In keeping with GTM holiday tradition, here's the latest list of profitable publicly held fuel cell firms:

1.

2.

3.

The biggest news in the 2018 fuel cell world was the reinstatement of the 30 percent federal Investment Tax Credit for fuel cells. That, and the long-promised IPO of VC-funded Bloom Energy, which now boasts the largest market cap and revenues of any fuel cell firm, by far.

But wait. Hold the presses. Germany’s SFC Energy, a maker of portable direct methanol fuel cells, could make history as the inaugural member of our list with just a bit of profit in this year’s final quarter. Stay tuned.

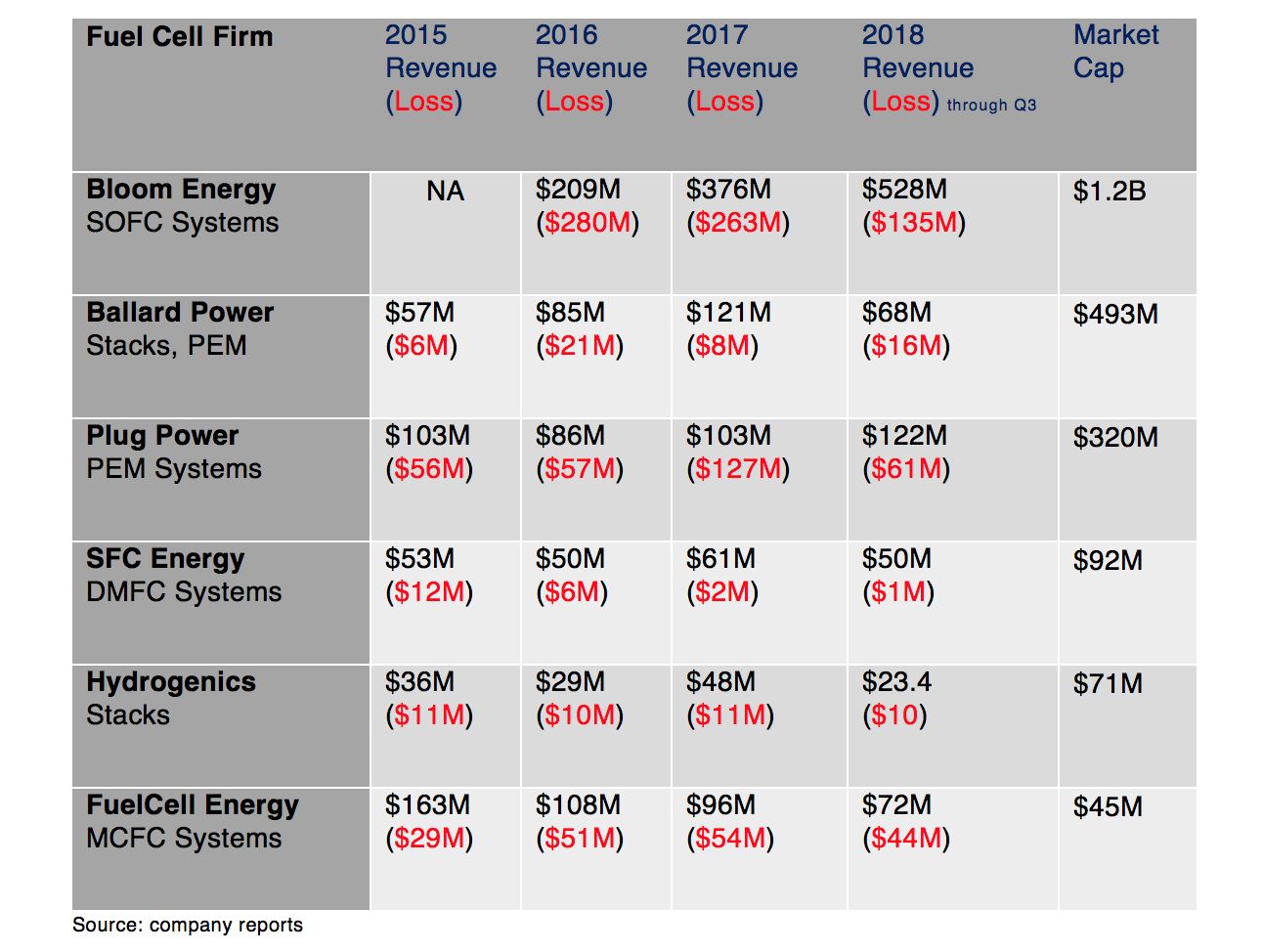

Before we celebrate, take a look at the financial results of the public fuel cell firms over the last few years.

