[Editor's note: this piece originally stated that the global O&M market would be worth 390 gigawatts by 2020. In fact, the number is much higher -- at 488 gigawatts. The original number was the forecast for 2019. This story has been modified to reflect that change.]

According to a new report from GTM Research and SoliChamba Consulting, Megawatt-Scale PV O&M and Asset Management 2015-2020: Services, Markets and Competitors, the global market for utility-scale PV operations and maintenance will reach 488 gigawatts by 2020, almost triple the estimated market of 133 gigawatts by the end of 2015.

“Just like the larger PV market, the global PV O&M market has been growing at a fast pace these past few years,” says report author Cedric Brehaut. “And unlike the EPC business, it remains attractive even when new construction slows, as seen in Germany, where the addressable O&M market for megawatt-scale plants exceeds 11 gigawatts in 2015 despite a drop in new megawatt-scale plant activations.”

More than half of the world’s O&M market has arisen in the last two years alone. The report identifies the distinct characteristics of markets where new installations remain the primary O&M opportunity, as in the U.S. -- versus countries where most of the addressable O&M market consists of older plants, as in Germany and Spain.

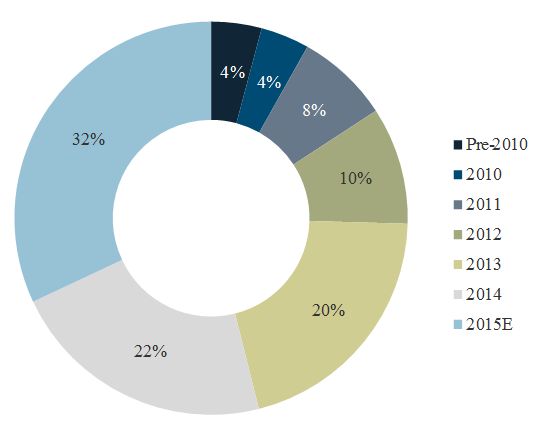

FIGURE: Global Megawatt-Scale PV O&M Market in 2015 by Plant Activation Year (Percentage of GW)

Source: Megawatt-Scale PV O&M and Asset Management

The report breaks down operations, maintenance, and asset management into three distinct services within the solar industry and analyzes the competitive landscape for each of these segments. While many vendors offer all these services, asset management remains distinct from O&M in most cases. The report notes a major trend of the decoupling of operations and maintenance, with half of analyzed O&M providers reporting different megawatt counts under operations compared to megawatts under maintenance.

“With a single vendor providing both asset management and O&M, there is no duplication of supervision and reporting functions, so arguably this results in lower staffing costs for managing the same asset portfolio,” said Brehaut. “But there are real risks that a ‘one-stop shop’ provider may not defend the interests of the owner as fiercely as would an independent asset manager.” A new trend also shows increased separation between operators and maintenance providers in certain markets because the two functions require very different competencies and infrastructures.

As the market grows, new competition emerges. GTM Research and SoliChamba Consulting segment the market into nine distinct provider types: project developers and EPCs, utilities and IPPs, investors, vertically integrated firms, inverter companies, independent service providers, and affiliated service providers. Each category has its own strengths and weaknesses.

The forecasted 488 of O&M gigawatts by 2020 will be served by a variety of business models and vendors.

***

This new report from GTM Research and SoliChamba Consulting considers 76 vendors managing over 40 gigawatts of megawatt-scale PV assets in aggregate, and analyzes the PV O&M and asset management market of 15 countries around the world.

41

41

15

15

9

9