Led by a record-breaking fourth quarter, energy storage deployments in the United States totaled 336 megawatt-hours in 2016, doubling the megawatt-hours deployed in 2015. According to GTM Research and the Energy Storage Association’s U.S Energy Storage Monitor 2016 Year in Review report, 230 megawatt-hours came on-line in the fourth quarter of the year, more than the sum of the previous 12 quarters combined.

FIGURE: U.S. Energy Storage Deployments (MWh)

Source: GTM Research / ESA U.S. Energy Storage Monitor

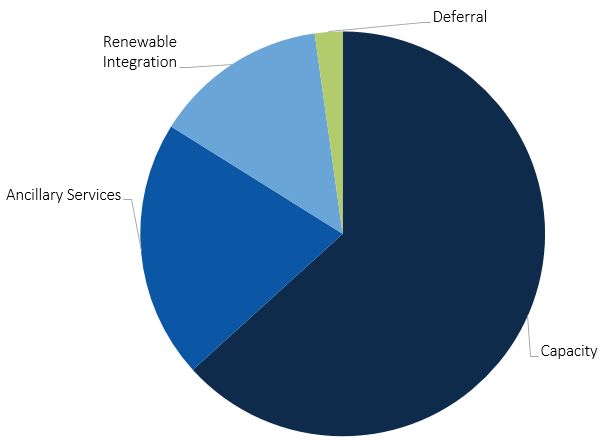

“The fourth quarter marked a turning point in the U.S. utility-scale energy storage market, reflected by the burst of deployments over an extremely short period from inception to interconnection,” said Ravi Manghani, GTM Research’s director of energy storage. “California will play a significant role in the future as utilities there continue to contract energy storage under the state’s 1.3-gigawatt mandate. While California took over the pole position in 2016 from PJM, the market shift was also transformational in terms of applications -- from short-duration ancillary services to longer-duration capacity needs.”

As a result, even though the market stayed roughly flat in megawatts, it grew 100 percent in megawatt-hours.

“The energy storage industry is rapidly maturing, and in 2016 we saw that growth take hold in a significant way,” said Matt Roberts, executive director of the Energy Storage Association. “The energy storage industry’s rapid response to address the Aliso Canyon disaster, as well as the continued growth in applications and business models for storage systems, signals to all stakeholders the immense value that energy storage systems are delivering today.”

According to the report, California made up 88 percent of all installed energy storage capacity in the fourth quarter, driven by the large 4-hour systems that were procured in response to the Aliso Canyon leak. The report notes that long-duration systems continue to be deployed in early 2017, a trend that is likely to persist over the coming quarters.

FIGURE: Front-of-Meter Deployments by Primary Application, 2016

Source: GTM Research / ESA U.S. Energy Storage Monitor

While utility-scale storage made up the bulk of deployed megawatt-hours, commercial and residential systems (behind-the-meter) represented a sizable 25 percent of capacity on the year. The majority of that came from commercial storage in California; however, the residential segment saw increased geographic diversification, with two-thirds of deployments outside California and Hawaii. GTM Research anticipates that the residential segment, starting from a small base, will be the fastest-growing segment over the next five years.

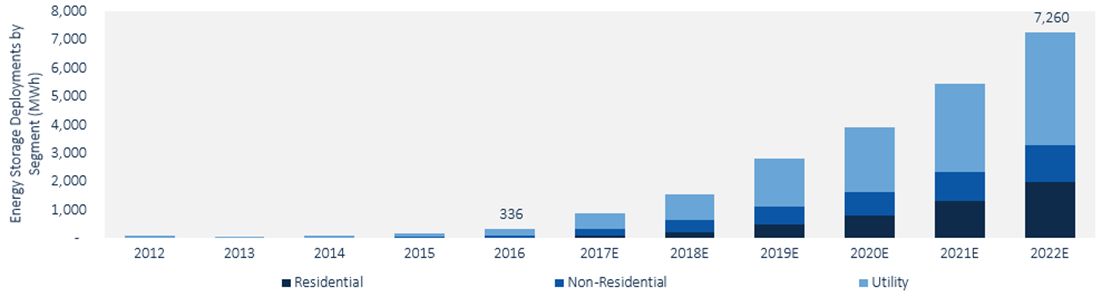

FIGURE: U.S. Annual Energy Storage Deployments, 2012-2022E (MWh)

Source: GTM Research / ESA U.S. Energy Storage Monitor

According to GTM Research, the United States’ energy storage market will grow from 336 megawatt-hours in 2016 to 7.3 gigawatt-hours in 2022 when it will be a $3.3 billion market.

Key Findings From the Report

- The U.S. deployed 336 megawatt-hours of storage in the entirety of 2016, growing 100 percent over 2015

- The U.S. deployed 230 megawatt-hours in Q4 2016

- U.S. energy storage market to reach 7.3 gigawatts in 2022, valued at $3.3 billion

- Behind-the-meter storage represented 25 percent of all deployments in 2016

- Measured in power, 221 megawatts of energy storage were deployed in the U.S. in 2016, which is essentially flat year-over-year

- Lithium-ion represented at least 97 percent of all energy storage capacity deployed in 2016

***

Purchase the report here.

42

42

15

15

9

9