Thin-film solar production is expected to double in each of the next three years to reach 4.18 gigawatts worth of equipment in 2010, according to a report to be released by Greentech Media and the Prometheus Institute on Tuesday.

"The thin-film [photovoltaics] sector is going to make a major impact on the overall growth of the PV industry in the next five years," wrote authors Sorin Grama and Travis Bradford, both of the Prometheus Institute. "It will change the economics to customers, trigger a more competitive landscape for all solar-energy technologies and force capital markets to assess and adapt yet again to a changing solar landscape."

The forecast represents a 65 percent increase from the companies' previous projection 18 months ago, according to the report. The authors also forecast that production will continue to grow, reaching almost 10 gigawatts in 2012.

The projections are based on a survey of 137 companies. According to the report, at least 143 companies were participating in thin-film solar as of July, with nearly 40 companies entering the space in 2007 and an additional 23 companies joining the movement in the beginning of this year. This implies that nonparticipating companies, as well as new companies yet to enter the field, could end up pushing the numbers even higher.

Most of the new companies are developing amorphous-silicon films on glass, which Prometheus said has the lowest barriers to entry because companies can buy "turnkey" manufacturing equipment from suppliers such as Applied Materials and Oerlikon.

While many companies already are entering the amorphous-silicon arena, the ramp time and output of amorphous-silicon lines has been "somewhat less robust" than originally expected so far, they wrote. "The ramp delays should be temporary however, and amorphous silicon is expected to make dramatic gains in production over the next couple years."

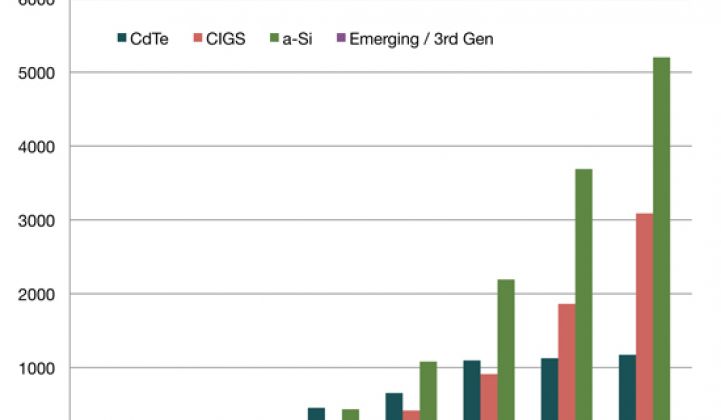

About 53 percent of thin-film companies are pursuing amorphous silicon, wrote Grama and Bradford, who expect amorphous-silicon films to make up half of the total thin-film production by 2010 and the majority of the production after that.

They expect cadmium telluride, which had the highest production in 2007, to remain the most common thin film to be produced this year before being overtaken by amorphous silicon. Cadmium-telluride films, which have been popularized by No. 1 thin-film manufacturer First Solar, will end up as a niche technology adopted by only a few companies, they wrote, although First Solar will remain a significant player in the industry.

Meanwhile, copper-indium-gallium-diselenide technologies – also known as CIGS–- "[remain] the most exciting, but also the most elusive," according to the report. Grama and Bradford predict that 2009 will be a breakout year for the technologies, adding that some might be able to expand quickly enough to meet or beat First Solar's cost and performance targets by 2011.

According to the report, First Solar (NSDQ: FSLR) will remain the largest thin-film manufacturer in 2010 with an estimated 1 gigawatt of production of cadmium telluride.

The authors expect the company to be followed by Sharp Corp., with 416 megawatts of estimated production of amorphous silicon; United Solar, with 254 megawatts of estimated production or amorphous silicon; Nanosolar, with 249 megawatts of estimated production of CIGS, and Miasolé, with 178 megawatts of estimated production of CIGS.

All together, Grama and Bradford expect only eight of 144 firms to reach "significant production" – defined as more than 25 megawatts of production – this year, increasing to around 30 companies by 2010.

Prometheus expects the sector to continue to hold its advantage with projected costs of less than 70 cents per watt. Such costs would enable a price of $1.40 per watt or less with a 50 percent gross margin, according to the report.

Meanwhile, the authors forecast that traditional crystalline-silicon wafer, cell and panel makers could see gross margins of less than 15 percent in some situations.

41

41

15

15

9

9