Note: We'll be discussing the PV inverter landscape and the challenges associated with PV inverters during our PV Inverter and BOS track at Greentech Media's 6th Annual Solar Summit.

The Basics of Advanced Energy’s Acquisition of REFUsol

Early on Tuesday, April 9, 2013, Advanced Energy announced the acquisition of Metzingen, Germany-based inverter supplier REFUsol for €59 million ($77 million) in cash and €9 million ($12 million) in debt and reducing working capital by €1.8 million ($2.4 million). REFUsol focuses on commercial solar inverter products, including three-phase string inverters, primarily for European markets and, according to GTM Research estimates, was the fourth largest inverter supplier by megawatt shipments in 2012 and had approximately €170 million ($223 million) in revenues in 2011. Advanced Energy reached 878 megawatts in shipments in 2012 -- enough to secure its position as the sixth largest inverter supplier in 2012.

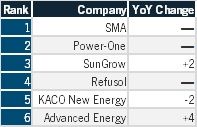

Figure 1: Top Inverter Suppliers by 2012, Global Shipments in MW

Source: GTM Research's report Global PV Inverter Landscape, 2013

The Backdrop of a Tumultuous Inverter Supply Landscape

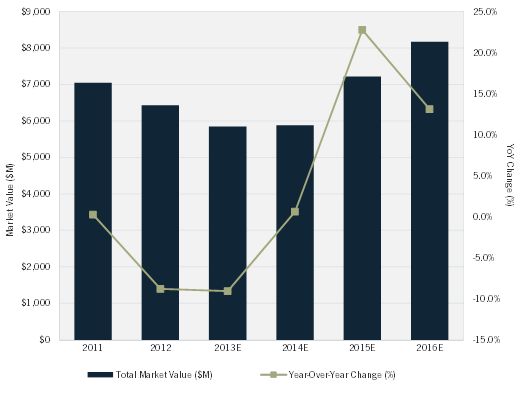

In our soon-to-be-published Global PV Inverter Landscape, 2013 report, we highlight the significant headwinds facing inverter suppliers. Falling European markets, coupled with failed entries into the new big three markets of China, Japan and the U.S., have exacerbated the desperate environment for incumbent inverter suppliers. With demand toward more price-sensitive markets and the recent explosion of inverter suppliers, inverter prices and margins have taken a major hit -- to the point where some diversified suppliers speak more of sales of other services like EPC and O&M than inverter hardware sales. Double-digit percentage hits to inverter pricing across all market segments have led to diminishing revenues from inverter sales despite growth in terms of megawatts shipped.

Figure 2: Forecasted Global Market Value of PV Inverters in $M, 2011-2016

Source: GTM Research's report Global PV Inverter Landscape, 2013

The widely publicized liquidation of Satcon and pullback by Siemens only inject further turmoil into the market, with “bankability” finally emerging as a key inverter purchasing concern for all installers. Our prediction for further market consolidation, whether by other acquisitions or via quiet divestment, should come as no surprise. In the past two quarters, we’ve already seen quite a few events, including:

- SMA's 72.5 percent equity stake in Chinese supplier Zeversolar

- Satcon bankruptcy filing, eventually leading to liquidation

- Siemens' pull back from solar inverter manufacturing

- Oelmaier acquisition by Lehner Agrar

- Diehl acquisition by mutares AG

- Sunways' refocus on customization rather than in-house inverter production

- Pairan insolvency

- Market exits by module-level power electronics firms like eIQ and Azuray

Further divestment by European and Asian manufacturers should be expected, as should struggling module-level power electronics companies reaching out for a bankable parent, creating a frothy environment for M&A activity.

Plugging Holes Through Acquisition

On paper, acquisition solves a number of concerns for both parties -- so much so that this analyst wonders why he didn’t make the prediction. We point out these concerns in the following excerpt from our competitive evaluation of inverter suppliers on cost structure, bankability and growth prospects.

