The past decade has been a wild ride for America's massive electricity sector. Cheap wind and solar have turned the industry's conventional economic wisdom on its head.

At the same time, climate change has begun directly impacting utilities — from hurricanes that have forced billions of dollars in recovery and grid-hardening costs for utilities like NextEra’s Florida Power & Light and Texas’ Oncor, to the wildfires that drove Pacific Gas & Electric into bankruptcy.

Utilities will be front and center in America's efforts to combat global warming, from drastically cutting their own carbon emissions to assisting other sectors, such as transportation, in cutting theirs. Today, no U.S. utility can be said to be close to that vision — or not outside a few fortuitously supplied and forward-thinking outliers like Vermont’s Green Mountain Power.

Still, some are undoubtedly moving ahead of others, driven by state mandates, the inexorable math of ever-cheaper renewables and other factors. Last year saw major carbon-free targets set by utilities including Duke Energy and Xcel Energy; this week, Arizona's APS made its own carbon-free pledge in a state without major climate legislation on the books.

Out of scores of potential examples, GTM has chosen to highlight four companies: NextEra Energy, Berkshire Hathaway Energy, Dominion Energy and Pacific Gas & Electric. These electricity giants provide a view into how America's major utilities are taking up the opportunities of the energy transition in 2020 — or failing to meet its biggest challenges.

NextEra Energy: America's renewables behemoth

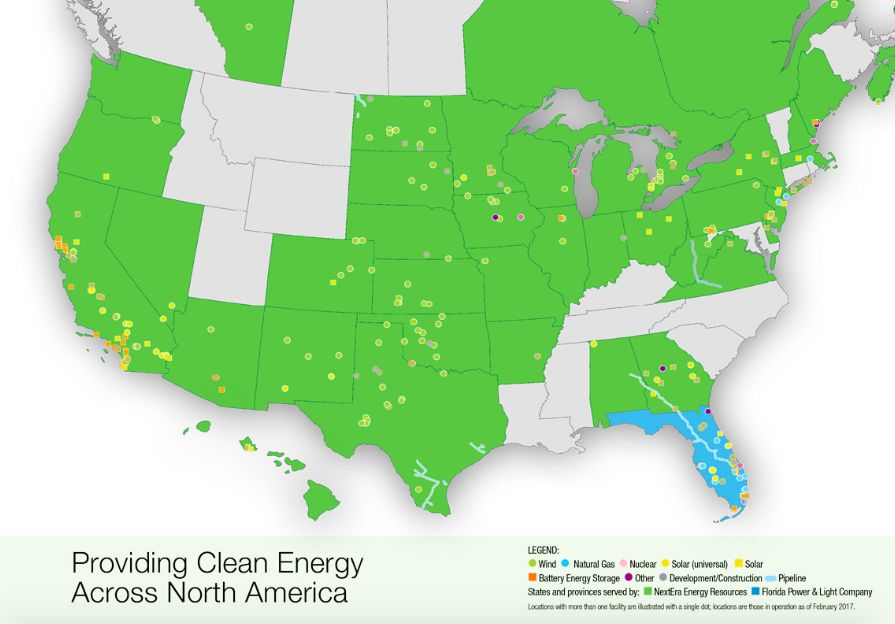

Renewables have long been the key driver of growth for Florida-based NextEra Energy, which developed its first wind farm more than two decades ago. What looked like a risky bet at the time has, in hindsight, been one of the smartest the utility sector saw in that time.

NextEra got into the U.S. wind business early in its development and quietly built a 15-gigawatt base of installed wind capacity, nearly twice the size of second-place Berkshire Hathaway Energy’s fleet.

More recently, NextEra has pressed heavily into utility-scale solar, its nearly 4.4 gigawatts of capacity now standing as the single largest solar fleet outside of China, according to Wood Mackenzie data. More than half of the company's solar projects in 2019 were paired with energy storage to create what the company calls a "near-firm" generation resource.

Thanks in large part to its mastery in the renewables market, NextEra has captured the title of largest U.S. electric utility by market capitalization, valued at a whopping $125 billion on Jan. 21. That's far above similar multistate utilities with a mix of regulated and unregulated businesses, such as Southern Company ($71 billion) or Duke Energy ($69 billion), or other similar multistate investor-owned utilities like Dominion Energy ($69 billion), American Electric Power ($49 billion) and Exelon ($46 billion).

