Whether booming off-grid power demand in emerging markets is met with grid extension or distributed renewables will be central to the growth story of the global clean-power sector.

As the technological and financial tool kit for providing affordable, reliable, appropriate and clean power to every household and business continues to expand, deployments of off-grid, decentralized, renewable energy systems will take an increasingly larger bite out of present and future power demand on the grid in countries that represent over one-third of the world’s population.

On-grid and off-grid power service offerings will increasingly see convergence as next-generation distributed energy service companies continue to evolve and scale. Because the future grid will be increasingly renewable, low-cost, digitally managed and, eventually, demand-following, the diffusion of off-grid systems is still highly interrelated with the rest of the grid.

Relatedly, low-energy-access countries’ urgent need for large utility-scale generation and grid infrastructure upgrades cannot be overstated; while solar lanterns and solar home systems (SHS) are an effective and targeted solution for rural households, small-scale distributed solutions cannot power industrialization and economic growth.

In recent years, sector stakeholders have increasingly rallied around the flag of integrated electrification planning, which we’ve previously dubbed the “growth game-changer” of the next decade of the decentralized renewables market. Put simply, integrated electrification planning efficiently allocates shares of the remaining addressable market for new electrification connections to different technology solutions (think grid extension projects, standalone solutions like solar home systems and, increasingly, renewable minigrids).

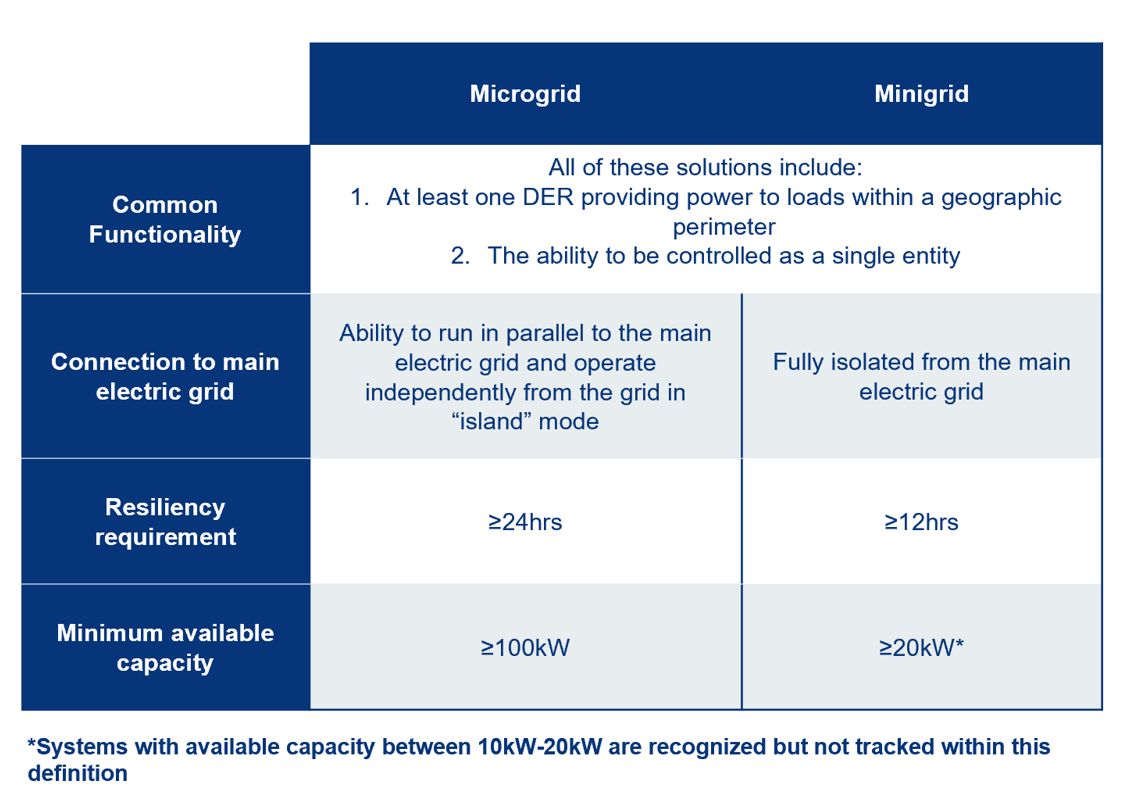

Wood Mackenzie's working definition of minigrids

Source: Wood Mackenzie

These planning exercises are capitalizing on advances in tools including geospatial surveying, new granular demographic data layers, customer surveys, historical electricity consumption data and artificial intelligence to optimize the extension of electricity service to homes and businesses at least cost and with maximum speed.

Countries including Togo, Senegal, Nepal and Kenya that have begun implementing integrated electrification plans will minimize connection costs, stranded asset risk and unnecessary competition while maximizing the customer footprint and growing demand with appropriate solutions for each offtaker.

Minigrids the lowest-cost option for many

Minigrids have an increasingly pivotal — and often underestimated — role to play in the future electricity mix envisioned in integrated planning exercises. Many of these historical analyses skew heavily toward solar home systems over minigrids due to their lower connection costs, but they often overestimate standalone SHS’ ability to meet demand from small and medium-sized enterprises and make broad assumptions about system longevity, replacement and upgrades over time. Lighting Global estimated that 420 million people now use standalone off-grid solar, while the World Bank's Energy Sector Management Assistance Program (ESMAP) estimates that another 47 million people rely on minigrids, a nearly tenfold difference.