Figure 3: 2013-2014 Prospects for REFUsol and Advanced Energy (Pre-Acquisition)

Source: GTM Research's report Global PV Inverter Landscape, 2013

To summarize, Advanced Energy’s primary strength has been its ability to ride the U.S. market, with a number-two slot in market share in 2012, overshadowed only by SMA with Satcon as a close follower. With Satcon’s demise, Advanced Energy was one of the best positioned to grab additional share. However, we predicted that Advanced Energy’s dependence on North America would soon become a liability, primarily due to:

- Significant pricing pressure due to new European and industrial conglomerate entrants in the U.S. utility-scale inverter market

- Lagging technology offerings in the small commercial space as rivals SMA, Power-One, and Chint (as well as REFUsol) introduce three-phase transformerless string inverters into the U.S. market

- Threatened commercial shares with the predicted growth in three-phase string inverter adoption in North America

- Weak entrance into other markets due to a lack of 50 Hz product

Meanwhile, REFUsol’s significant growth has come as a result of strong European adoption due to a compelling and well-regarded commercial product portfolio. However, REFUsol’s leadership would soon become problematic, due to:

- European markets that make up REFUsol’s core have become hyper-competitive as falling incentives and growing desperation grips much of the European industry.

- Market penetration outside of Europe has been minimal, especially in key regions like the U.S. and India, despite significant investment

In short, Advanced Energy gains strong products and distribution in areas where it has been lagging, and REFUsol’s parent company likely saw a clean exit from the solar industry and an opportunity to refocus on its core products, taking a similar stance as the one staked out by Diehl Controls in the sales of its inverter business. Furthermore, since REFUsol relied on its sister companies within the Prettl group for manufacturing, it carries no manufacturing assets into the deal.

Ongoing Concerns and Question Marks for Advanced Energy

The acquisition certainly improves Advanced Energy’s competitive positioning considerably, but doesn’t change the fundamental dynamics in the inverter industry. Pricing will still fall as the result of new entrants and desperate incumbents and demand continues to diffuse into emerging markets, where both Advanced Energy and REFUsol still have a long way to go. While the products and distribution are accretive, rapid and successful integration will be necessary to prevent a fall in the North American and European markets. Near and medium term concerns will be:

- Bankability: Advanced Energy is now more highly leveraged on its solar inverter business, which may be a concern if the downturn in global inverter markets is worse than expected in 2013 and 2014. Both companies, however, have had a solid industry reputation in terms of reliability and quality.

- Increased competition in the U.S. market: While REFUsol’s products allow Advanced Energy to compete in the new three-phase commercial string front in the North American theater, this does little to stem the tide of new entrants in the utility-scale inverter market.

- Little penetration in China and Japan: REFUsol’s 50 Hz product is a first step toward Advanced Energy entering new markets, but neither have had much success in penetrating the domestic-dominated markets of China and Japan, due to pricing and certification issues, respectively. Advanced Energy is attempting to enter the Chinese market through partner SGEG, and REFUsol also tried to enter the Chinese market with a proprietary product.

How the Acquisition Stacks

The acquisition certainly shores up significant weaknesses in Advanced Energy’s offerings, but the company still needs to successfully integrate REFUsol, as well as develop a coherent and successful emerging markets strategy -- no easy task considering a host of other suppliers doing the same. However, Advanced Energy does have a track record of success, with its star rising after a successful merger with PV Powered in 2010. Furthermore, the acquisition comes at a fair discount. REFUsol's revenues were €170 million ($222 million) in 2011 (though with a likely drop in 2012). Nevertheless, Advanced Energy was able to take on the portfolio for just €59 million ($77 million) in cash and €9 million ($12 million) in debt -- a valuation that was certainly built on near-term risk and prospects rather than historical performance.

Ultimately, while we see stronger prospects for the combined portfolio, near-term European declines, fierce competition in the U.S., and slow growth of emerging markets will hold back the company in 2013. While integration and execution after the acquisition will determine longer-term prospects, Advanced Energy has addressed key weaknesses and has new powerful assets with which to weather the oncoming inverter industry shakeout. We don't believe that SMA and Power-One are quaking in fear just yet, but it does add significant resistance to their U.S. expansion and strengthens a major global competitor.

Senior Editor Stephen Lacey asks Tucker Ruberti, Director of Segment Marketing at AE Solar Energy, about the acquisition:

41

41

15

15

9

9