Relatively stable market conditions and steadily improving fundamentals have given PV suppliers much to smile about over the past three quarters.

Here are five important trends identified in the June 2014 edition of GTM Research’s monthly PV Pulse data service that illustrate the solar supply sector’s recent recovery and its transition to a new growth phase heading into 2015.

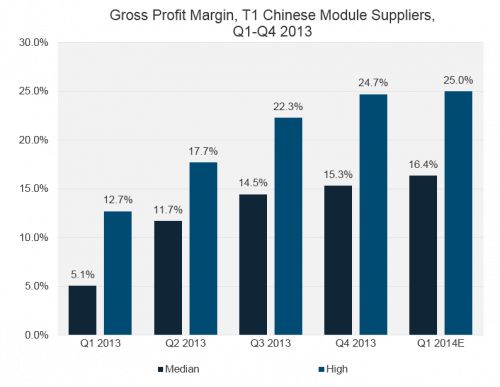

1. Profit margin expansion

Perhaps the clearest indication that supply market conditions have improved in recent quarters is the expansion in gross profit margin levels since early 2013. After languishing in the low single digits or worse through much of 2011 and 2012, the median gross margin for top-tier Chinese module suppliers (Yingli, Trina, Canadian, JA and Jinko) has improved every quarter from Q1 2013 onward, crossing 16 percent in Q1 2014 by GTM Research’s estimate.

The reason? Stable-to-up pricing in major markets combined with continuing manufacturing cost reductions, particularly on the processing (non-silicon) cost front. For Chinese module companies, a gross margin in the mid-teens is the minimum requirement for net profitability, which is what you get when you sell at $0.65/watt with a manufacturing cost of around $0.55/watt.

Of the public Chinese suppliers, one firm, JinkoSolar, has consistently recorded gross margins above its peers thanks to its industry-leading manufacturing cost ($0.48/watt in Q4 2013), achieving a margin of almost 25 percent in Q4 2013, and a similar margin profile is expected for Jinko in Q1 2014 as well.

Source: GTM Research PV Pulse, June 2014

2. Polysilicon pricing recovery

Compared to PV components (ingots, wafers, cells, modules and inverters), polysilicon manufacturing is a highly capital-intensive business, with large fixed costs dictating the need for high plant utilization levels on a constant basis. That, coupled with a relative lack of plant modularity, means that of all PV value chain segments, the solar silicon sector is intrinsically the most sensitive to excess capacity.

As a result, polysilicon experienced the most severe effects of overcapacity during the recent industry downturn, with spot prices hitting an all-time nadir of $15.9/kilogram in early 2013 -- below cash cost levels for most suppliers. Pricing remained depressed until December of last year, but has risen by 21 percent since then. With limited capacity additions expected in 2014, GTM Research expects pricing to be in the $21-$26/kilogram range for the remainder of the year.

Next year, especially the second half, could be another story, with significant volumes of additional capacity from the likes of Daqo New Energy, Tokuyama and Wacker ramping up to full utilization levels by then. However, many of these new plants would employ more modern, cost-effective technology than older plants, and could sustainably sell into the market at less than $20/kilogram -- which would keep silicon’s contribution to solar module and system costs below 10 cents per watt.

Source: GTM Research PV Pulse, June 2014

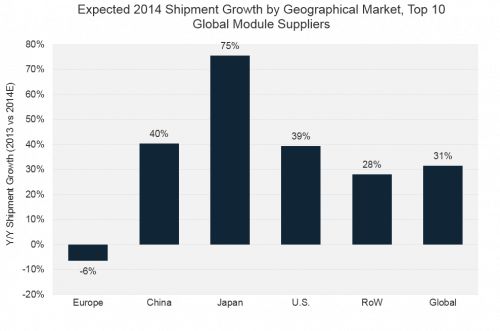

3. Aggressive shipment guidance

Growth in shipment volumes is not necessarily an indicator of health in the PV supply chain; most if not all PV suppliers were able to achieve this even amidst the recent industry downturn. However, where shipment increases in previous years came at the expense of precipitous declines in selling prices (hence the phrase “profitless prosperity”), no such elasticity will be required to trigger growth in 2014, as demand growth is expected to be robust even under a stable-to-up pricing environment.

