mature and competitiveness increases. While hardware component prices continue to fall, developer costs remain elevated with very little room to decrease year-over-year.

There will be a heightened focus on reducing these developer costs as countries in the region make progress with their renewable developments.

Strong market conditions and policy frameworks will be crucially important to fuel increased growth.

***

Molly Cox and Valentina Izquierdo are Wood Mackenzie solar analysts. Learn more about the new reports, Latin America and Canada solar PV system pricing 2020 and Global solar PV market outlook update: Q3 2020.

41

41

15

15

9

9