Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!

---Lewis Carroll, Through the Looking Glass

2012 was both the hottest year on record for the contiguous U.S. and the most expensive year for gasoline in U.S. history. What gives?

Superstorm Sandy, which devastated the New Jersey and New York areas in October, raised awareness about climate change substantially because of a growing awareness that the numerous major storms and hurricanes hitting the East and the South are far beyond normal averages. But concerns about fossil fuel depletion (“peak oil”) seem to be on the downswing as we hear more and more news about booming production of oil and gas in the U.S. This essay will look at what I call the “twin crises” of climate change and peak oil and attempt to make sense of the hubbub of news surrounding these issues.

Whether human-generated emissions of greenhouse gases are behind recent extreme weather events or broader climate trends is debatable now only in terms of the degree to which human causes are trumping any natural variation. There is obviously much natural variation in the record -- and this variation has taken place historically before any human influence. The differences today are the speed at which such changes are occurring.

Popular concern about climate change diminished dramatically in the last few years, however, for a variety of reasons, and President Obama decided not to push comprehensive solutions to climate change through Congress in his first term -- and, to be fair, he couldn’t have even if he wanted to after Republicans took back control of the House in 2010. To his credit, Obama did complete a major update to fuel economy (CAFE) requirements for cars and light trucks, which are now required to achieve 54 mpg by 2025 (with some major loopholes that bring the actual number down to about 36 to 42 mpg, still a major improvement). He is also pushing for major new emissions limits on coal power, now the largest source of carbon dioxide in the U.S.

With the wakeup call of Superstorm Sandy and a new four-year term, Obama has indicated that he will make climate change and energy solutions a major priority, as I wrote recently.

Concerns about the second of the twin crises, peak oil, have similarly diminished. I haven’t seen polls on this issue, but it’s clear that the attitude among the public and pundits alike is far more complacent on this key problem than it was just a few years ago, as oil prices reached record highs in a precipitous run-up that peaked in mid-2008.

Many experts are now downright bullish on the prospects of American fossil fuels, due to new fracking technologies, with many commentators talking of a new economic era for the U.S. ushered in by plentiful new cheap fossil fuels. This attitude is strange for a number of reasons, not least of which is that 2012 was, as mentioned, the year of our most expensive gasoline ever and most expensive oil ever, when prices are adjusted to 2012 dollars -- in the midst of a so-called boom in natural gas and oil production. There are many experts who see major problems with oil on the horizon. A recent research article in Nature, a major scientific journal, stated: “The economic pain of a flattening [oil] supply will trump the environment as a reason to curb the use of fossil fuels.”

This two-part series will attempt to show why concerns about climate change and peak oil should be at the very top of our political agenda, from the local to the international level. This essay focuses on oil production forecasts and the next will focus on natural gas projection forecasts.

The World Energy Outlook

The International Energy Agency (IEA) made headlines in late 2012 with its latest World Energy Outlook (WEO 2012) and its conclusion that the US may in fact become the world’s largest producer of oil by 2020 and possibly even energy independent for all practical purposes by 2035. There had previously been a lot of talk about the boom in U.S. production, but this report from the Western nations’ official energy watchdog seemed about the most powerful support possible for the “U.S. energy production is booming” school of thought.

What got buried under the headlines, however, is the second paragraph of the report’s Executive Summary:

Taking all new developments and policies into account, the world is still failing to put the global energy system onto a more sustainable path. Global energy demand grows by more than one-third over the period to 2035 in the…central scenario, with China, India and the Middle East accounting for 60% of the increase. […] Emissions in the New Policies Scenario correspond to a long-term average global temperature increase of 3.6 °C.

Emissions in the business-as-usual scenario (i.e., policies we have in place today) correspond to a 6° C (11° Fahrenheit) rise by 2100 -- which would be “catastrophic” for much of the globe, according to IEA’s chief economist Fatih Birol.

So the mainstream media’s treatment of this major report from the IEA misses what is clearly the most important point: we are on track for a climate catastrophe under current policies. It is certainly a good thing from a purely economic perspective that U.S. energy production is up. But from the broader climate perspective, it’s the opposite of good. The paradox, of course, is that we need fossil fuels to run our economy today. The solution to the paradox, as the IEA itself points out, is to rapidly move away from fossil fuels to a more efficient economy that runs almost entirely on renewable energy.

The IEA is far from infallible, however, and its recent statements on U.S. oil and gas production are strangely out of step with its own pronouncements just a few years ago. The IEA now projects that natural gas and oil fracking will lead to a dramatic increase in both natural gas and oil production in the U.S. through 2020. I’m going to explore various objections to these forecasts in this essay, focusing on oil.

