Wind power is all the rage in Texas. The Electric Reliability Council of Texas is the nation’s leader in wind development, with over 22 gigawatts in operation on a 70-gigawatt peak system, according to S&P Global.

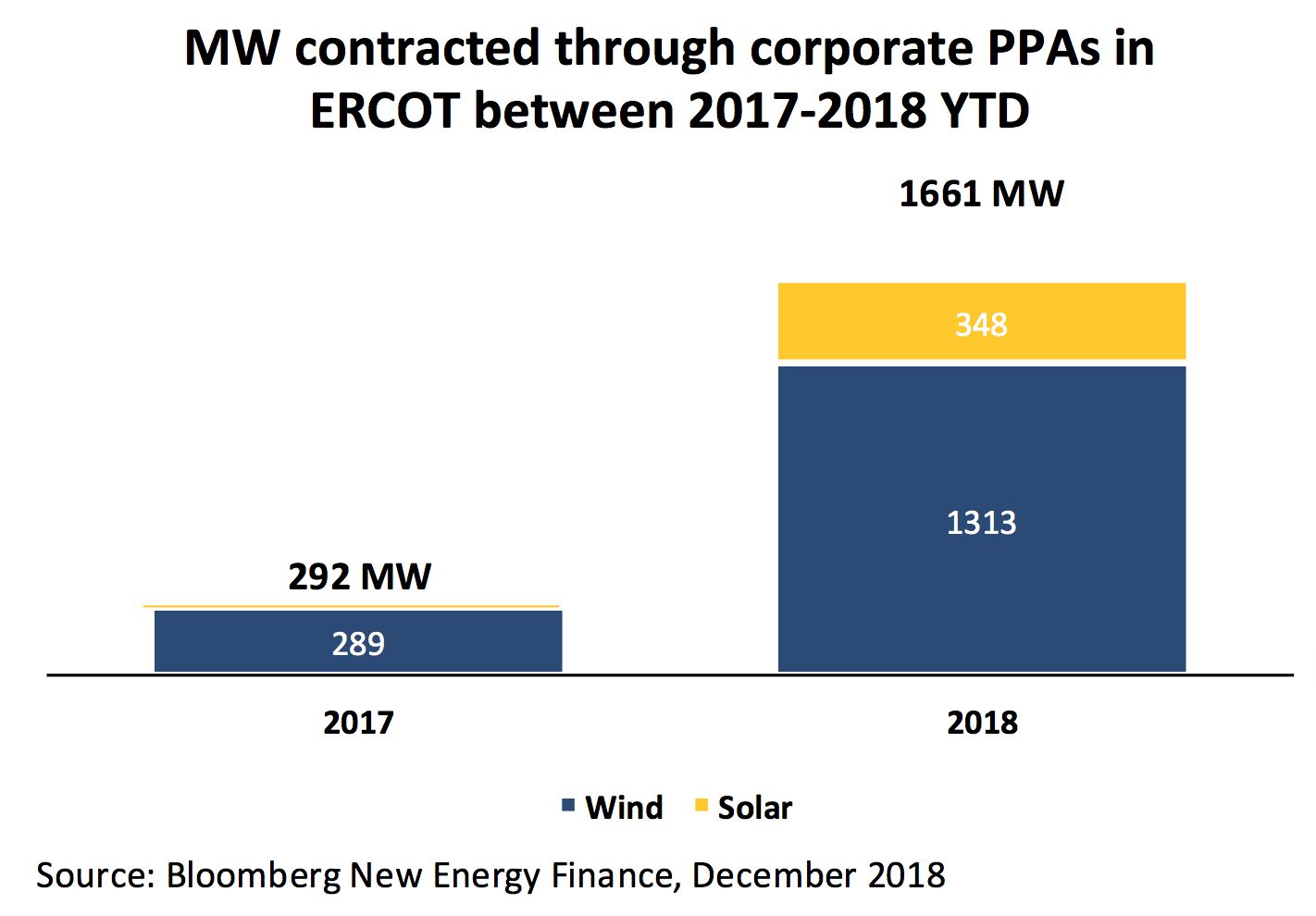

In recent years, there has been an influx of interest from corporations to procure renewable energy in ERCOT, particularly from new players who wish to settle financially in the market. Nearly 2 gigawatts of corporate renewable energy deals have been executed in ERCOT territory in the past two years. Of the 2 gigawatts, 81 percent has been wind.

Corporates procuring Texas-based renewable energy to satisfy sustainability goals typically do so by signing long-term power-purchase agreements (PPAs), with either a wind or solar company that is developing new projects in the region. The PPA guarantees a dependable, long-term, flat revenue stream for the new power plant and allows corporates to lock in power prices that are lower than the expected value of electricity. Win-win for both entities.

Interestingly, corporates have disproportionately favored wind generators that take advantage of the federal Production Tax Credit (PTC), which has allowed wind developers to offer extremely low electricity prices to these corporations.

