The latest U.S. Residential Solar Update from GTM Research goes into stark detail about the changes afoot in this maturing and volatile market.

Not too long ago, a standalone SolarCity was growing 50 percent each year with a goal of 1 million solar rooftop customers by July 4, 2018. Residential solar players like Sungevity, NRG Home Solar and Spruce Finance were growing strong -- driven by the California Solar Initiative, the Investment Tax Credit and falling solar costs. Small vendors were being squeezed by the big guys. Power-purchase agreements (PPAs) dominated over solar loans.

Well, it's 2017. Trump is president. Pluto's not a planet. And the residential solar industry is moving up (and down) in unanticipated ways.

Sungevity went bankrupt. NRG pulled out of the market. Spruce had layoffs. SolarCity is now part of Tesla, on a throttled growth path and focused on solar roofs with infinity guarantees. And the long tail of solar installers is having its revenge.

States continue to actively fine-tune their residential solar programs. Hawaii's solar industry today shows what happens when a net energy metering program is abruptly removed. In April, Honolulu issued 188 permits for solar PV systems, a 61 percent decline from April 2016 and a 75 percent decline from April 2015, according to Marco Mangelsdorf, president of ProVision and founder of the Hawaii PV Coalition.

Sunrun is being investigated by the U.S. Securities and Exchange Commission regarding "whether the company adequately disclosed how many customers had canceled contracts," according to PV-Tech, which reports, "The SEC has already issued a subpoena to Sunrun and interviewed past and current employees. The commission is 'also looking into SolarCity,' according to a filing."

Mangelsdorf notes, "Last year, as reflected in their 10-K filings, the big three lost more than a cumulative $1.3 billion -- with SolarCity $820 million in the red from revenue of $730 million, Sunrun negative $303 million on revenue of $454 million and Vivint Solar minus $242 million on revenue of $135 million."

Amidst this chaos, GTM Research tracks and forecasts the trends and seismic shifts in this market.

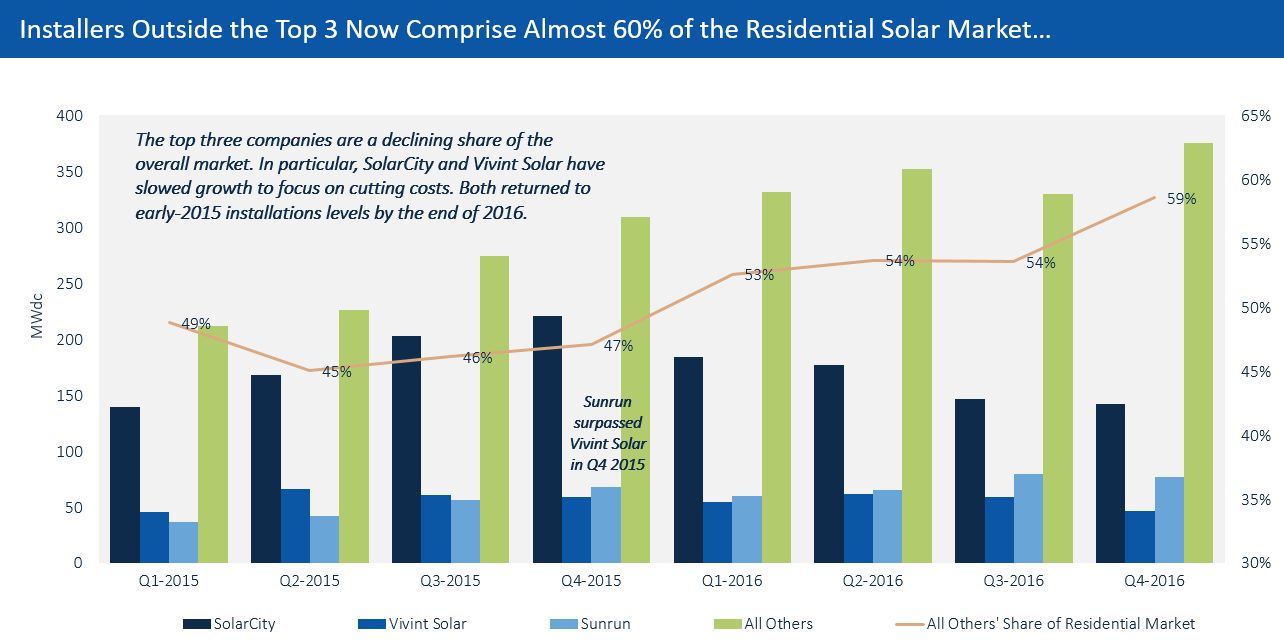

The revenge of the long tail

Although growth of the overall residential market slowed drastically in 2016, falling to 19 percent, installers outside of the top three grew at a much higher rate of 36 percent. In 2017, GTM Research expects SolarCity, Vivint Solar and Sunrun collectively to remain flat, while the rest of the market will grow close to 20 percent. (Andrew Beebe riffs on the long tail here; Barry Cinnamon provides a small installer's perspective here.)