NextEra owns and operates one of the world's largest fleets of wind and solar projects. (Credit: NextEra)

Compared to some of its peers, NextEra’s market position is privileged by its large mix of unregulated business, not all of it renewables.

NextEra’s slate of state-regulated investor-owned utilities, by contrast, is relatively light — not that it hasn’t been trying to expand it. Over the past five years, NextEra has failed in its $4.3 billion bid for Hawaiian Electric and its $18.7 billion bid for Oncor.

That leaves it with its flagship utility Florida Power & Light, with more than 5 million customer accounts, and the smaller utility Gulf Power, with about 460,000 customer accounts, which it acquired for $6.4 billion last year. Both are relatively advanced in terms of grid modernization.

FPL has already deployed smart meters, outage detection and restoration, and other key distribution grid technologies helpful in recovering from the state’s frequent hurricanes. Gulf Power is using its smart meter fleet for locational demand response.

FPL is now putting NextEra’s deep renewables expertise to use in its in-state utility-scale solar plans, with more than 8 gigawatts planned by 2030. This has helped push Florida ahead of California for utility-scale solar development projections through 2025, but it has made it difficult for third-party solar developers to enter the market.

FPL is also planning more than 400 megawatts/900 megawatt-hours of battery energy storage at its Manatee Energy Storage Center, one of the largest projects in the country.

As with most investor-owned utilities, NextEra has been much less supportive of policies that permit its customers to be paid for the solar they put on their roofs. FPL joined other Florida utilities in a multiyear fight against the expansion of net metering in the state, including backing a ballot initiative, defeated in 2016, that would have locked in utilities' monopoly over electric sales. Third-party solar installers only won the right to serve Florida customers in 2018, and rooftop PV penetration remains low.

Such slow growth in one of the country's sunniest states could be seen as a lost opportunity to reduce carbon emissions. At the same time, NextEra's investment, backed by the certainty of rate recovery, has boosted the state's solar generation far beyond what would be possible with distributed PV, and at lower cost.

This tradeoff is one increasingly being adopted across the Southeast, with Duke Energy’s push into utility-scale solar in its home states of North Carolina and South Carolina following a similar path.

Berkshire Hathaway: No two regions the same

Few utility groups are sailing in as many different political and geographic crosscurrents as Berkshire Hathaway Energy, the energy holding company of Warren Buffett’s $500 billion conglomerate.

BHE owns four regulated utilities serving customers in 11 states across the Western U.S., as well as an unregulated renewables business that operates across the country.

BHE’s giant wind fleet is shared between its unregulated and regulated utility businesses, with Iowa-based MidAmerican Energy Company taking an early lead in capturing the region's plentiful wind resources. With just short of 800,000 customers, MidAmerican had more than 6,500 megawatts of wind power at the end of 2018, accounting for about 60 percent of its generation capacity.

MidAmerican met just over half its customers' energy demand in 2018 from renewables and expects wind to be able to meet 100 percent of its demand on an annual basis when its 591-megawatt Wind XII project is complete this year.

