With GTM Research estimating global PV supply to be in excess of demand by an average of 35 gigawatts per year over the next three years, 180 existing module manufacturers will either expire or acquiesce to acquisition by 2015. The largest number (88) of casualties will exit high-cost manufacturing markets in the U.S., Europe, and Canada.

Today GTM Research publishes Global PV Module Manufacturing 2013: Competitive Positioning, Consolidation and the China Factor, a report analyzing more than 300 module manufacturers, their global facilities, business models, financial health and chance of acquisition or expiry. The report also examines the market conditions and competitive metrics that will affect the trajectory of these firms over the next three years, including global demand, manufacturing costs, the influence of Chinese lenders, and the innovative upstream and downstream strategies that will buoy business lines.

FIGURE: CRYSTALLINE SILICON FACILITIES IN HIGH-COST LOCATIONS LIKELY TO FACE CONSOLIDATION IN 2013-2015

Source: Global PV Module Manufacturing 2013 (GTM Research)

“It’s the devil or the deep blue sea for the majority of these high-cost firms,” said Shyam Mehta, Senior Analyst at GTM and the report’s author. “Manufacturing costs for firms in Europe, the U.S. and Japan are currently over 80 cents per watt. The cost for their Chinese competitors is between 58 cents and 68 cents per watt. The writing is on the wall: these companies will either take what they can get via acquisition or they will bow out.”

While part of the report’s consolidation analysis focuses on companies operating in high-cost PV manufacturing markets, the question of Chinese module manufacturers, their strategies in the face of U.S. and potentially European import tariffs, as well as their domestic demand, debt and diversity are explored extensively in the report.

The report estimates that 54 of the 180 ill-fated firms will come from China. Most of these are so-called “solar zombies,” companies with manufacturing capacities less than 300 megawatts that have operated uncompetitively with support from the government. China’s number of ill-fated firms could be much higher if not for an aggressive downstream build-out that will prop up select domestic suppliers. China’s recent announcement to increase its cumulative 2015 solar target from 15 gigawatts to 21 gigawatts will most likely provide captive demand for firms such as Alex Solar, LDK Solar, and Astronergy.

In addition, as evidenced by the municipal loan to LDK Solar in July 2012 and the China Development Bank’s renewal of its pledge to support twelve selected domestic suppliers, GTM Research anticipates that the Chinese government will continue to provide financial support to established firms with large workforces in order to cover near-term debt obligations, or possibly to encourage diversified Chinese industrial conglomerates to acquire these companies. Potential beneficiaries of these strategies include Trina Solar, Yingli Green Energy, Suntech Power, JA Solar, Jinko Solar and Renesola; these companies make up more than 20 percent of existing global module capacity.

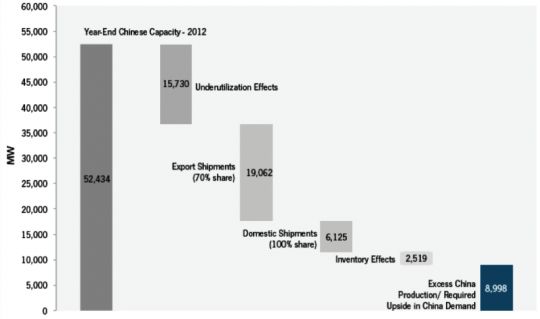

FIGURE: SUPPLY-DEMAND RECONCILIATION, CHINESE MANUFACTURERS, 2013E

Source: Global PV Module Manufacturing 2013 (GTM Research)

“To date, the consolidation in the PV manufacturing space that has occurred has done very little to relieve the industry of the ongoing problem of overcapacity,” said Mehta. “Profitability in the PV supply chain will continue to be extremely challenged until and unless there is significant capacity rationalization in China. For numerous reasons, we do expect this to start taking place in 2013. Combined with the exit of most firms in higher-cost locations and a stronger end-market, 2014 should see a more stable balance between supply and demand, which will position a select group of suppliers for sustained profitability. However, the road ahead will be strewn with casualties: between 2012 and 2014, we estimate that nearly 60 percent of existing PV suppliers will be forced to exit the market.”

RANKING: LEADING GLOBAL MODULE MANUFACTURERS BY 2015 (ordered alphabetically)

- Canadian Solar

- First Solar

- Hanwha Solar

- JA Solar

- Jinko Solar

- SunPower

- Talesun

- Trina Solar

- Yingli Green Energy

Source: Global PV Module Manufacturing 2013 (GTM Research)

For more information on Global PV Module Manufacturing 2013: Competitive Positioning, Consolidation and the China Factor, visit http://www.greentechmedia.com/research/report/global-pv-module-manufacturers-2013.

Report author Shyam Mehta talks about solar module winners, losers, who gets acquired, and what the market looks like in 2014 in this podcast.

42

42

15

15

9

9