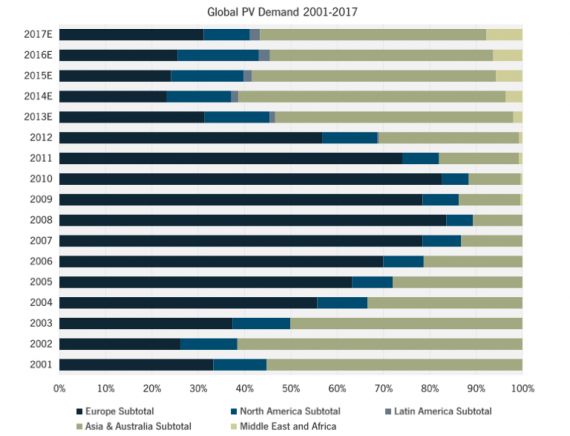

The global solar PV industry is in the midst of numerous transformations. From a broad perspective, promising solar markets are shifting from European rooftop markets toward Asian and American ground-mount markets. In parallel with this trend, PV system developers are weaning themselves off of diminishing government incentives and actively seeking a post-subsidy existence. While the ultimate outcome of the quest is likely to be a more global, more sustainable industry, the evolution creates numerous headwinds for microinverter and DC optimizer vendors, primarily an increased consciousness of system cost and favoritism toward large, centralized projects.

Source: GTM Research

In fact, despite overall installed capacity growth expected in 2013 and 2014, the crash of European PV markets has compromised the overall addressable market for most MLPE vendors. The negotiated PV module price floor in Europe only serves as an additional imperative to reduce upfront BOS costs, often at the expense of MLPE. Furthermore, new major markets in the Asia-Pacific region pose significant challenges for MLPE penetration, while other promising markets in MENA and Latin America have not yet blossomed. Thus, while the first wave MLPE survivors have successfully proven out the technology’s scalability, their growth prospects will be challenged in a stagnant addressable market.

Installations in sizable and easily addressable markets in the U.S., U.K., Australia, and Germany will achieve slower than average growth versus global totals, in large part due to the challenged markets in Europe and Australia. While MLPE starts from a small share in these countries, a tightening market means tighter competition and more price erosion on traditional products -- both of which will slow MLPE adoption, according to GTM Research's new report.

In contrast, booming markets in Asia such as China and Japan offer the promise of growth; gaining even a small share in these markets could boost MLPE’s prospects significantly. However, China’s extremely low-cost landscape coupled with a heavy favoritism for large multi-megawatt projects makes near-term MLPE adoption extremely small. While Japan sports high incentive rates and relatively costlier components (both very good for MLPE), the certification process has been incredibly difficult for foreign entities to navigate, particularly microinverters.

Nevertheless, the evolving value proposition of MLPE, coupled with additional bankability from a more strongly backed and experienced vendor landscape, will continue to push MLPE adoption forward. While older, more bullish forecasts may no longer be attainable, there continues to be a bright market for MLPE vendors, with overall MLPE growth rising from 1.1 gigawatts in 2013 to 5.1 gigawatts in 2017, representing a 46 percent CAGR over four years. Because of more rapid growth of commercial and industrial markets, GTM Research expects DC optimizers to account for 57 percent of the cumulative MLPE market between 2013 and 2017.

Source: The Microinverter and DC Optimizer Landscape 2014

From a geographical perspective, North America will continue to dominate the MLPE landscape, with nearly 50 percent of all MLPE deployments in 2013 destined for the continent. GTM Research continues to see North American share bouncing between 47 percent and 49 percent of the global market as the technology continues to gain market acceptance and expands into new territories and market segments. In 2017, demand pullback in the U.S. will compel an overall growth slowdown, and North American share will drop to 29 percent.

Source: The Microinverter and DC Optimizer Landscape 2014

***

The full report contains nine distinct forecasts through 2017 by region and market segment.

41

41

15

15

9

9