Section 25 of the federal residential Investment Tax Credit drops to zero on January 1, 2017 -- a short 13 months from now.

Effectively, the after-incentive selling price to residential homeowners will go up by 30 percent. A typical 5-kilowatt system at $4.00 per watt will increase in price from $14,000 (with the 30 percent ITC) to $20,000. It doesn’t take a degree in economics to conclude that residential sales will plummet.

Indeed, GTM and SEIA expect that it will take several years to find $1.20 per watt in cost savings in order to resume the pace of installations in 2016. The recovery period depends on the solar industry’s continued cost-reduction efforts, combined with future local electric rates and incentives.

The current cost stack for residential installers provides insight into the cost factors that are most likely to be reduced -- and those that will remain persistently high.

For the purposes of this analysis, costs are those experienced by typical small residential installers that buy through distribution, use microinverters or optimizers, install top-tier modules, pay sales tax, include a warranty reserve, and maintain a 5 percent net profit margin.

Obviously, large installers and installers with integrated financing models experience lower costs in some categories (such as equipment and direct labor), and higher costs in others (overhead, supply chain and financing-related costs).

A quick rundown of pre- and post-ITC cost components shows how challenging this $1.20 per watt reduction will be. Although some analysts project 40 percent cost reductions over the next few years, these calculations are often based on flawed assumptions about the “all-in” costs incurred by large installers. In reality, the categories with the most potential for cost reduction are hardware -- we as an industry have demonstrated an ability to reduce costs as volumes increase.

Soft costs will be much more challenging to reduce. There are structural reasons why these soft costs will remain stubbornly high. Unlike hardware costs, soft costs obey Murphy’s law -- not Moore’s or Swanson’s -- because they are created and defined by a myriad of local policies (many of which are designed to protect incumbent energy industries).

The following summary of cost reductions illustrates one path toward this $1.20/watt goal.

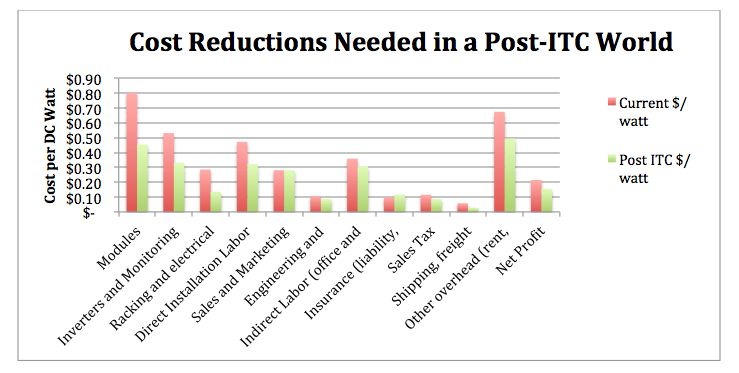

Modules: Save $0.35 per watt

Most manufacturers have product roadmaps that are likely to achieve these reductions. Improvements include lower-cost cells, higher efficiencies, automation, cheaper components (backsheets, junction boxes), supply-chain improvements (big savings potential here), and localized manufacturing.

I can hear the module companies grumbling already, but GTM Research forecasts combined with more efficient distribution strategies can achieve these goals. There is no doubt in my mind that on January 1, 2017, installers will be seeking out the solar modules that provide the lowest total installation costs (including installation labor and mounting systems), and will put less emphasis on manufacturer stability and perceived quality.

Inverters and monitoring: Save $0.20/watt

Improvements include component miniaturization, module integration and streamlined monitoring. On the other hand, new requirements (rapid shutdown, grid integration services, storage) will increase costs.

Racking and electrical balance-of-systems: Save $0.15 per watt

By integrating the mounting systems (no more racking or fiddly little rooftop parts), electrical components and grounding in the modules, racking and electrical costs can be reduced. Moreover, this component integration saves direct and indirect labor.

Ironically, the biggest barrier to further module integration is the module companies themselves, which are loath to increase their costs (with special module frames or module electronics), since they typically sell on a dollar-per-watt basis without considering downstream installation issues.

Direct installation labor: Save $0.15 per watt

Higher-efficiency modules, integrated racking and factory-installed module electronics will reduce installation costs. The challenge with reducing installation costs without simplifying equipment is that quality will suffer. Paying installation crews by the kilowatt installed will reduce costs -- but crews will be tempted to cut corners with inferior installation methods (missing rafters, substandard components).

