In September, the Department of Energy’s SunShot Initiative celebrated that its 2020 price target for utility-scale solar had been achieved three years early.

But the triumph appears to have been short-lived.

An analysis from the DOE’s National Renewable Energy Laboratory found that the average price for utility-scale solar recently fell to less than $1.00 per watt and below 6 cents per kilowatt-hour -- without subsidies. GTM Research calculated that U.S. utility-scale fixed-tilt solar system pricing fell below $1 per watt earlier in the year, using a different methodology.

However, a new GTM Research report finds that the average fixed-tilt utility-scale solar price has since edged back above of the SunShot price target, amid market uncertainty surrounding the Section 201 solar trade case.

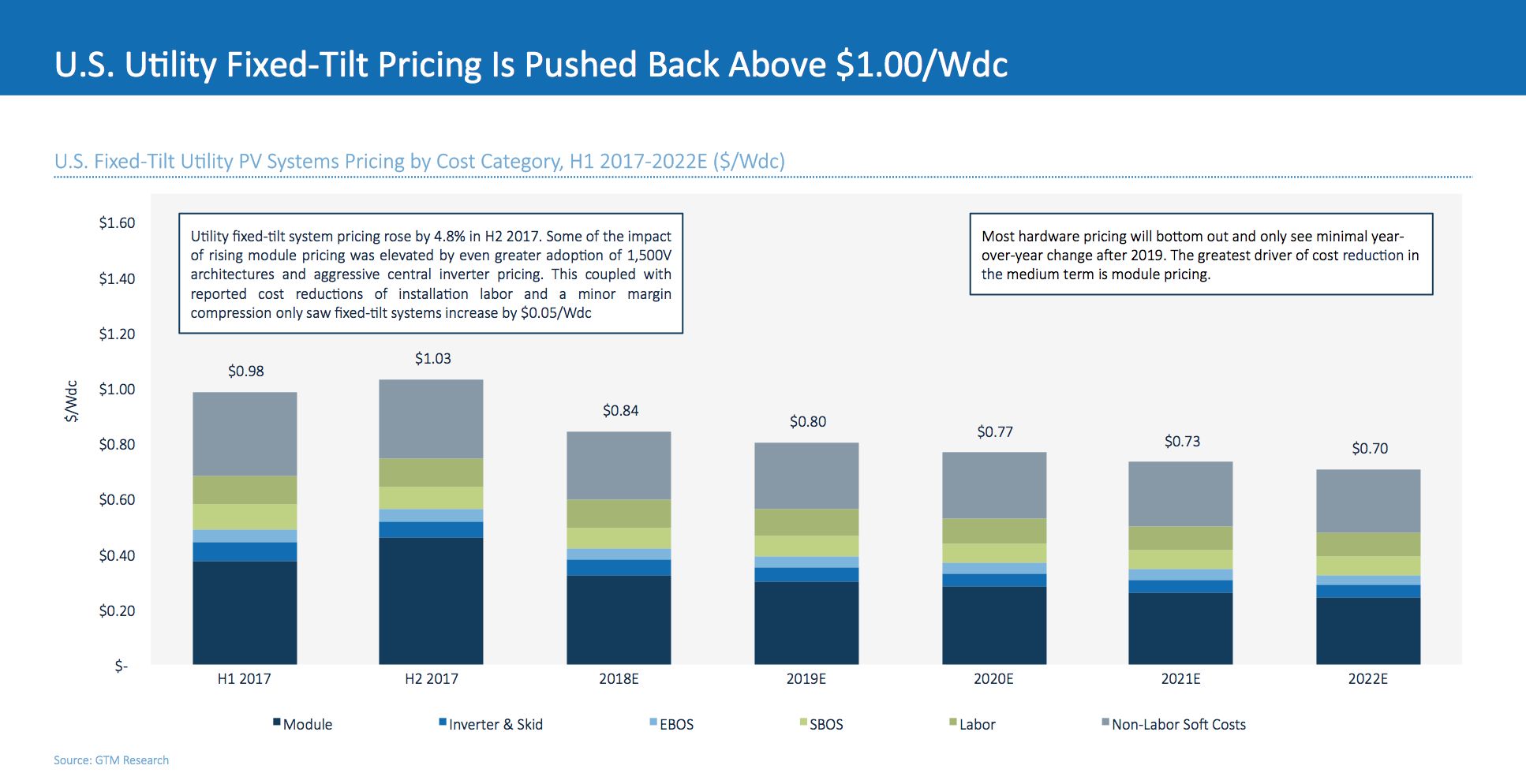

In the first half of 2017, the average fixed-tilt system was priced at 98 cents per watt (all figures for direct current, or DC) with engineering, procurement and construction (EPC) pricing below $1.00 per watt in 26 states. Today, average pricing for fixed-tilt systems sits at $1.03 per watt, with only six states seeing average pricing below the $1.00-per-watt mark.

GTM forecasts for 2018 and beyond show average system prices falling again. But notably, the base-case forecast does not include any future impacts from Section 201 tariffs, because the remedies that will be applied are still unknown.

