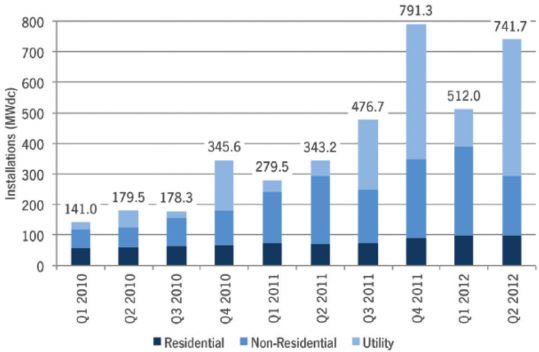

GTM Research and the Solar Energy Industries Association® (SEIA®) today released U.S. Solar Market Insight: 2nd Quarter 2012. The report finds that U.S. solar achieved its second-best quarter in history, having installed 742 megawatts of solar power, and the best quarter on record for the utility market segment. Utility installations hit 477 megawatts in the second quarter, with eight states posting utility installations of 10 megawatts or greater: California, Arizona, Nevada, Texas, Illinois, North Carolina, New Mexico, and New Jersey. In total, the U.S. now has 5,700 megawatts of installed solar capacity, enough to power more than 940,000 households.

According to U.S. Solar Market Insight: 2nd Quarter 2012, the utility photovoltaic (PV) market will remain strong through the last two quarters of 2012. With 3,400 megawatts of utility PV projects currently under construction, and weighted U.S. average system prices 10 percent lower than the previous quarter, GTM Research forecasts an additional 1.1 gigawatts of utility PV to begin operating before year’s end. The report forecasts a total of 3200 megawatts, or 3.2 gigawatts, of PV will be installed in the U.S. in 2012, up 71 percent over 2011.

FIGURE: U.S. Solar PV Installations, 2010-Q2 2012

Note: Figure for PV installations above does not include 30-megawatt CPV project installed in Q2 2012 characterized as concentrating solar power within the report.

Source: U.S. Solar Market Insight: 2nd Quarter 2012

“The U.S. solar industry is rapidly growing and creating jobs across America despite the slow economic recovery,” said Rhone Resch, president and CEO of SEIA. “More solar was installed in the U.S. this quarter than in all of 2009, led for the first time by record-setting utility-scale projects. With costs continuing to come down, solar is affordable today for more homes, businesses, utilities, and the military. Smart, consistent, long-term policy is driving the innovation and investment that’s making solar a larger share of our overall energy mix.”

For the fourth consecutive quarter, the U.S. residential solar market grew incrementally, installing 98.2 megawatts. California, Arizona, and New Jersey led residential installations nationally, with smaller-market states of Hawaii, Massachusetts, and Maryland demonstrating strong quarter-over-quarter growth.

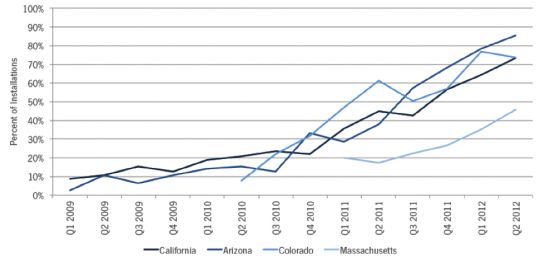

In addition, the residential segment continues to be highlighted by consumer acceptance of third-party solar ownership models. The major state markets in California, Arizona, and Colorado all saw third-party residential solar account for greater than 70 percent of total Q2 2012 installations. U.S. Solar Market Insight: 2nd Quarter 2012 finds that in the California market, this quarter marks the first time that the average installed price of a third-party-owned system was lower than that of a system purchased outright: $5.64 per watt for third party versus $5.84 per watt for directly owned solar systems.

“We’re starting to see innovative PV business models take a substantial hold in the U.S. residential market,” said Shayle Kann, Vice President of Research at GTM Research. “The success of third-party residential solar providers has attracted more than $600 million in new investments in recent months. This influx of cash into the residential space signifies the growing acceptance of solar leases and power purchase agreements as a secure investment for project investors. We expect that third-party installations will claim even more market share in the coming quarters.”

FIGURE: Percentage of Residential Third-Party Installations in Arizona, California, Colorado & Massachusetts, 2009-Q2 2012

Source: U.S. Solar Market Insight: 2nd Quarter 2012

In contrast to the utility and residential markets, the non-residential (e.g., commercial, government, non-profit) segment contracted, falling from 291 megawatts in Q1 2012 to 196 megawatts this quarter. Although California (down 45 percent) and New Jersey (down 35 percent) contributed to a large part of the decline, these states were not alone. Only ten of the twenty-four states the report tracks individually saw quarterly growth in the non-residential market in Q2 2012. This trend was likely due to a combination of factors. In some individual markets such as New Jersey, it was a result of state-market-specific factors such as SREC oversupply. In other states, Q1 2012 had been bolstered by safe-harbored 1603 Treasury Program installations.

In addition to coverage of U.S. demand markets, U.S. Solar Market Insight: 2nd Quarter 2012 provides insight into the state of PV component manufacturing in the U.S. Global oversupply continues to be the chief challenge to U.S. PV suppliers, as wafer, cell, and module production in the U.S. fell 33 percent, 25 percent and 28 percent, respectively in Q2 2012 as a result.

41

41

15

15

9

9