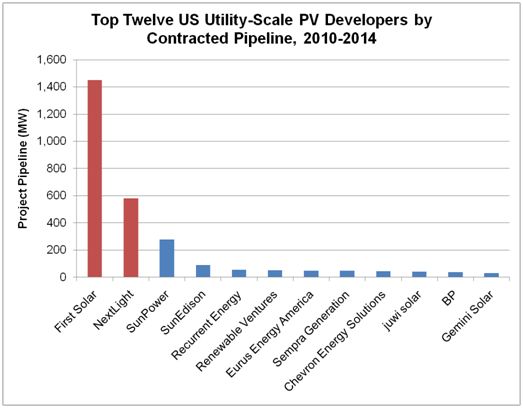

This morning, First Solar announced the acquisition of Nextlight Renewable Power, LLC for about $285 million. In doing so, it combined the largest utility-scale PV project pipeline in the U.S. with the second largest. First Solar already had over 1.4 GW in development through a mix of multi-hundred megawatt projects (Sunlight, Stateline and Topaz) and a number of smaller projects. Nextlight, which was founded by Energy Capital Partners, a private equity firm with over $3 billion in funds under management, had a 570 MW contracted pipeline of mostly large-scale projects which have now been added to First Solar's coffers.

First Solar's downstream integration strategy has largely been built around the acquisition of expertise and pipelines. In 2007 it acquired Turner Renewable Energy, gaining an internal EPC team. This was followed by two pipeline acquisitions: Optisolar in 2009 and Edison Mission Group earlier this year.

Today's acquisition does two things for First Solar. First, it builds First Solar's development and EPC team. One of Nextlight's biggest selling points was its management team, which has deep roots in the energy project development business. If First Solar is shifting its resources more heavily toward the downstream side of the market, it will benefit from a larger project development experience base.

Second, it ensures First Solar's near-term dominance in the U.S. utility-scale project development game. First Solar's contracted pipeline already dwarfed its next competitor (which happened to be Nextlight), but now we estimate it to be more than seven times the size of the next largest U.S. pipeline.

Source: GTM Research

Aside from the impact on First Solar's business, this can be viewed as an incremental negative for other module suppliers, particularly SunPower. By locking up a large proportion of contracted utility-scale projects in the U.S. to use its own modules, First Solar is effectively limiting the total market for its upstream competitors. The utility-scale market in the U.S. has thus far been a tale of two suppliers: First Solar and SunPower. Until this announcement, Nextlight was rumored to be considering using SunPower's high efficiency crystalline modules on one-axis trackers for a number of its projects -- but that possibility has now disappeared.

But not to fear for SunPower, because it has been focusing its downstream efforts on the high-return Mediterranean markets, as evidenced by its recent acquisition of SunRay. This difference between the downstream efforts of each company reflects a dynamic that GTM Research has noted for some time now. In markets with high fixed incentives such as Spain, Italy, Greece and France, project developers are easily able to meet investor threshold returns at a range of reasonable module prices. Equity investors will not base an investment decision on the difference between, say, 20 percent and 22 percent internal rates of return (IRRs). The developer's best strategy, then, is to maximize gross project returns -- to maximize the total value of funds upon which it can earn attractive returns. In contrast, markets such as the United States and Germany, in which investor returns are tighter and incentives smaller, place greater emphasis on maximizing equity IRRs. In order to meet threshold rates of return, developers must seek to cut project costs as much as possible.

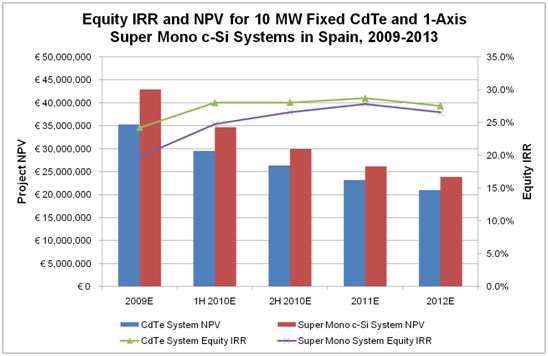

Given current pricing and efficiency, lower cost, lower efficiency thin-film modules (particularly First Solar's CdTe) tend to provide slightly higher equity IRRs. But higher cost, higher efficiency crystalline silicon modules (such as SunPower's "Super Mono c-Si" modules) offer larger gross returns. The figure below displays the differential between two representative 10 MW ground mount systems in Spain, one using CdTe modules on a fixed substructure and the other using Super Mono c-Si modules on a 1-axis tracking system. Over time, gross returns (represented by project NPV) decline along with the Spanish feed-in tariff but falling system prices enable steady equity IRRs.

Source: GTM Research

This serves as a partial explanation for First Solar's dominance, both in terms of modules and project development, in the U.S. and German utility-scale PV markets. It also partially explains SunPower's focus on growing Mediterranean countries and other high feed-in tariff markets for its utility-scale project development operations. Over time, this differential between technologies may fall and project pipelines could become more evenly spread amongst technologies and suppliers. But in the meantime, watch for First Solar to maintain its position atop all suppliers and developers in the U.S. utility-scale PV market.

As a final note, it is important to remember that there are two reasons why the window of opportunity in the U.S. is far from closing for other module suppliers. First, the utility-scale market in the U.S. remains nascent and a true ramp-up will far exceed the 2,000 MW under contract with First Solar. In other words, there is still plenty of room for entry. Second, utilities may ultimately become wary of increasing their exposure to a single developer (i.e., First Solar) in order to meet their renewable energy or solar mandates. As a result, we may begin to see utilities with existing First Solar contracts selecting other developers in future RFP cycles.

41

41

15

15

9

9