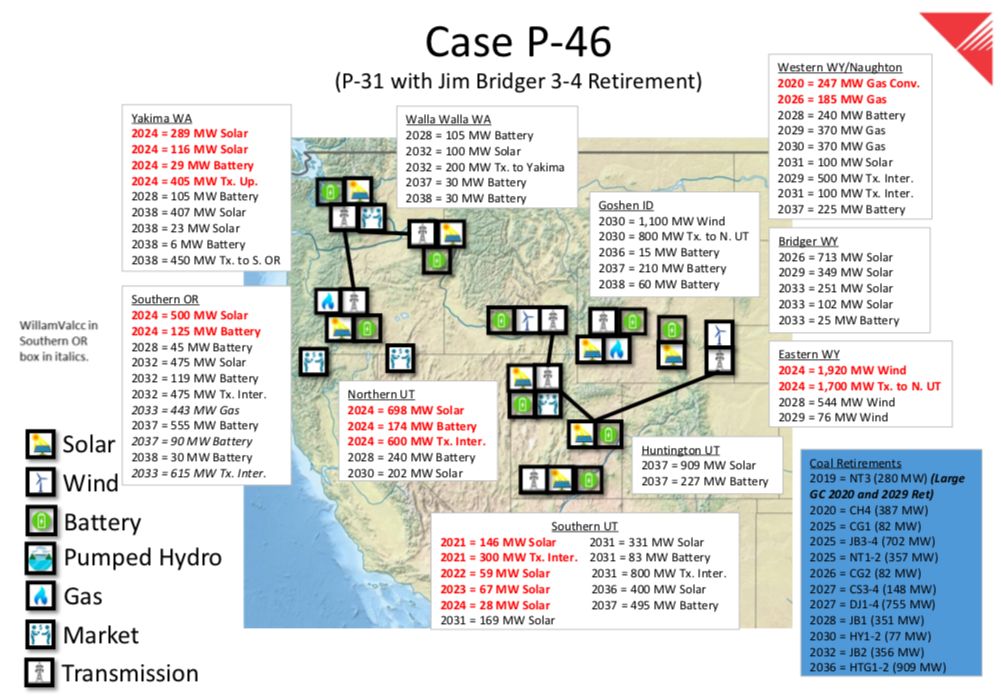

Then there's PacifiCorp, which serves about 1.9 million customers across six states from Oregon to Wyoming and whose utilities plan to build or repower more than 2 gigawatts of wind capacity by the end of this year.

Over the medium term, PacifiCorp's integrated resource plan calls for adding 3,000 megawatts of solar paired with about 600 megawatts of battery storage by 2025, along with another 3,500 megawatts of new wind, as the below chart indicates. It also calls for the early retirement of five Wyoming coal plants, setting up a conflict with the state’s coal-friendly political leadership.

PacifiCorp is going big on renewables, including in coal-friendly Wyoming. (Credit: PacifiCorp)

Finally, there's NV Energy, Buffett's Las Vegas-based utility serving about 1.3 million customers. NV Energy is developing Nevada's first wind project while taking a much deeper dive into capturing the state’s vast solar energy potential.

NV Energy's integrated resource plan calls for adding nearly 1.2 gigawatts of solar by 2023, along with about 590 megawatts of battery storage, including one project that’s set to exceed NextEra’s Manatee Storage Center in terms of megawatt-hour capacity.

Still, NV Energy has a checkered track record when it comes to renewables. Most investor-owned utilities have fought state efforts to expand net metering for solar-equipped customers, and Berkshire Hathaway’s utilities are no exception.

NV Energy pushed state regulators to pass a 2015 decision that would have slashed compensation for existing as well as new net-metered customers, a move that prompted a backlash from solar advocates and led state lawmakers to reinstate the program in 2017.

NV Energy also faced a revolt from its largest commercial client, MGM Resorts International. The casino giant defected in 2016 to contract with independent energy provider Tenaska, allowing it to reduce rates while doubling its share of renewables compared to NV Energy’s state-mandated share.

This push from politically powerful commercial customers to set their own energy futures, combined with a Democrat-controlled state legislature, has driven major changes in Nevada energy.

NV Energy has adapted with its recent push into renewables; other utilities that have yet to shift from the status quo now face a reckoning, as our next example illustrates.

Dominion Energy: Risks of the status quo

Dominion Energy has made waves with its renewables plans over the past year, notably the 2.6-gigawatt offshore wind farm it plans to build for its home state of Virginia, by far the largest such project underway in the country.

But Dominion, which has operations in 18 states and a major stake in natural-gas infrastructure, has also been holding back Virginia's renewable energy potential, according to critics.

However, with Democrats taking control of the state legislature in November, Dominion's hold on state energy policy has been challenged.

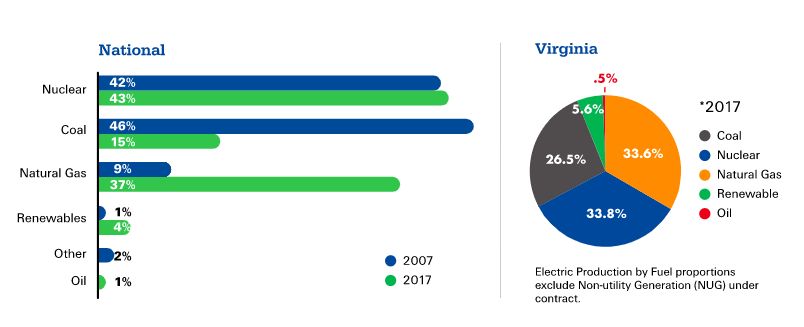

Dominion’s generation portfolio for Virginia is roughly one-third natural gas, one-third nuclear and one-quarter coal, with just over 5 percent ascribed to renewable energy, much of it hydropower and biomass. It’s heavily invested in its existing natural-gas operations, and its plans for the Atlantic Coast pipeline project have drawn opposition from environmental groups and local residents.