In most cases and with the possible exception of Bloom, it’s the usual grim story with year-over-year revenue and losses headed in the wrong direction.

In addition to a lack of profit, a recurring theme in the stock performance of these public fuel-cell firms is an initial burst of buoyancy and hype followed by a dreary slog into life as a small-cap company.

A brief fuel cell tech rundown

Fuel cells electrochemically convert hydrogen and oxygen into DC electricity.

Fuel cells employ an assortment of electrolytes, catalysts and temperatures. But in almost all cases, the membranes are expensive to fabricate, and the technologies require precious metal catalysts (typically platinum or palladium) or high process temperatures. Input fuels range from natural gas to methanol to hydrogen. There are ongoing R&D and DOE efforts to reduce the need for expensive metals and to improve the reliability and lifetime of the fuel cell stack.

Common technologies include proton exchange membrane (PEM), solid oxide (SOFC), phosphoric acid (PAFC) and molten carbonate (MCFC). There are a number of other technologies, all adept at destroying investor capital. GE, GM, Hyundai, Honda, Johnson Matthey, Panasonic, Siemens, Samsung, LG, Sharp, Toshiba and Toyota have all invested in and, in many cases, abandoned fuel cell technology.

Bloom Energy, Doosan and FuelCell Energy build large stationary fuel cells, using SOFC, PAFC and MCFC technologies, respectively. Plug Power, on the other hand, targets its PEM fuel cell system at powering forklifts and other vehicles in the enormous materials handling market.

While Bloom's and FuelCell Energy's equipment runs on natural gas, Plug Power's PEM fuels cells run on "five nines" hydrogen and work most productively with a hydrogen infrastructure at the customer site.

State incentives in California and elsewhere have driven large stationary fuel cell installations, while other locales consider fuel cells for microgrids and grid resiliency. Fuel cells are again eligible for the 30 percent federal Investment Tax Credit, a lifesaver for most firms.

Fuel cell shipments globally were about 670 megawatts in 2017, up from 500 megawatts in 2016, and the market is growing — as is the list of Fortune 500 fuel cell customers. In fact, almost 10 percent of Fortune 500 firms use fuel cells for stationary or motive power.

The stationary fuel cell market will grow 18 percent year-over-year to reach more than $2.1 billion by the end of 2019, according to research firm Fact.MR. Technavio pegs the annual growth rate of the fuel cell market at nearly 28 percent through 2023.

Market player highs and lows in 2018

Bloom Energy: Bloom Energy finally went public in July of 2018 after a dozen years of suspense and more than $1.2 billion invested. Bloom’s stock soared to double its $15 IPO price but soon fell to earth and is now well below its IPO price in a bleak time for most stocks.

Bloom partnered with Key Equipment Finance to help finance more than $100 million in fuel cell projects and with SK Engineering and Construction to expand its sales channel in South Korea. Battery storage was included in 27 of Home Depot's fuel cell projects with Bloom in 2018. Bloom continues to blaze trails in powering data centers and other critical applications for a wide swath of Fortune 500 firms.

Bloom has faced significant losses in the past two years — $263 million on revenues of $376 million in 2017, and $280 million on revenues of $209 million in 2016. In the first three quarters of 2018, Bloom reported a net loss of $135 million on revenues of $528 million.

Bloom claims its system emits 756 pounds of CO2 per megawatt-hour compared to 960 pounds of CO2 per megawatt-hour for the average natural gas plant and 2,280 pounds of CO2 per megawatt-hour for a coal plant.

Posco Energy: Korea’s Posco Energy is a fossil fuel independent power producer and a division of steelmaking giant Posco. It claims to be the world’s largest fuel cell manufacturer, with a 50-megawatt annual production capacity and 160 megawatts installed across South Korea.

