Three years ago, I posed the question: Is the SolarCity model the only way to scale residential solar?

Based on the way the industry has progressed since then, the answer is a resounding no. While the vertically integrated models of SolarCity and Vivint once seemed like they would forever dominate the residential solar market, the events of the past few years point to a very different conclusion.

In fact, they bring up a different question: Should residential installers try to scale nationally at all?

Putting aside these two companies, there are a number of others that have failed in their attempts to rapidly grow.

- California installer Verengo, once the second-largest residential installer, went bankrupt after its short-lived East Coast expansion.

- Direct Energy Solar and now-defunct NRG Home Solar tried and failed to move from the East Coast into the California market.

- Even a few companies that didn’t try to expand to new regions, such as Next Step Living in Massachusetts and American Solar Direct in California, grew too quickly in one market and ended up going out of business.

- Several installers that specialize in door-to-door sales, such as Brite Energy and Suncrest Solar, had some of the quickest boom-and-bust cycles I’ve ever seen. Don’t recognize those names? Exactly.

These failures can also negatively impact finance providers that depend on the success of their large installer partners -- companies like Sungevity, OneRoof Energy and Spruce Finance, the latter being the only one of the three that (barely) still exists.

Source: GTM Research U.S. Downstream Distributed Solar Service

Source: GTM Research U.S. Downstream Distributed Solar Service

There are two major problems installers face when trying to expand. First, they have trouble adjusting to different cost structures, local requirements, and the cultural nuances of selling in new markets.

Second, it requires a lot of money spent on customer acquisition, in addition to the initial cost of expansion. Small, local installers have the cheapest cost of customer acquisition because they rely mostly on referrals and community events. Operating on a larger scale typically requires huge investments in marketing and partnerships or, in the case of the door-to-door companies, incentivizing salespeople. This leads to thin margins at best.

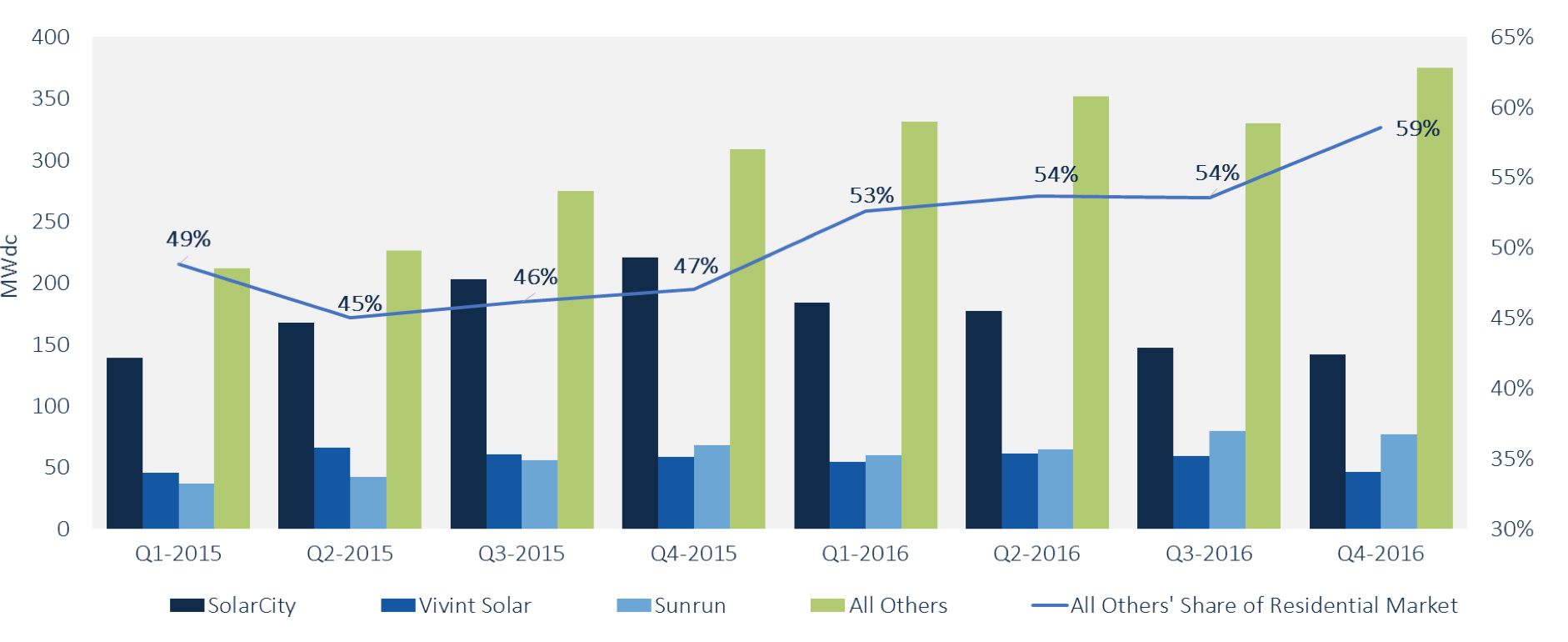

One could make the argument that SolarCity and Vivint actually did succeed in scaling installation nationally, but a large market share does not equate to success. They were only able to grow so quickly because of their access to financing, and it was that third-party financing combined with the rising cost of customer acquisition that prevented these companies from being profitable. Both have slowed the pace of installations to refocus on cutting costs.

But even if installers shouldn’t expand that much, there is still a place for other national companies in the residential solar market. Customer acquisition in particular is an area that could use more innovation and investment on a larger scale. We’re already starting to see installers outsource sales, especially as costs continue to rise and referrals become harder to obtain in mature markets.

Whether it’s originators selling door-to-door, leading in-store sales, or running advertising campaigns, this piece of the value chain is much better suited to a national business model than installation. And there is still an opportunity for some companies -- ahem, Tesla -- to pivot to a sales-only model.

Sales, financing and other services may be successful as national businesses, but the best way for the industry as a whole to grow sustainably is for installation to be left to local companies who can better serve the needs of customers while turning a profit for themselves.

***

Nicole Litvak is a senior solar analyst at GTM Research.

Get access to all of GTM Research's U.S residential solar data and reports with a subscription to the U.S. Downstream Distributed Solar Service.

41

41

15

15

9

9