But the future potential in the minigrids sector is staggering; credible estimates suggest that minigrids will be the least-cost solution for 100 million Africans and up to 292 million people globally by 2030. By the same year, ESMAP estimates that globally, minigrids could carry a USD $3.3 billion annual profit potential for private sector developers.

While the long-term trend of corporate-level investment in off-grid solutions is aggressively positive, minigrids have been a categorically underfunded segment of energy access markets, raising only 20 percent of the total corporate-level capital for energy access sector since 2010, according to Wood Mackenzie data.

In Wood Mackenzie’s Energy Transition Practice, we’ve been taking a much closer look at minigrid markets as of late, and we recently zoomed in on Kenya as an compelling case study to apply a contextualized market evaluation methodology and draw some lessons for the global minigrids sector.

Kenya is neither the largest nor the most robust private-sector minigrid market globally, but a few rarely concurrent attributes about Kenya’s market make it an attractive case: its impressive progress toward universal electricity access on and off the grid, prioritization of comprehensive national electrification strategies, and a mature and well-studied SHS market.

Kenya's rapidly rising electrification rate

Kenya’s electrification rate has risen aggressively from 42 percent in 2015 to 75 percent in 2018 on the back of myriad national electrification programs, as well as it being one of the epicenters of the global solar home system market for many years. The 2018 Kenya National Electrification Strategy set a goal for universal access by 2022, aiming to address 60 percent of the remaining 12.8 million Kenyan residents without electricity with grid extension and intensification and 40 percent with off-grid solutions such as minigrids and SHS.

These goals are bolstered by three World Bank-financed programs: the Last Mile Connectivity Program (LMCP), the Kenya Electricity Modernization Program (KEMP), and the Kenya Off-Grid Solar Access Project (K-OSAP), which have collectively attracted $1.3 billion in committed financing to provide electricity access to 1.1 million Kenyans by 2023.

But not all is rosy. Despite Kenya Power’s (KPLC) impressive advances in expanding the rate base by connecting over 3.25 million new customers since 2015, largely through the LMCP, most of these new customers have been low-income peri-urban and rural households. These customers consume on average only 8 to13 kilowatt-hours per month and cost significantly more to connect and meter compared to urban customers who consume on average 40 to 50 kWh per month.

Additionally, many of the LMCP contractors connected hundreds of thousands of customers without metering them in 2016-2017 before the election, resulting in even less cost recovery from the expensive investments in the distribution network to connect low-demand customers. Consequently, KPLC’s net earnings declined by 92 percent year-over-year in 2019, driven by continually stagnating electricity demand, increases in power purchase and finance costs, and rampant power theft from unmetered customers and cartels that have cost the company a running tab topping KES 20 billion (~$185.5 million).

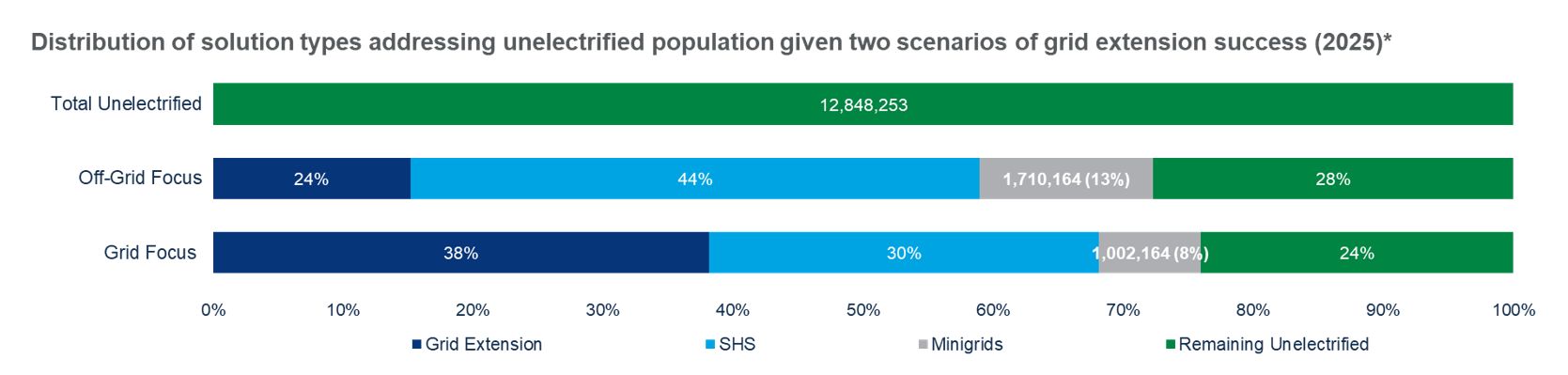

As a result, the future growth of the private minigrid market in Kenya is most sensitive to the success of the national grid extension programs, particularly the LMCP. We’ve therefore modeled both a grid-centric and off-grid centric scenario. We estimate that minigrids will serve between 1 million and 1.7 million Kenyans by 2025, representing between 8 and 13 percent of the remaining residents who do not have electricity. Private-sector players are positioned to serve 55 percent of new connections.

Across all technology sets for electrification, we forecast that Kenya will reach 94 percent electrification by 2025, falling short of the 2022 target but continuing its progress toward universal access.

Source: Wood Mackenzie

Kenya is a strong example of the increasingly convergent worlds of grid-connected and off-grid power markets. As integrated electrification planning becomes a more standard tool for utilities and regulators, the role of minigrids as a key ingredient will become increasingly apparent.

***

Download the free executive summary of Wood Mackenzie's new report, The Missing Piece to the Integrated Electrification Puzzle: A Bottom-Up Study of Kenya’s Energy Access Minigrid Market.

41

41

15

15

9

9