Source: GTM Research U.S. Residential Solar Update 2017

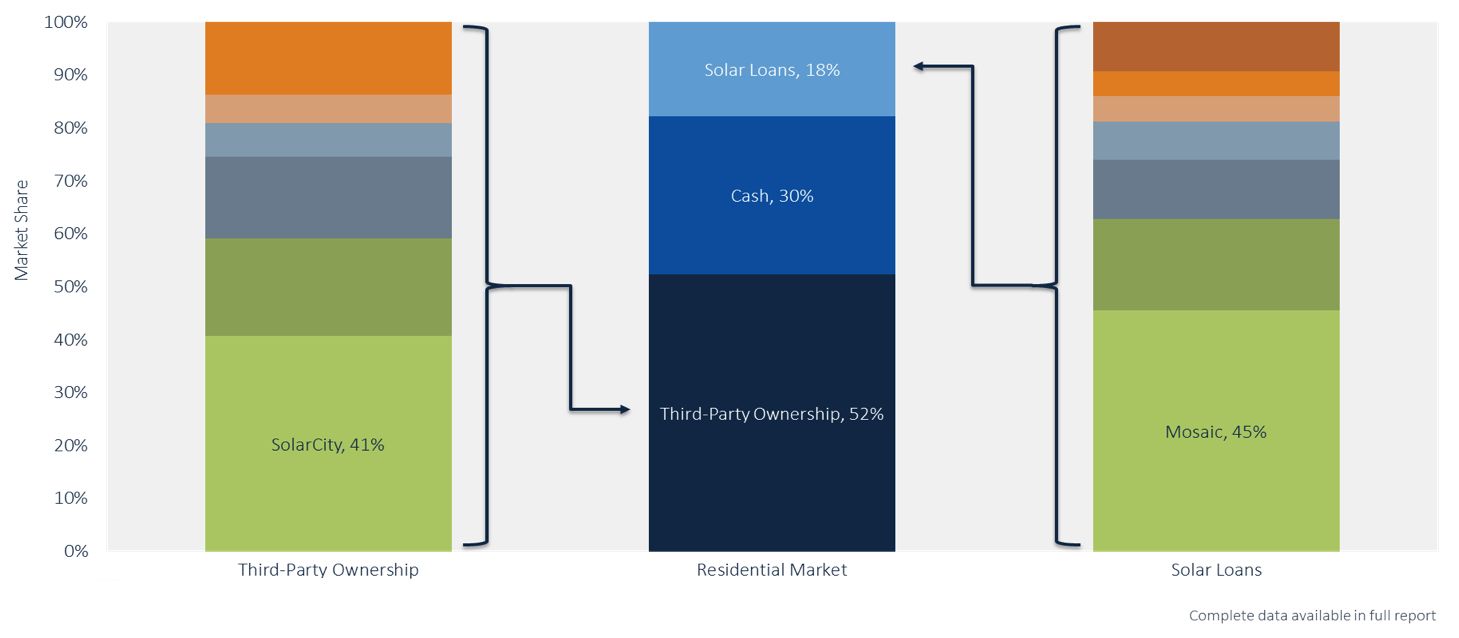

The shift to solar loans and cash

GTM Research reports that Q4 2016 was the first time since 2011 that the customer-owned share of the market was greater than 50 percent. The third-party-owned (TPO) share of the market will continue its steep drop-off in 2017 (when it is expected to fall to 41 percent) as SolarCity and Vivint increase their use of loans, and emerging markets without TPO, such as Florida and Texas, continue to grow.

Source: GTM Research U.S. Residential Solar Update 2017

Despite concerns over the supply of tax equity in the past year, the major TPO players have continued to raise sufficient financing for PPAs and leases, especially given that several of them are shifting much of their business to loans.

Securitization activity is beginning to pick up again, and yields are coming back down after spiking in 2016. Mosaic and Sunnova are the newest entrants to the solar asset-backed securitization (ABS) market. SolarCity and Mosaic issued asset-backed securities in the first quarter of 2017, and Sunnova announced its first ABS deal in April.

Additional market shifts in the U.S. residential solar market are identified by GTM's solar experts here.

***

The premier global solar conference for defining industry needs and creating new business is back for its 10th year! Join us in Scottsdale, Arizona May 16-18 for Solar Summit and Solar Software Summit 2017. Learn more here.

41

41

15

15

9

9