This is the second piece in a four-part series offering insights and perspectives from GTM Research's latest smart grid report, Electric Vehicles 2011: Technology, Economics, and Market. To read part one, click here. To see the report's co-author speak on this topic at The Networked EV, register today!

In 2005, Bill Ford, Chairman of the Ford Motor Company, said that his company intended to build up to 250,000 hybrid-electric vehicles (HEVs) by 2010 -- the actual number turned out to be 35,496. In 2008, J.D. Power and Associates estimated that 600,000 HEVs would be sold in 2009; actual sales reached a little more than 290,000. Forecasting market growth is difficult in any industry, but the automotive industry seems to be a particularly tricky sector. With the emergence of the first electric vehicles for the mass market, the fortunetellers are back on stage, leading CNN Money to headline a recent article “Lies, Damned Lies, and Electric Vehicle Forecasts.”

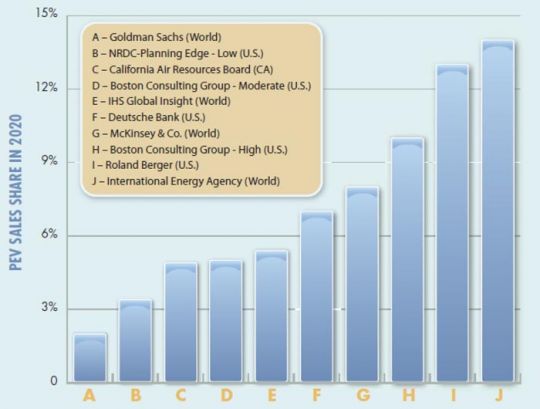

The California Plug-In Electric Vehicle Collaborative has compiled recently published electric vehicle forecasts, showing market penetration rates of plug-in hybrid-electric vehicles (PHEVs) ranging from two percent to 14 percent by 2020. Goldman Sachs ('A' in the figure below) forecasts that there will be 2.0 million PHEVs and 1.7 million BEVs sold in 2020, while the International Energy Agency ('J' in the figure below) puts these numbers at 5.0 million and 2.0 million, respectively. Both organizations arrive at their conclusions based on total vehicle sales of 100 million units and battery prices of $300 to $450 per kilowatt-hour. This illustrates that forecasts can be massively disparate, even when derived from the same assumptions about key variables.

Figure: Third-Party Forecasts of EV Fleets in Different Regions

Source: California Plug-In Electric Vehicle Collaborative

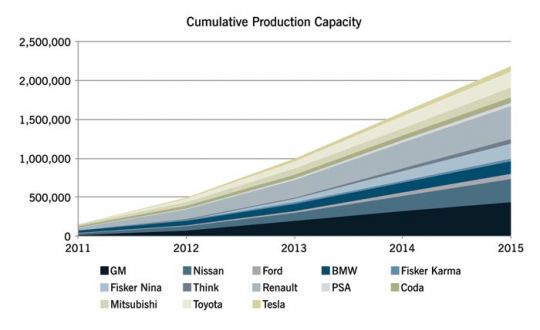

So what is the problem with such forecasts? In our view, the root of the problem is what we call excess demand hypothesis. According to this model, demand will greatly exceed the supply or production capacity of a technology in the years to come, and growth in technology deployment therefore equals the rate at which production capacity expands. Conveniently, this approach reduces an analyst’s task of forecasting industry size to estimating production capacity (as GTM Research did in the graph shown below), which depicts production capacity as announced by major vehicle manufacturers as of mid-2011.

Figure: Cumulative Production Capacity by Car Manufacturer

Source: GTM Research

It is important to realize that this type of supply-side analysis is prone to two fundamental biases. First, it tends to be incomplete. For the most part, production capacity forecasts are available only from first-movers with a strong strategic focus on electrifying their product portfolios. General Motors and Nissan, for instance, are frequently releasing statements about changes in production capacity for their Volt and LEAF models, as they compete head-to-head for share of voice in the marketplace. At the same time, laggards are often excluded, even if they represent a significant share of the global car market (e.g., Volkswagen).

Second, supply-based forecasts are often inaccurate. Announced production capacity rarely equals actual production, as can be seen by the massive delays in delivering the Nissan LEAF and Fisker Karma. In addition, car companies can and will adjust production capacity dynamically in reaction to market demand. On May 11, 2011, for instance, General Motors announced that it was going to increase the production capacity of its Chevy Volt and Opel Ampera to 60,000 annually, up from 45,000.

GTM Research believes that the excess demand hypothesis might hold for electric vehicles -- but only in the short term. There are a good number of early adopters eagerly waiting for their LEAF or Volt to be delivered, but it remains unclear how many followers there will be once the early adoption phase is over. Ultimately, sales will be determined by both supply and demand, and estimates on both sides of the equation are fraught with uncertainty, as the electric vehicle ecosystem is complex and dynamic.

This raises questions about the utility of forecasts in general. Does it really matter if there are three, five, or eleven million EVs on the road by 2015? We believe it does not. The electrification of transportation is inevitable, but it might happen at a slower pace than many think. The reasons for this are presented in our report, Electric Vehicles 2011: Technology, Economics, and Market. In the meantime, readers must judge for themselves what to make of Google.org’s latest prediction that EVs will account for 90 percent of all vehicle sales by 2030.

41

41

15

15

9

9