But even a quasi-state-run company with a big factory can’t make a profit in fuel cells: Posco intends to exit from the fuel cell business in the near future, according to various reports, after posting $292 million in accumulated losses since 2007.

Doosan Fuel Cell America builds and markets a 460-kilowatt phosphoric acid fuel cell based on technology acquired from UTC. The Korean firm has a partnership with Wells Fargo Vendor Financial Services to finance its systems. The stationary fuel cell puts out a claimed CO2 (electric only) emission of 998 pounds per megawatt-hour and claims a 10-year stack life. Customers include Cox Communications and Coca-Cola.

FuelCell Energy acquired a 14.9-megawatt fuel cell park from Dominion Energy in a $37 million deal with the financial help of the Connecticut Green Bank. It’s part of the firm’s strategy to hold and grow its generation assets and capture more consistent revenues and cash, in this case from a power-purchase agreement with Connecticut Light & Power.

Connecticut’s recent clean energy RFP awarded 22 megawatts to FuelCell, along with 20 megawatts for Doosan and 10 megawatts for Bloom.

Despite these and other wins, FuelCell continues to lose money. Its stock price is down to $0.52 per share from $1.86 per share one year ago.

Ballard Power announced a strategic collaboration with Weichai Power, a Chinese engine and auto parts conglomerate. Weichai agreed to purchase a 19.9 percent stake in Ballard for $163 million, a 15 percent premium to the stock price. Ballard’s other China partner, Broad-Ocean, agreed to purchase $20 million in shares to maintain its 9.9 percent ownership level — so, as GTM has reported, Ballard is flush with cash.

In its 22nd year as a profitless public company, Ballard had a 2018 replete with stagnant growth and mounting losses.

Plug Power acquired American Fuel Cell (AFC) in 2018 and is integrating AFC’s thinner metal plate technology into its fuel cells, saving volume in space-constrained applications. Plug opened a second manufacturing facility in upstate New York.

Plug upped its full-year 2018 revenue guidance to between $175 million and $190 million from the previously forecasted revenue range of $155 million to $180 million.

Fuji Electric: Fuji Electric has been selling a 100-kilowatt phosphoric acid fuel cell since 1998.

Germany’s SFC Energy, a contender for the inaugural spot on the profitable fuel cell company list, might eke out some earnings in 2018 on sales of its portable fuel cells for consumer, oil and gas, and industry. SFC added lithium-ion batteries to some of its hybrid generators this year.

Europe’s SOLIDpower installed its 1,000 solid oxide fuel cell in 2018, a compact 1.5-kilowatt unit with hot water capabilities for home and office.

LG, the world’s largest builder of lithium-ion batteries, just shut down the 70-employee LG Fuel Cell Systems (the former Rolls-Royce Fuel Cell Systems) after gaining $18 million in government grants and investing hundreds of millions in development. LG has no plans for further development of the technology, according to The Cleveland Plain Dealer.

How do you assess the health of an industry?

How do you assess the health of an industry? Is it whether it's growing? Profitable? Innovating? Winning market share from competing technologies? Driving down costs?

Fuel cells are not faring too well by these parameters.

Wind, solar, efficiency and storage are leading the energy transition away from carbon, but Matthew Klippenstein, Plug In BC EV adviser and fuel cell industry analyst, contends that fuel cells, renewable hydrogen and liquid energy carriers, next-generation nuclear, biofuels and other technologies still have their contributions to make.

Klippenstein suggests that the fuel cell sector’s growth “continues to track, and possibly exceed, the earlier trajectories for solar and wind energy,” and “dismissing hydrogen and fuel cells would be as premature as dismissing solar in the early 2000s, or wind in the mid-1990s.”

But the solar industry took advantage of the maturity of the silicon industry and its Moore’s law-esque scaling. The wind industry has the swept-area law, and lithium-ion has automated 20-gigawatt-hour factories. Is there any equivalent scaling mechanism in fuel cells?

Klippenstein believes that Toyota, Hyundai and others could drive production of hundreds of thousands of stacks for fuel cell EVs in the coming years — and that will serve as the catalyst for scaling this industry to profitable distributed generation from natural gas and hydrogen.

In the meantime, we’ll keep waiting for profits.

41

41

15

15

9

9