Dominion's generation fleet centers around nuclear and gas. (Credit: Dominion Energy)

In Virginia, Dominion has used its lobbying clout for decades to secure favorable policies from state lawmakers, sometimes at the expense of its ratepayers. Most recently, in 2015 it secured passage of a law that ostensibly froze rates at their current level, but actually held them higher than they would otherwise have been if the State Corporation Commission had been allowed to review them and order refunds.

Virginia’s Grid Transformation and Security Act, passed in 2018, ended the rate freeze and mandated that Dominion spend $870 million on energy efficiency. But it also declared large swaths of renewable energy, energy storage and transmission and distribution grid investment to be “in the public interest.”

This move weakened regulators' authority over Dominion’s investment decisions, but opened up the opportunity for the utility to push ahead on self-owned renewable projects in the state, such as last fall's contract for clean energy for state agencies and now its offshore wind project.

Dominion has been accused of undercutting the 100 percent clean energy offerings from competitive electricity providers in the state, while proposing its own clean energy package that includes coal-burning biomass plants as well as solar and hydroelectric facilities. Big-box retailers like Target, Walmart and Costco have sought to depart Dominion's service, while key data center clients like Apple, AWS and Microsoft have criticized Dominion for its plans to expand natural gas.

The recent flip of Virginia’s legislature from Republican to Democratic control leaves Dominion facing the possibility of a raft of new clean and distributed energy mandates coming in 2020.

That includes the likelihood of legislation codifying Governor Ralph Northam’s executive order setting a 30 percent renewable portfolio standard for 2030 and a goal of 100 percent carbon-free energy by 2050. The state may also see the passage of a “Solar Freedom” bill to reform interconnection standards, lift the state’s 1 percent cap on net-metered solar, and confirm the legality of third-party solar power-purchase agreements.

Virginia lawmakers are considering other policy changes that could alter Dominion's role, such as opening its energy markets to broader retail competition, or even relegating the utility to the role of distribution grid operator.

While similar efforts have failed before, the shift in political and popular opinion against the state's dominant utility indicates significant changes ahead in 2020.

PG&E: Today's climate crisis

State policies have driven many important and beneficial changes at utilities. But state policies do not ensure a successful utility energy transition.

For evidence, look no further than California, the U.S. leader in distributed and utility-scale solar, as well as in batteries and electric vehicles that can absorb, balance and make use of intermittent and distributed solar supply.

The state's largest utility, Pacific Gas & Electric, has been a trailblazer in all of those areas. PG&E is also bankrupt and facing a highly uncertain future.

PG&E’s wild tumble into the abyss underscores how well-meaning state ambitions can be overridden by a combination of complex factors — from climate change and land-use patterns, to a specific utility’s poor decisions and safety failures, to regulatory shortcomings.

Indeed, PG&E’s financial collapse has driven a number of of state politicians to call for its public takeover — an unprecedented step in the modern American utility sector.

PG&E is already on track to meet the state’s 2030 targets of 60 percent renewables and has pledged to honor its legacy renewable energy contracts through bankruptcy. It promises to expand investment into fire-resilient infrastructure, including plans to turn substations in fire-prone regions into battery-backed community microgrids.

But it’s still not clear how PG&E will pay off its creditors and emerge from bankruptcy by mid-2020, let alone structure its business to finance billions of dollars of grid-hardening and fire-prevention efforts along with its broader state-mandated goals.

In the longer term, PG&E and its fellow California utilities may face an existential challenge to their role as the state’s default generation resource procurers via the rise of community-choice aggregators.

CCAs already manage electricity procurement for more than half of PG&E’s customers, with cheaper and cleaner energy compared to PG&E’s legacy resource mix. Since its bankruptcy, some CCAs have sought to take over portions of PG&E’s grid, while others have called for relegating it to the status of a “wires-only” utility.

PG&E’s unusual circumstances make comparing it to other utilities difficult. California is unique in holding utilities financially liable for fires caused by their equipment even if they followed all safety regulations.

Still, utilities across the country and around the world will need to come to grips with climate change and local demands for control over their energy supply. PG&E is the canary in the coal mine — and among the most important utilities to watch in 2020.

41

41

15

15

9

9