Sales and marketing: No change -- and probably up

Medium-sized and small residential installers already acquire customers fairly inexpensively, and if homeowners haven’t purchased solar by the end of 2016, it is likely to be even more expensive to convert them after the ITC goes to zero. I have yet to see a rapidly growing solar company reduce its customer acquisition costs on a sustainable basis.

Engineering and permitting: Save $0.02 per watt

Software services that enable installers of all sizes to outsource their design and engineering will result in net savings (after accounting for the cost of the software itself). Some of these software services also help with system design, project management and shading analysis -- offering further potential for savings.

Indirect labor: Save $0.05 per watt

Indirect labor accounts for all the other labor expenses except direct labor on the roof -- including office and warehouse staff, project management, interconnection and incentive paperwork, and financing documents.

We are operating in a very paperwork-intensive industry; without eliminating the sources of this paperwork, it will be very difficult to reduce the office staffing necessary to support residential solar installations. Project management software is available to reduce these back-office costs, but software licensing fees and training costs must also be considered.

Insurance: Extra $0.02 per watt

Liability, workers' comp and health insurance costs for installers will go up, not down.

Sales tax: Save $0.03 per watt

Sales tax reductions are proportional to equipment purchases; if equipment costs go down, so do sales tax costs.

Shipping and freight: Save $0.03 per watt

Because of a complete lack of component integration, solar supply chain costs are high. Installers pay freight for modules, inverters and racking; and each manufacturer incurs freight charges from their factory to a local distribution facility. Better component integration and more efficient local distribution will reduce these supply chain costs.

Other overhead: Save $0.18 per watt

Overhead is a catch-all category that includes everything needed to keep a business running: bank charges, computer and office expenses, dues and subscriptions, meals, travel, accounting and legal fees, rent, maintenance, tools, telephones, utilities, and warranty expenses. Some of the overhead cost savings result from lower selling prices. Significant savings can be achieved by avoiding products and services that create additional overhead.

For example, I am aware of a number of residential installers that select financing products that are not burdened with complicated paperwork requirements, or hardware products that are easy and fast to install.

Net profit: Save $0.06 per watt

These savings are proportional to lower selling prices. If installers expect to stay in business for the long term, they must have sustainable profits.

The reality

Unless hardware costs plummet dramatically, I think it is optimistic that we will achieve these savings in a five-year period. All the soft-cost improvements put together add up to $0.35 per watt -- and achieving some of these reductions will be a stretch because the solar industry has little or no impact on the sources of these costs. On the other hand, $0.85 per watt hardware and direct labor savings (cost of goods sold) are within our industry’s control (and perhaps we can do even better).

For installers that keep a close eye on their gross profit margin, the necessary reduction in cost of goods sold means that gross profit margins must increase to cover overhead. At a $4.00-per-watt installed price and $2.09 per watt of cost of goods sold, the gross profit margin is 48 percent -- leaving a 5 percent net profit.

When hardware and direct labor costs are reduced by $0.85 per watt, the gross profit margin of the business must increase to 56 percent to maintain the same 5 percent net profit. Installers must increase their gross margins -- keeping gross margins steady is a recipe for disaster. Moreover, expenses tend to increase faster than gross sales, so increased sales volumes do not compensate for stable gross margins.

Finally, some people in the industry think the elimination of the ITC is a good thing. I hear comments that installer margins are too big, there are plenty of inefficiencies that are easy to eliminate, or that incentives are inherently bad. Invariably, I find that these opinions are either naive (from people who have not operated a residential solar company), or promulgated by individuals who prefer a different business model for solar deployment in the U.S. -- such as utility-scale solar, or commercial installations where MACRs and Section 48 of the tax code still provide a 30 percent benefit in 2017.

Residential installers have a little over a year to take two specific actions in the face of this ITC elimination. First, we need to continue to support the efforts of SEIA, Vote Solar and state solar organizations to extend the 30 percent ITC for residential solar, including solar thermal.

Convincing Republican senators and representatives that residential solar is a local job engine is key to this effort.

Second, we need to provide guidance to our manufacturing partners on ways to reduce total installed system costs -- not just the cost of their respective components. Without these two actions, it is simply wishful thinking that the residential solar industry will be okay in 2017.

***

Barry Cinnamon runs Cinnamon Solar, a local San Jose installer, and Spice Solar, a provider of technology and components for integrated racking solar modules. He is a Board of Directors alternate at SEIA, former president of CALSEIA, and founder of Westinghouse/Akeena Solar.

42

42

15

15

9

9