(The real good news is that the U.S. and the world are undergoing a less publicized revolution in energy: the transformation of our electricity infrastructure away from fossil fuels and nuclear to renewables like solar, wind and biomass. More on these positive solutions in Part II of this series.)

WEO 2012 forecasts the following for U.S. oil and gas production, with the key conclusion for present purposes being a projection of over 50 percent of U.S. oil production coming from unconventional sources by 2020 or so -- up from about 25 percent today.

Figure 1: WEO 2012 Forecast for Oil and Natural Gas Production

It is helpful to compare WEO 2012 with WEO 2008. WEO 2008 was important because it was the first time that the IEA had conducted a supply-side analysis of global oil production. Previously, IEA had literally assumed that oil production would match whatever demand the global economy required, with no constraints on production. WEO 2008 found that the decline rate for the largest 800 oil fields, which constitute the vast majority of global oil production, is about 6 percent annually, and will rise to almost 9 percent by 2030. This was big news because the industry’s widely held assumption until that time was about 3 percent.

A 6 percent decline rate leads to 83 percent depletion after 30 years. An 8.6 percent decline rate leads to a 50 percent decline within about eight years and 93 percent depletion after 30 years.

In terms of the U.S., our current six-million-barrel-per-day average annual production will, all else being equal, with a 6 percent decline rate, fall to three mbpd in just twelve years. At an 8.6 percent decline rate, it reduces to three mbpd in just a little more than eight years. This means that the U.S. will have to replace literally half of its current production in eight years just to stay even.

The bottom line: The higher depletion rate of 8.6 percent, or even higher, is very likely applicable to the U.S. because we are now getting so much of our oil from unconventional sources, and these sources have far higher decline rates than conventional sources. (I am currently in dialogue with the U.S. EIA to gain more insight into the data it used for projecting U.S. oil production and will write more on this when I obtain the data I’m seeking.)

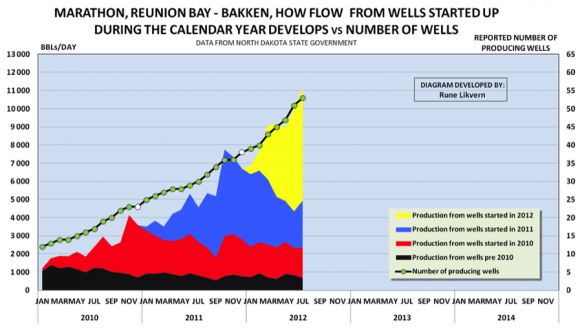

Rune Likvern, an independent oil analyst, wrote a widely read article on the Bakken formation in North Dakota, in 2012. The Bakken formation is one of the key new areas for oil production in the U.S. and it is currently producing about 0.7 mpbd (about 9 percent of the U.S. total). The IEA’s WEO 2012 relies on experience with the Bakken formation in making its very optimistic projections about unconventional oil production in the U.S. However, it’s not clear that this dog will hunt, so to speak, because the decline rates are so high for these new oil shale wells. Likvern shows that Bakken formation oil production from existing wells declined by more than one-third in just one year from mid-2011 to mid-2012. The total production continued to increase, however, because of new wells being added at a rapid rate (see Figure 2). The open question is: can this rate of depletion continue to be mitigated by adding new wells?

Likvern’s key conclusion is: “Shale plays do not get a pass on the laws of physics or the history of play and basin developments. […] It is challenging to find support for the idea that total production of shale oil from the Bakken formation will move much above present levels of 0.6 - 0.7 mbpd on an annual basis.” Production has already started to fall from the Bakken formation, as rigs are pulled out of the region, so it seems that Likvern’s analysis may turn out to be very accurate.

This is the Red Queen in action: we are running faster and faster just to stay in the same place. Or, to be fair, we’re running faster and faster to increase production in the short term, before a seemingly inexorable plateau and later decline sets in.

Figure 2: Likvern on Bakken Formation Oil Production

Another very skeptical take on the shale oil revolution comes from G. Allen Brooks, the Managing Director of PPHB LP, an energy investment company, highlighting exactly the same issue: the huge decline rates of shale oil and natural gas wells. Brooks cites the 44 percent annual decline rate for Bakken natural gas wells, which is even higher than Likvern shows for Bakken oil wells, and suggests that this may ultimately be applicable to oil wells too. Brooks states:

Fatih Birol, the IEA's chief economist, said his agency's forecasts to 2017 were based on data about existing reserves and production. He warned that the geology and reservoir performance of the oil shales were "poorly known," and he said it was unclear whether new reserves would be found to sustain production levels, let alone grow them. This is a critical consideration that underlies all the bullish forecasts for a new petroleum age for North America.

