Last week I attended EnerNOC's analyst day, a gathering of financial and industry analysts, for an update by its senior management team on EnerNOC's strategy.

To summarize, EnerNOC has positioned its offerings, team and capabilities to expand beyond demand response (DR) programs into software. This meeting provided an update of this plan, especially for the financial community. With a profitable core business, more than $100 million in cash on hand and an infusion of enterprise software talent, EnerNOC has a real chance to become a leader in the emerging enterprise energy management software space.

Below are my notes and thoughts from the event. All the presentations can be found online here.

Key Notes From the Presentations

-

Market opportunity: EnerNOC sees a $1.5 billion U.S. market for DR, and a global DR market three times larger than that. It estimates the market for energy management software, which it calls Energy Intelligence Software (EIS), to be $5 billion.

-

EnerNOC believes it is poised and ready to be a leader in the EIS segment, just as it became a leader in the DR space against numerous competitors.

-

EnerNOC has added software experience throughout the company, including at the board level, management team (new CFO and new VP of Enterprise Sales), product management, product marketing, and engineering.

-

In DR, the biggest market opportunity for growth is in Texas (ERCOT) and international markets. Its DR strategy is to diversify away from PJM, expand sales to traditional utilities, and grow internationally.

-

For the EIS market, the strategy is to focus on the top 100,000 commercial and industrial customers (C&I) in the U.S. and to sell them the company's chief products: SupplySMART (procurement and utility bill management), EfficiencySMART (energy use monitoring), and DemandSMART (demand response and time of use monitoring).

-

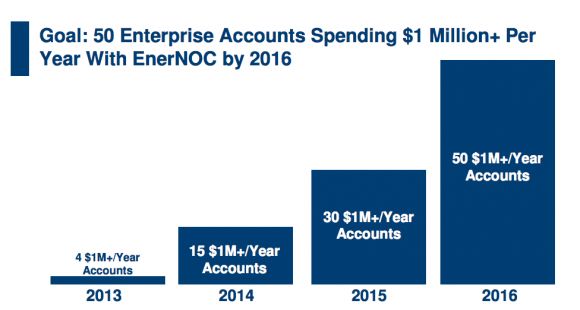

Sales strategy is to close 50 large C&I customers, which have an average $200 million yearly energy spend, on software deals of $1 million annually in three years. EnerNOC already has four customers at this level and proposals in place with another ten.

-

According to company executives, top competitors for software sales are Schneider Electric, Siemens, Constellation, Ecova, Comverge and IBM.

-

From a business-model standpoint, EnerNOC aims to diversify away from its hugely seasonal business (100 percent of EBITDA and 70 of percent revenue come in Q3) with increased software sales and non-Q3 DR revenue.

-

Growth strategy has three elements: 1) Grow U.S. DR business, 2) Drive DR internationally, and 3) Drive adoption sales of its energy management software. This strategy will add $200 million in top-line growth with the following breakdown: $40 million in DR, mostly driven by Texas; $90 million for international DR; and $70 million in EIS software, driven by $1 million yearly contracts with large C&I customers.

-

Gross margins are expected to dip from 50 percent to 45 percent next year, and then grow toward 50 percent afterward.

Groom Energy Analysis

Regarding the software business, with the addition of many people with software experience, the company looks very different than it did three years ago. We were pleased to hear that the company is investing more in a utility bill management (monthly bill) solution for customers rather than just real-time interval data, as this development matches the broader customer need we see in the marketplace.

The existing relationship it has with thousands of customers through its DR offering (DR clearly has been a "killer app") and its strong balance sheet position it well to execute on its product roadmap.

EnerNOC's offerings and roadmap include a number of capabilities that will be attractive in the market, including enhanced understanding of tariffs for customers, using DR fees to fund energy management software (most vendors can't do this), one-stop shopping, peak-rate analysis with action at the facility level (e.g., time of changes), and energy analysts to analyze energy data for time-starved facility and energy engineers.

A higher mix of recurring and high-margin software revenue will help increase company valuation (the company is currently valued at 1X revenue -- enterprise value / revenue).

The transition will not be easy, however. EnerNOC made a large, successful DR business by basically giving money to companies to shut things off or to run local generators. Asking companies to pay for software, in a highly competitive software field, is a larger challenge.

We have seen few $1 million yearly software deals for energy management software, so we believe EnerNOC's average deal size estimates are too high, but the company may make up for this on a larger volume of smaller deals. The company's roadmap does not include any products for asset management, so companies that wish to have a single solution for asset management and energy management will need to consider to other vendors.

Overall, however, EnerNOC is well positioned to be a market leader. Only a handful of other companies have the product breadth and financial resources to challenge them.

***

Paul Baier leads Groom Energy's Sustainability Consulting practice, which assists Groom Energy's customers with their sustainability and energy reduction strategies, carbon footprint, and responses to supply chain surveys such as Walmart Supplier Assessment and Carbon Disclosure Project.

41

41

15

15

9

9