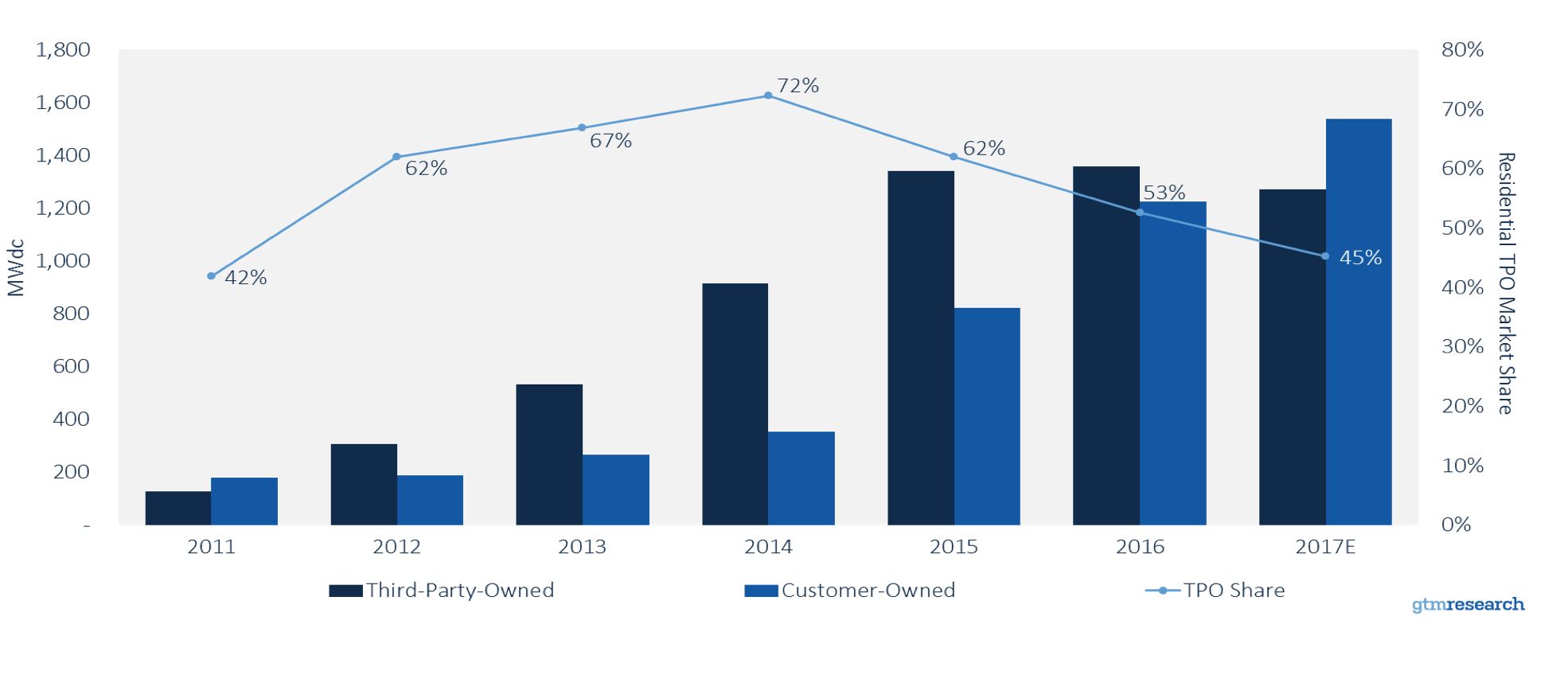

We’ve long been following the shift away from residential solar leases, which peaked in 2014 at 72 percent of the market. In recent months, the market has been increasingly leaning toward customer ownership. And now officially ownership dominates.