Brooks concludes:

The IEA has conducted extensive research into oilfield decline rates in the past [referencing the 2008 oil field decline study], but we sense little of that research was brought to bear in this study. […] At this point, we plan to use the [WEO] study as just one possible scenario for how the industry might evolve in the future. We are less inclined to embrace it than many others.

It seems likely, based on the very high decline rates seen in new tight oil formations in the U.S., that U.S. oil production will struggle to meet the levels that IEA forecasts, leaving the U.S. with continued reliance on oil imports and an increasing price problem when it comes to oil and gasoline.

This result wouldn’t be terribly bad, all else being equal, because we can probably get by with a lot less oil than we currently use, simply through conservation and efficiency improvements. However, all else is not equal: global oil exports have been in decline since 2005, and the U.S. is and will remain a major importer of oil. Even though oil imports have declined substantially in the last few years, primarily due to declining consumption, we still import about eleven million barrels per day -- equivalent to the entire output of Saudi Arabia and Iran combined. And it seems almost certain that global oil exports will continue to decline. I discuss the issue of “peak oil exports” further below, after focusing first on global oil projections.

Global oil projections are likely also off-base

Looking at global oil production forecasts, it appears that IEA is also unduly optimistic with respect to its oil projections. A detailed review by a researcher at the University of Barcelona, analyst Antonio Turiel, casts serious doubt on the accuracy of WEO 2012’s global oil forecasts due to their failure to take into account the declining energy content of unconventional oil.

Turiel shows the IEA’s projections for global oil production: a fairly steady uptick in overall production despite an inexorable decline in conventional oil production. Then he shows what this curve should look like after accounting for lower energy content in unconventional oil and the increased energy required to extract unconventional oil. This leads to a profound difference, taking global oil production down from almost 100 mbpd by 2035 to under 70 mbpd. And this assumes that the IEA’s underlying projections about unconventional oil production are correct -- which is far from established.

This 30 mbpd difference will, if accurate, have a profound impact and will lead to far higher prices for oil, as well as shortages in very parts of the world, all else being equal.

The triple whammy: High declines for unconventional fields, lower energy content for unconventional oil, and declining global oil exports

But there’s more bad news on oil availability. The issue of declining global oil exports, or “peak oil exports,” is probably the most important of the trends that I’ll discus in this essay. Citigroup recently projected that Saudi Arabia’s oil exports will, under current trends, decline to zero by 2032 because of increasing consumption by the Saudis themselves. The Saudis recently became their own biggest customer.

Citigroup’s projection came on the heels of a similar report from Chatham House, the British think tank, finding that Saudi oil exports will fall to zero by 2038, for exactly the same reasons as Citigroup cites. This decline in oil exports will occur due to the dramatic growth in consumption by Saudi Arabia’s rapidly growing population and increases in per capita energy consumption. Saudi domestic consumption of oil is growing at about 7 percent per year, which leads to a doubling of consumption every ten years.

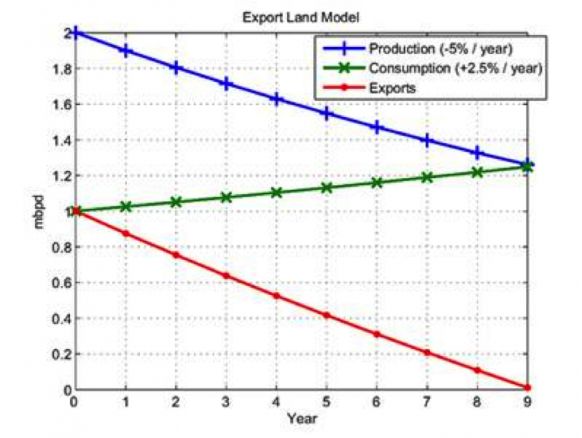

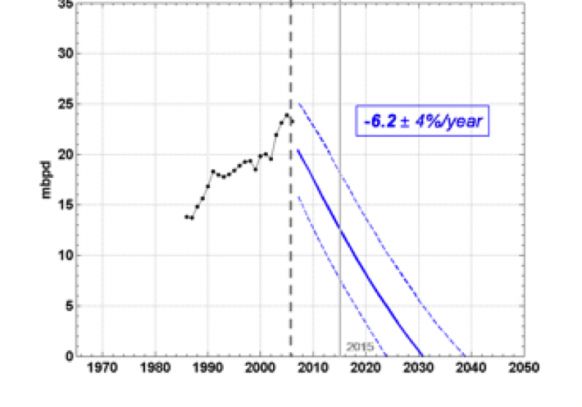

Saudi Arabia’s problem is not, of course, unique to Saudi Arabia. It is a global problem that afflicts most oil-producing countries. Jeffrey Brown and Samuel Foucher have developed an “Export Land Model” to predict how the global net oil export situation will unfold in coming years. They found that the top five exporters of oil (Saudi Arabia, Russia, Iran, United Arab Emirates and Norway) decline from about 24 mbpd in 2008 to about 7.5 mbpd in 2020 and go to almost zero by 2030. Global net oil exports are currently about 40 mbpd, so these producers comprise more than half of the global export market.