Taken together, the top ten global module firms currently expect overall shipment growth of 33 percent in 2014. In particular, shipments to Japan, which has the highest module prices in the world, are expected to grow by 75 percent, with strong growth also expected out of China, the U.S. and Latin America.

Source: GTM Research PV Pulse, June 2014

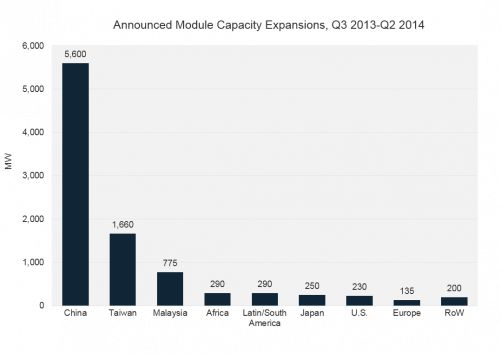

4. Capacity expansions

Overcapacity cast a dark and gloomy shadow over the PV supply sector for the better part of the last three years. It was understandable that adding more manufacturing capacity was the last thing on PV suppliers’ minds during that period. Precious few expansions were carried out and practically no new facilities were constructed.

However, things have changed radically on this front over the last nine months. Beginning in Q4 2013, there has been a spate of announcements by suppliers, both established and emerging, across the value chain.

Whereas expansions in China are mostly being carried out by acquiring or buying second-hand equipment from weaker suppliers, firms based in Taiwan and Malaysia are installing new production lines. Additionally, a number of small module assembly plants have been announced with the aim of serving markets that directly or indirectly favor locally produced modules. Examples include JA Solar’s 150-megawatt joint venture in South Africa, Pure Energies in Brazil, and ReneSola’s planned 80-megawatt plant in Japan.

Overall, the resumption of manufacturing expansions and capital spending (albeit at highly muted levels compared to 2009-2011) signals that supplier market confidence has returned, and that the sector is gearing up for a new growth phase leading into 2015.

Source: GTM Research PV Pulse, June 2014

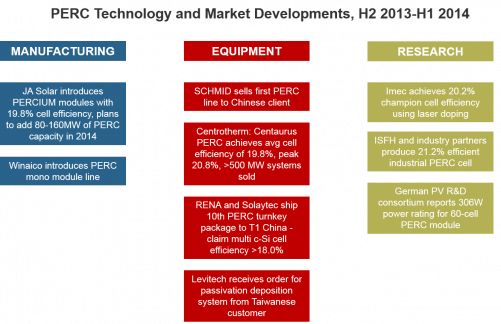

5. New technology investments

With supplier balance sheets severely eroded and cash at a premium, investments in new manufacturing technology concepts came to a virtual standstill during the recent industry downturn. Improvements in key performance metrics such as conversion efficiency and silicon utilization were incremental and achieved using approaches that required minimal capital investment (e.g., greater use of virgin polysilicon, advanced metallization pastes, and central sorting of ingots).

The last six months have not only seen a pickup in capacity spending plans, but an increased desire on the part of suppliers to invest in new technology concepts that have a greater potential to drive lower costs and higher efficiencies.

In particular, the passivated emitter with rear contact (PERC) cell concept seems to have gathered momentum all of its own, as the table below shows. PERC combines advanced front-side wafer texturing with rear-side passivation, and has consistently been suggested as a relatively low-cost way to produce crystalline silicon cells at greater than 20 percent efficiency (the record cell efficiency is currently 21.6 percent).

Announcements relating to investment in PERC have come steadily in recent quarters from both equipment vendors and manufacturers, and tool orders are likely to accelerate leading into the second half of 2014 and 2015. Given that much of the easy work relating to efficiency improvement and cost reduction has been done in recent years, investment in next-generation technologies such as PERC, advanced metallization and fluidized bed reactor (FBR) polysilicon will be necessary for continued progress on these all-important metrics going forward.

Source: GTM Research PV Pulse, June 2014

All data and graphics in this article are excerpted from PV Pulse, GTM Research's monthly global PV market tracker. For more on the Pulse, click here.

42

42

15

15

9

9