According to a recent study, there are 806 geothermal power projects in development around the world with a combined capacity of 23,313 megawatts, with the majority located in Asia, North America and Africa.

That sounds impressive, but the industry faces strong challenges everywhere. Projects need to secure government approval, public consent (sometimes complicated by local opposition), power purchase agreements and, last but not least, necessary financing. The latter has been particularly challenging.

In addition, the push to explore for unconventional natural gas has been counterproductive to geothermal development in the United States, despite the green credentials of geothermal power.

Looking at overall projects in development, Asia is by far the most active, with a combined planned capacity of around 10,100 megawatts. The majority of these projects can be found in Indonesia, followed by the Philippines and Japan. North America follows with around 6,340 megawatts in development, mostly in the U.S. Africa has a planned capacity of around 2,500 megawatts, mainly in Kenya. European development accounts for around 1,400 megawatts, which mostly falls on Iceland and Italy. Turkey, which was categorized as being part of the Middle East, has around 800 megawatts in development.

Looking at individual countries, Indonesia is the leading country, with more than 8,000 megawatts of projects in development. It is followed by the U.S. with around 6,100 MW in development. If all projects were to come on-line, America would still remain the top country, with Indonesia coming in a close second.

Ranking third with around 1,880 megawatts under development and an installed capacity of 175 megawatts, Kenya is probably one of the hottest markets at the moment. All the major suppliers and service firms have been actively pursuing business opportunities in a market that is supported by various national development banks, and international organizations such as IFC, the World Bank and The African Development Bank.

The Philippines have announced ambitious geothermal development plans, but account only for around 1,550 megawatts of concrete development, with a currently installed capacity of 1,968 megawatts.

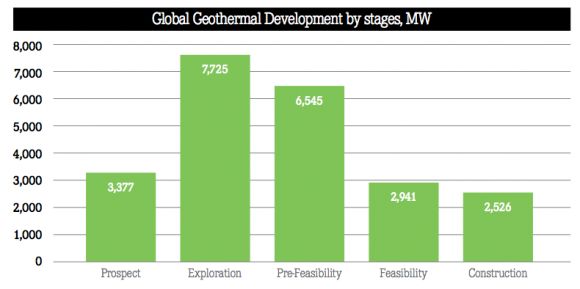

Source: ThinkGeoEnergy

The fourth largest market today is Turkey. With its continuously growing economy, Turkey is looking to geothermal to fuel its increasing energy demand. The country currently has some 780 megawatts under development, most of this utilizing lower-heat resources and combined development plans for power generation and direct use in greenhouse and district heating applications.

Iceland has some 780 megawatts of geothermal power generation capacity on the drawing board, somewhat less than the plans called for before the financial collapse of 2008. The geothermal market has slowed substantially since then, mainly due to political disagreement regarding development and the apparent lack of foreign investment.

Also notable are New Zealand and Mexico. New Zealand has seen a strong increase in installed geothermal capacity and has around 500 megawatts in various stages of development. Mexico is planning to increase its current geothermal power generation capacity of 810 megawatts by about 25 percent in the coming years.

This year, the Italians celebrated the centennial anniversary of the first commercial geothermal power plant at Larderello in Tuscany. The operator of the Larderello plants, Enel Green Power, seems though to be looking abroad for further developments, especially in South and Central America. This is related to Italy’s weak economy and local opposition toward some development plans.

Interestingly, Japan only comes in at number ten in the rankings. Despite its plentiful geothermal resources, ambitious renewable energy plans following the 2011 earthquake and nuclear crisis, and the resulting electricity shortages, geothermal energy development has not picked up. Supporting legislation and the opening up of national parks has so far resulted in eight geothermal projects, though rather small-scale, with a combined capacity of 116 megawatts.

Current development still only scratches the surface of the large geothermal development potential, which includes not only conventional geothermal resources, but also the application of enhanced/ engineered geothermal systems (EGS) technology for thus far insufficient conventional resources. Based on various sources, we estimate a more conservative development potential of around 180,000 megawatts.

Analyzing where projects are in the development phase provides a great overview of the business opportunities for suppliers to the industry. Based on available data, we estimate that more than 75 percent of all projects are in the early stages of development, having not yet proven their resources. Almost two-thirds of those are still in the prospecting and exploration phases.

Only around 24 percent of all projects are either drilling or already in the construction phase. With everything going as planned, only some 5,000 megawatts will be on-line in the coming two to four years. Without efforts to help projects finance the drilling of necessary wells, many of these early-stage projects might not be able to move ahead.

***

This article was originally published at ThinkGeoEnergy and was reprinted with permission.

Alexander Richter founded ThinkGeoEnergy in late 2008. He is a Board Member of the Canadian Geothermal Energy Association (CanGEA) and formerly of the U.S. Geothermal Energy Association (GEA). He was a founding member of the first and only geothermal-energy-focused investment banking team at Icelandic bank Glitnir (now Íslandsbanki).

41

41

15

15

9

9