Distributed energy resources can include rooftop solar PV, behind-the-meter batteries, or other sources of electricity. But they can also include demand-side resources -- homes, businesses, factories, farms, or electric-vehicle fleets, capable of curtailing electricity consumption when the grid needs it most.

California has been hard at work on new regulations and market structures to bring distributed energy resources (DERs) into play as grid assets. Next week, it will start taking bids for its latest experiment on the demand side of the DER equation -- the Demand Response Auction Mechanism, or DRAM.

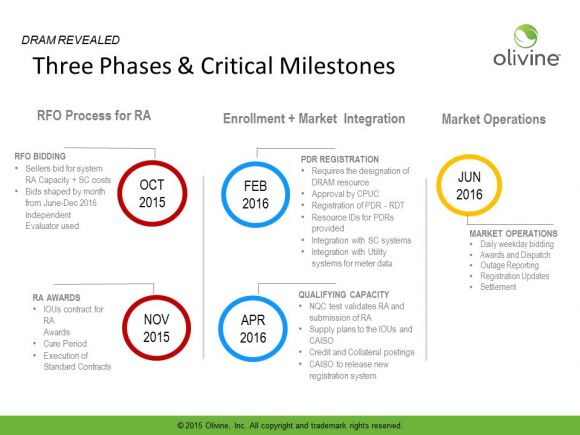

Under rules laid down by the California Public Utilities Commission (CPUC) in June (PDF), Monday, Oct. 26 is the deadline for would-be aggregators of grid-scale distributed resources to submit their DRAM bids to the state’s big investor-owned utilities. For the first time, the state’s grid markets will be open to DERs, aggregated into units of at least 100 kilowatts in scale, as an alternative to large, centrally controlled power plants or demand-response resources.

These bids are likely to include a blend of demand-side portfolios, from behind-the-meter battery systems at commercial and industrial buildings, to smart thermostats and electric-vehicle chargers at homes.

Each will name its own price per kilowatt for the combination of demand reduction it has to offer, or believes it can get in place by June 2016, when the DRAM resources are expected to come into play in California’s grid markets.

Utilities have until November to make their awards. Each has a minimum target for how much DRAM it should obtain -- 10 megawatts apiece for Pacific Gas & Electric and Southern California Edison, and 2 megawatts for San Diego Gas & Electric, with at least 20 percent of each to come from the residential sector.

That’s not a huge market to compete over, compared to the hundreds of megawatts of traditional demand response being done through dozens of utility and grid-operator programs across the state.

But the DRAM pilot's 22-megawatt minimum is a floor, not a ceiling -- and according to Beth Reid, CEO of Olivine, the number of bids submitted is likely to exceed expectations. That’s because this year’s DRAM pilot project is meant to establish ground rules for how a lot more of California’s demand response is done in the future -- and would-be contenders in that future market want to establish themselves.

“Based on the conversations I’ve had, I think there will be a significant number of bids, more than were anticipated,” Reid said in a Thursday interview. Olivine is the scheduling coordinator responsible for interacting with grid operator CAISO’s energy markets on behalf of companies putting bids into DRAM. That means she’s heard from a lot of “sellers,” in DRAM parlance, asking questions about the nuances of the program in advance of next week’s deadline.

“There are a lot of players who at least want to try it,” she said, though she wouldn’t name any specific companies. Greentech Media has talked to a few companies about their interest in DRAM, such as home energy automation startup Ohmconnect and smart-EV-charging startup eMotorWerks.

Others can be presumed to have bids in the works. Demand-response provider EnerNOC has teamed up with Tesla to test battery-backed supermarkets and other commercial/industrial customers in California, for instance, and Stem, Green Charge Networks and the dynamic duo of Tesla and SolarCity have lots of behind-the-meter batteries deployed in the state.

Energy storage could end up playing a significant role in many of the bids, Reid noted. “We have a reasonable amount of storage in the market, and people don’t realize it, because it’s acting as demand reduction,” she said. Of course, there are complications with taking batteries designed to reduce a building’s demand profile for relatively short periods of time, and assigning them the task of providing load reduction for four hours at a stretch.

Solar power and other distributed generation can also play a role, now that the DRAM program specifically allows net-metered customers and recipients of Self-Generation Incentive Program (SGIP) funding to participate, she said. But fossil-fuel-fired backup generators, or BUGs, won’t be permitted -- a nod to the state’s interest in promoting carbon-neutral resources.

DRAM differs from California’s established rules for demand response in a number of ways, including its combination of two concepts -- resource adequacy, or RA, and wholesale energy markets -- in a unique manner, she noted.

“What’s in it for utilities is the RA.” California’s utilities are required to procure resource adequacy to cover times of peak energy demand, and today that’s done through bilateral contracts with gas-fired power plants. But allowing aggregated DERs to play a role could reduce the need for these “peaker” plants, if they can provide the same reliable and flexible response.

Winning bids will have to provide some significant lengths of load reduction to meet these requirements -- four hours per day, available three days in a row, during specific hours of the day when utilities need it. In return, utilities will pay in advance for winning resources. That’s the capacity side of DRAM, and it’s expected to make up the majority of revenues for participants, Reid said.

But there’s another way for sellers to make money, one that utilities aren’t involved in. Starting in June 2016, DRAM program winners will start bidding their capacity into CAISO’s day-ahead energy markets, using the same structure that’s been set up for a series of pilot projects PG&E has been doing since last year.

It’s hard to predict how sellers will calculate the right price to offer, given the novelty of the approach. But “I think the price points will be dramatically different,” Reid said. “You’re talking about lots of different technologies, lots of different strategies. Lots of them are residential, others are large-scale C&I.”

No matter what combination they’re after, bidders will need to tally up what they believe it will cost them to deliver reliable load reduction from whatever demand-side resources they can muster, and try to predict what their competitors are offering. This “price discovery” function is part of the rationale for creating the DRAM in the first place, Reid noted -- “the idea is to let the third parties figure that out themselves.”

There’s a lot more complexity to the upcoming DRAM bidding and selection process, and that’s just for the first round. Another auction, for capacity to meet the 2017 peak season, will be held in April 2016, Reid said. These upcoming auctions will face new rules for “flexible” RA, as well as other developments in the state’s complex and ever-changing energy regulatory framework. We’ll be taking a deep dive into the DRAM at GTM Squared next week -- stay tuned for more details.

41

41

15

15

9

9