Prices increase across all segments for the first time in a decade

The recent price increase stems from a rush to procure “tariff-free” solar panels over the summer with the potential for new tariffs looming. U.S. developers have specifically been looking to procure crystalline-silicon solar (CSPV) modules from manufacturers in Malaysia, Vietnam and Thailand, which are the primary vendors in the U.S. market today, but had a limited amount of available capacity this fall as the Section 201 trade case intensified. The shortage stems from the fact that their product is purchased several quarters in advance.

Modules sourced from China and Taiwan are less attractive to U.S. developers, because they’re already subject to anti-dumping and countervailing duties from previous trade cases.

“Installers and EPCs are scrounging to get this tariff-free capacity from modules that aren’t sourced from China or Taiwan delivered before whenever President Trump would sign new tariffs into law,” said Benjamin Gallagher, GTM solar analyst and lead author of the new report, U.S. PV System Pricing, H2 2017.

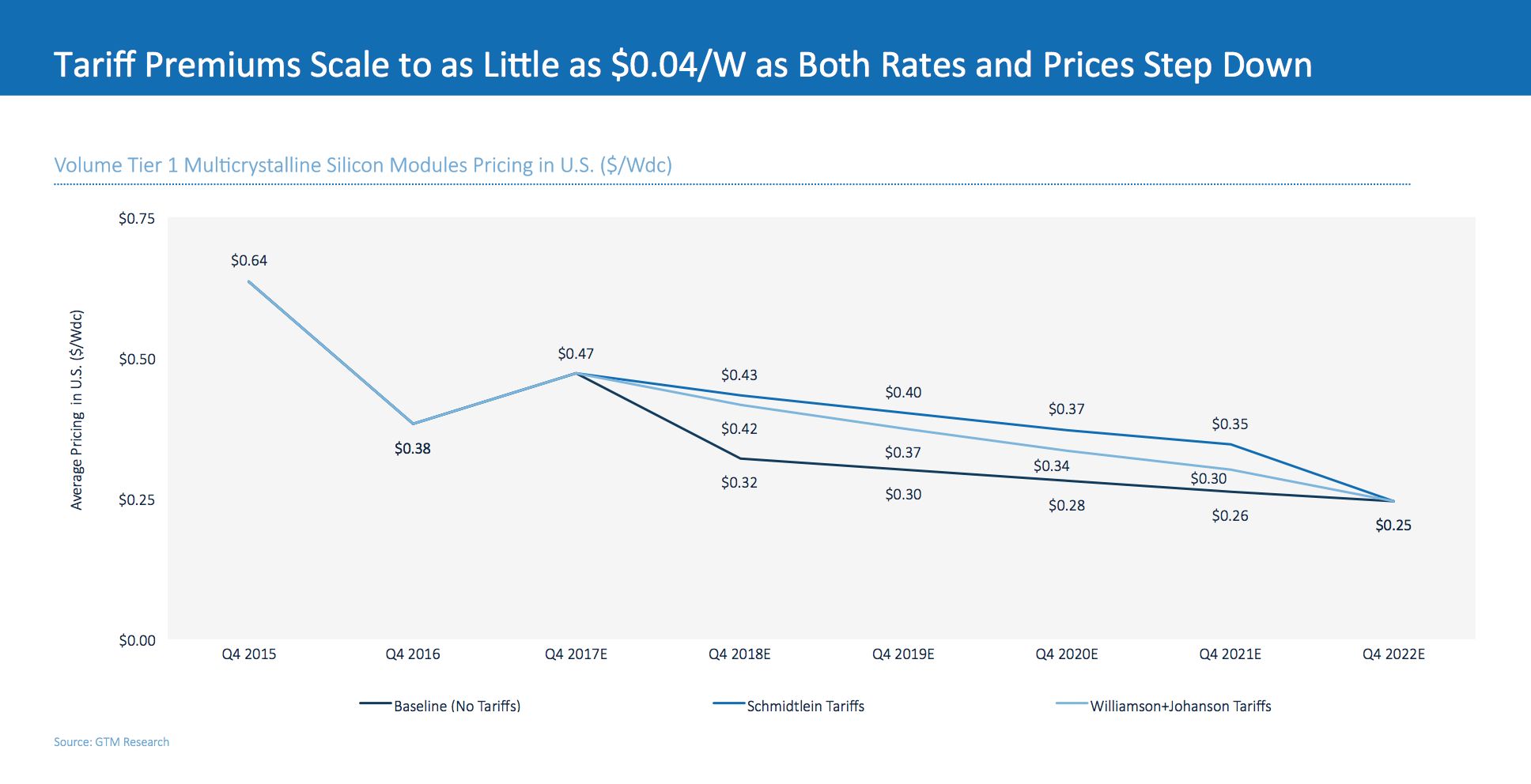

If President Trump, who has the final say, decides to put new tariffs in place under the Suniva and SolarWorld Americas Section 201 trade petition, module prices will increase in every major CSPV panel manufacturing market except for Singapore. The anticipatory spike in demand has already caused module prices in the U.S. to increase from around 33 cents in the first quarter of 2017, to 47 cents in the fourth quarter of 2017, according to GTM Research.