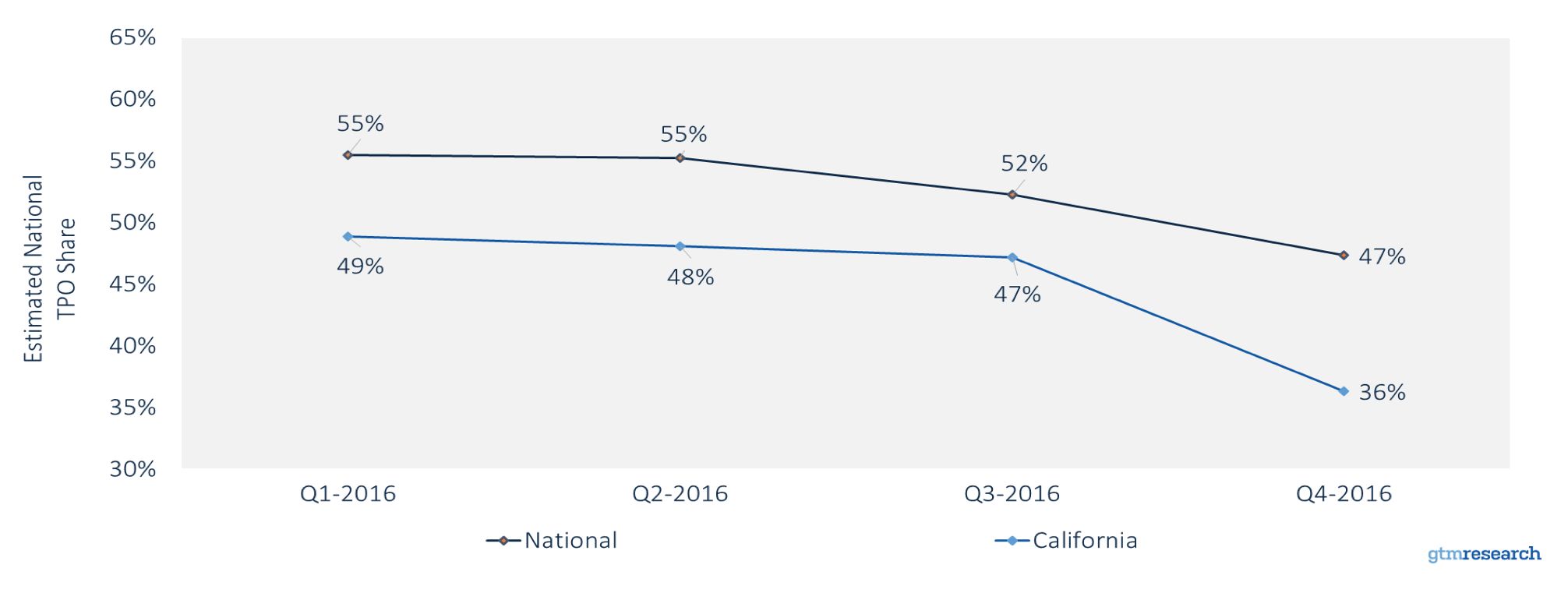

The market flipped in the last quarter of 2016, when just 47 percent of all new residential solar installed was third-party owned.

Source: GTM Research U.S. Distributed Solar Service

Source: GTM Research U.S. Distributed Solar Service

There are two major reasons why Q4 tipped the scale. The first is SolarCity.

As Tesla recently announced, 28 percent of SolarCity’s Q4 solar deployments were purchased by customers. Presumably that percentage is even higher for residential installations. Despite SolarCity’s declining market share, the company still accounts for about one-quarter of all residential solar installed. Any major changes to its strategy will have an impact on the market -- and we’re already seeing that impact.

Tesla said it will continue transitioning to direct sales in order to generate more cash upfront. Vivint Solar is also making this shift, albeit more slowly and still primarily in markets without legal third-party ownership.

The second (and somewhat overlapping) reason is California. The state fell to 36 percent third-party ownership in Q4, down from almost half the market at the beginning of the year and as high as 75 percent in mid-2013. Small local installers, as in most other states, have long preferred cash sales. The biggest change happening in California, however, is that larger installers like SolarCity, Sunrun and Sungevity are moving to cash more quickly there than anywhere else.

California is a shrinking market. But it's still an extremely influential segment on the national market. It could be a sign of what’s to come in other major solar states, especially as national installers introduce loans in new markets.

Overall, the national TPO share declined to 53 percent in 2016. Third-party-owned capacity was roughly flat from 2015, while customer-owned solar grew almost 50 percent.

This year will be the first full year since 2011 in which less than half of new residential solar installed is third-party owned. There are several factors that could slow this trend, such as the relative rise of TPO-dominated Sunrun or, likewise, growing TPO-dominated states such as New Jersey and Maryland.

This year will be the first full year since 2011 in which less than half of new residential solar installed is third-party owned. There are several factors that could slow this trend, such as the relative rise of TPO-dominated Sunrun or, likewise, growing TPO-dominated states such as New Jersey and Maryland.

But despite these, all signs point to the continued rise of customer ownership. Leasing was a necessary temporary solution that sparked the original growth of residential solar, but the future is cash and loans.

42

42

15

15

9

9