Europe may lag the United States and China in terms of overall smart grid investment, but it’s still a multi-billion-dollar market for smart meters, distribution automation, and the next wave of distributed, renewable energy integration. And while U.S. smart grid investments have been falling over the past year, Europe’s investments are growing.

So says the European Commission’s Joint Research Centre, which this week released a report tallying more than 450 projects representing a collective investment of €3.15 billion ($4.28 billion) across the 28 EU member states, plus Switzerland and Norway.

That tally includes 50 new projects, worth a combined €475 million ($646 million), that have started since the JRC’s last report, which covered projects through late 2012. Over that time, 400 new companies entered the smart grid sector.

JRC’s Smart Grid Projects Outlook 2014 report also includes new interactive visualization tools -- including this cool map showing region-by-region spending across Europe over the past decade.

Bloomberg New Energy Finance labeled Europe the “sleeping giant” of smart grid in its February report on 2013 industry investment, noting the progress of large-scale smart metering contracts in Spain, France and the U.K., as well as growing spending on distribution grid monitoring and control systems, demand response and green energy integration.

JRC’s report doesn’t specifically include smart meter projects, which added up to nearly €5 billion as of its latest tally. It's calculating those separately in a report set to be released later this year. But it does highlight a number of projects that are tying together smart meters, consumer engagement, distributed energy resources, electric vehicle charging and other grid edge systems. Here are the highlights from the report.

Investment is coming across a broad set of grid imperatives

JRC's report uses several key categories to organize its hundreds of projects. Most investment is going into "smart network management," which includes "increasing the operational flexibility of the electricity grid, like substation automation, grid monitoring and control," and the like.

Smart customer and smart home technologies take second place, followed by aggregation of demand-side resources like virtual power plants, integration of distributed energy resources, electric vehicle integration, and large-scale renewable energy integration:

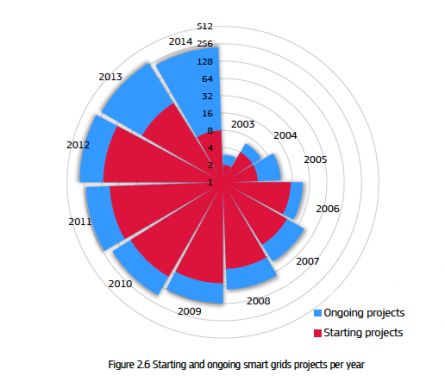

Growth remains strong, despite some slight drop-off from previous years

JRC's report makes clear that it shouldn't be compared directly to its previous surveys of Europe's smart grid activity, as some of its reporting methods have changed over the years, and because several projects that got underway couldn't be counted in its most recent figures. That's what makes last year look slightly off compared to 2012 in this graph representing investment growth over the past decade.

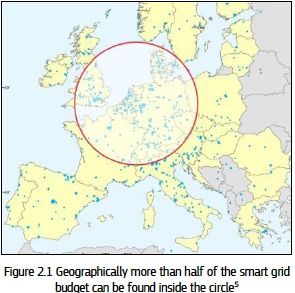

Spending on smart grid projects is spread unevenly across the continent

While JRC has counted up more than 500 project sites across the 30 countries it surveyed, more than half of the investment has taken place within the circle shown below. More than half the spending comes from France, Germany, the U.K. and Spain, while Denmark has the lead on its neighbors in terms of projects and spending on a per-capita basis.

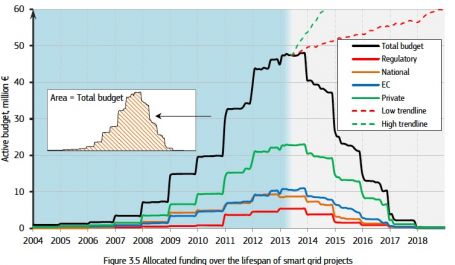

Private investment is growing, but government backing still remains critical

The share of smart grid investment coming from the industry rose to 49 percent, up from 45 percent in JRC's previous report. Still, nearly nine out of ten projects are receiving public funding of one kind or another, indicating the critical role of government in moving R&D work into the "D&D" (demonstration and deployment) phase of development.

Regulatory funding mechanisms are still rare

Out of the 51 percent of public funding for European smart grid projects, 22 percent has come from the European Commission, while another 18 percent has come from national governments. Only 9 percent has come from regulatory mechanisms, such as rates and tariffs. That will obviously have to grow in order for smart grid investments to become part of the way a typical utility or energy services provider does business, and to allow new projects to come on-line to start bolstering growth in future years, as the following chart indicates.

41

41

15

15

9

9