These net oil export projection declines are due to the demographic explosion that the Chatham House report focuses but also to declines in oil production in these countries. Chatham House chose not to discuss the role of declining oil production, choosing instead to believe Saudi projections of steady oil production, but this is a real and extremely serious corollary to the demographic explosion in oil-producing nations. It’s also the reason why Brown and Foucher project Saudi Arabia and other oil exporters going to zero faster than the Chatham House report. Figure 3 illustrates (with generic numbers) how these two trends work together to cause net oil exports to decline very quickly. Figure 4 shows the result of Brown and Foucher’s modeling for the top five producers.

Figure 3: Brown and Foucher’s Export Land Model

Figure 4: Brown and Foucher’s 2008 Projections for the Top Five Global Exporters of Oil

At the same time that global net oil exports are likely to decline quickly, China and India’s oil consumption is growing equally rapidly. A recent forecast by Jeffrey Brown found that under current trends China and India will consume literally all global net oil exports by about 2028. Will this actually happen? Probably not, because powerful nations like the U.S. will likely use their economic and even military power to ensure their energy needs -- a recipe for heightened conflict in a world that is already facing numerous other sources of conflict.

The future of energy

What do these trends add up to? It’s very likely, in my view, that the U.S. will, in just a decade or two, have to find a way to manage with about half the oil we currently consume. We could achieve this through conservation and energy efficiency, or through a dramatic and wartime-like expansion of drilling, or a combination of all three. But it seems highly unlikely that increased production will be able to get us much beyond where we are today due to the very high decline rates for oil shale fields discussed above.

What, then, is the future of energy? It seems pretty clear to me that the future of energy, at least insofar as oil is concerned, will be a story of necessary and dramatic conservation and energy efficiency improvements -- led by far higher prices and the declining availability of oil. An International Monetary Fund (IMF) working paper from mid-2012 supports this view and projects “a near doubling of the real price of oil over the coming decade.” The paper takes peak oil seriously, based on the decline rates observed in oil fields around the world.

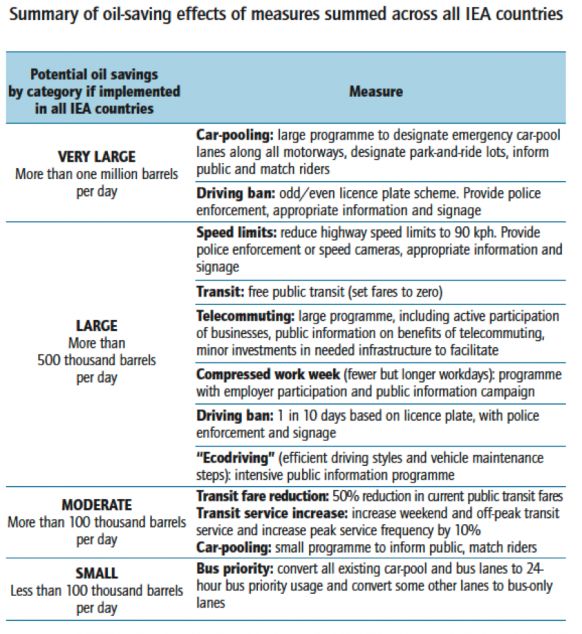

The IEA also released an excellent report in 2005 called “Saving Oil in a Hurry.” The report shows the following options for rapidly reducing oil consumption:

Figure 5: IEA’s Recommendations for Saving Oil in a Hurry

My feeling is that the U.S. and other advanced nations could get by with half of the oil they currently use largely through improved efficiency in transportation, but primarily through conservation measures. This means things like walking or biking instead of driving, using more freight trains instead of trucks, carpooling, or simply not driving as much when not necessary.

Now, there is a possibility that the oil shale revolution will spread to other countries in coming years and we’ll see a temporary boost in production like we’ve seen here in the U.S. But it’s unlikely that this increase will do more than provide a few extra years of time to transition away from oil. Those extra years will be very helpful, but we shouldn’t lose sight of the bigger picture of dramatically declining oil availability for massive oil importing countries like the U.S. Now is not the time to be complacent about our massive looming energy problems.

***

Tam Hunt is managing member of Community Renewable Solutions, a renewable consulting and project development company focused on community-scale wind and solar. He is also a lecturer at UC Santa Barbara’s Bren School of Environmental Science & Management.

42

42

15

15

9

9