Chaos in the U.S. module market caused the average system price in all solar market segments to increase for the first time in more than decade. From the first half to the second half of the year, prices rose from $2.92 per watt to $2.96 per watt in the residential sector, and from $1.54 per watt to $1.56 per watt in the commercial sector.

Module prices are expected to stabilize and start to decline if a modest tariff is put in place, in line with proposals put forward by the U.S International Trade Commission (U.S. ITC). But the outcome of the case is currently up in the air.

Trump hasn't officially weighed in on the issue, although U.S. Trade Representative Robert Lighthizer has asked that the U.S. ITC issue an additional report on the "unforeseen developments" that led to an increase in foreign solar imports, possibly seeking to stave off a policy reversal at the World Trade Organization. The commission has 30 days to produce the report, which moves the deadline for Trump to impose tariffs or quotas from January 12 to January 26.

In the meantime, module prices are likely to remain high.

Balance-of-system vendors come to the rescue

While the recent price spike sends a shock through the U.S. solar market, the more surprising takeaway is that the price increase could had been much worse if it weren’t for the efforts of balance-of-system technology providers, said Gallagher.

“Aggressive hardware pricing, especially in the inverter and racking markets, reduced the overall impact of high module prices,” the report states. For utility-scale PV, for instance, more widespread adoption of 1,500-volt architectures has reduced installation labor and electrical balance-of-system costs.

“There are individual elements in each cost bucket spurring these cost declines that are all part of larger, aggressive pricing environment,” said Gallagher. “There are companies bringing new technologies and new designs to market, and most of that is being driven by differentiating themselves in an increasingly commoditized space."

The market is seeing the fruits from many months of labor that predate the Section 201 case, but have come just in time to soften the blow from it. The fact that a module price increase from 33 cents per watt to 47 cents per watt only resulted in a 5-cent increase in fixed-tilt utility-scale prices is a testament to the cost-cutting efforts in other areas of the industry.

“You would have seen higher overall system pricing if it wasn’t for these balance-of-system vendors pricing aggressively in the market,” Gallagher said. “They’ve come to the rescue, so to speak, to mitigate a huge inflation in pricing that would have come in the second half of this year.”

Unfortunately, these vendors will be under more pressure to offer even lower prices going forward, squeezing their margins further, especially as new tariffs are confirmed. But the good news for the broader U.S. market is that there is still some flexibility in hardware markets and at EPC firms to help push project prices lower.

“Even with system costs and pricing falling so much over the past 10 years, stakeholders are still able to squeeze out a few pennies,” Gallagher said.

He added that the U.S. ITC’s proposed 30 percent tariff on modules would result in an approximately 10-cent increase, which would bring module prices to around 45 cents per watt. That's similar to current module pricing, as well as to project price levels seen in the second half of 2016.

The 30 percent tariff scenario is "setting the clock back a year, but it’s not the end of the world,” Gallagher said.

But price isn’t the only relevant factor.

“Markets are built upon assumptions around risk. Having this total uncertainly about what the tariffs may be is bad for the industry. That’s unequivocal," Gallagher said. "System pricing and module pricing rising is a bad signal to investors. It’s a bad signal to people who were on the fence with regard to funding or investing in PV or renewable energy more broadly.”

Residential and commercial solar struggle with familiar issues

An uptick in pricing isn’t good for new solar buyers, or for more traditional investors looking to enter the market for the first time. And it’s certainly bad news for individual component manufacturers that need a clear forecast on their sales revenues. But this is more of an issue related to the anxiety around how new tariffs will be implemented, rather than the recent price spike, according to Gallagher.

The latest PV pricing report also shows -- Section 201 aside -- that certain segments of the solar market continue to struggle with the issues that have plagued them in the past. Residential solar, for instance, continues to cope with high soft costs associated with sales, marketing, design, engineering and installation labor. Customer-acquisition costs actually increased from the first half to the second half of 2017.

A 30 percent tariff on modules would have less of an impact on residential solar than utility-scale, because the module makes up a smaller share of the overall cost stack in that space. But a higher module price certainly wouldn’t help residential solar companies as they strive to cut soft costs with few signs of improvement.

Commercial solar developers are in an even tougher bind. In residential, there is at least the promise of reducing soft costs. But that golden ticket just doesn’t exist for commercial EPCs. Their ability to reduce internal construction costs or find cheaper hardware is constrained due to project size and available financing methods.

To cope with new tariffs, EPCs report that they plan to change their relationships with subcontractors by prioritizing lowest-cost service, while potentially cutting the fixed costs of full-time employees internally.

GTM Research’s latest pricing report reveals that while project prices have gone up, underlying solar market trends haven’t changed substantially in light of the Section 201 case. For better or for worse, the pressure to cut costs persists across all market segments.

In this context, the Section 201 case may not be a death knell, at least not if one of the U.S. ITC’s proposed remedies is accepted. But it is already proving to be a setback.

“In the broader transition away from being highly policy-driven to primarily market-driven, this is a hiccup that the solar industry does not need,” said Gallagher.

***

Learn more about GTM Research's new pricing report here.

42

42

15

15

9

9