But the PPA price is not the only important variable. To their detriment, corporates have been ignoring the wind generation profile and the fact that it is not as valuable as the solar generation profile.

Are corporate customers making the best financial decision when it comes to these complex, multimillion-dollar contracts? Are corporate customers leaving millions of dollars on the table by pursuing cheap wind PPAs rather than solar?

Wind's historical advantage in ERCOT

To answer these questions, let's first take a look at how the ERCOT market is set up.

ERCOT is a deregulated and highly liquid electricity market. Cheap capital, strong solar irradiance and wind resource, load growth, and upward trending electricity price forecasts make this an attractive renewable energy to both buyers and sellers — despite a lack of statewide carbon or clean energy policies.

Given that ERCOT is not compliance-driven, unlike many of the other leading renewable energy markets such as CAISO or ISO-NE, buyers will only purchase power if the levelized cost of energy for a new power plant or PPA rate is lower than the expected market price of energy. This dynamic this keeps gas and solar from being overbuilt.

If a hypothetical combined-cycle gas turbine in Houston can run at a marginal cost of $35 per megawatt-hour, but the levelized market revenue in its region is expected to be $30 per megawatt-hour, the CCGT plant is expected to lose $5 per megawatt-hour. Thus, the CCGT power plant’s developer is likely not going to receive the sufficient price signals to incentivize future development.

Wind is the exception to this market condition because the PTC allows wind build-out to continue well after the market price of energy is driven below the levelized cost of wind. The PTC is monetized on a generation level, and the developer receives approximately $24 per megawatt-hour (post-tax). Therefore, a wind developer has a cushion of $24 for every megawatt generated, and can still make a profit if regional prices were to drop below wind’s marginal cost to run (which is zero).

Despite wind’s policy advantage, the rapid cost decrease in solar technology has allowed solar to become very competitive in the market and deliver high value to both developers and power purchasers. Roughly 2 gigawatts of utility-scale solar PV is operating in ERCOT with a forecast of 8.2 gigawatts to be operating by 2025, according to Wood Mackenzie's North America Power & Renewables tool. A sizable portion of this demand will come from C&I customers.

In 2018 alone, more than 1.6 gigawatts' worth of corporate renewable PPAs were signed in Texas. Demand is expected to increase going forward as corporates seek to reach their sustainability goals.

Corporates chase low-priced wind PPAs

The corporate customer segment is diversifying beyond the traditional renewable buyers: tech companies with renewable goals and/or data center load. Telecommunications, retail, manufacturing, consumer packaged goods and healthcare companies are starting to set aggressive renewable energy goals and have subsequently accelerated their procurement efforts. Corporations with no in-house renewables procurement teams often seek to contract renewable energy with the help of a third-party adviser or broker.

There is a strong economic impetus for corporations to procure renewable energy, as they seek to hedge their exposure to future power prices and obtain renewable energy credits to reach their carbon and/or renewables targets. A majority of the large-scale corporate deals executed to date have been structured as virtual power-purchase agreements. Under this structure, when the floating price is below the contract price, the buyer (corporations) must make the seller (developer) whole, up to the PPA price. When the floating price rises above the contract price, the seller passes the excess revenues to the buyer.

Corporate customers have historically chased the low wind PPA prices before the wind shape was exhausted. But value is no longer tied to a low PPA price, but rather the healthy spread between the PPA and market prices.

A more valuable solar shape

Solar and wind generators produce at no marginal cost and sometimes are incentivized to produce when excess supply exists. When the sun shines and the wind blows, renewable energy plants are generating, leaving less demand to be met by traditional power plants. Consequently, when there is an oversupply of the negative- or zero-cost units setting the marginal prices, wholesale market prices decline.

The PTC has artificially inflated the value of wind, leading to high saturation levels. As a result, the overall value of a wind PPA is decreasing with each incremental megawatt of wind built. The decreasing PPA value is more dramatic for wind, considering the relative build-out compared to solar and wind’s negative covariance with load in Texas. Wind capacity makes up 23 percent of ERCOT capacity versus 2 percent for solar.

Wind in Texas is negatively correlated with load, whereas solar generation has a strong positive correlation with load. This would supposedly be undone if solar becomes overbuilt, but it is nowhere near the penetration level necessary to depress prices. It took roughly more than 10 percent of solar penetration in CAISO before solar began cannibalizing its own prices.

Texas is the only state with forecasted load growth, which speaks to the solar shape’s increasing value. Wind in ERCOT, however, blows disproportionately at night in the spring and fall, when demand for electricity is low. Similar to what is occurring in CAISO, the high amount of penetration has led to a suppression of prices when capacity is abundant and load is low. The inverse relationship between the wind generation and load in ERCOT makes the wind shape less valuable than the solar shape.

In ERCOT, solar and wind generators make their profit from a handful of hours, particularly when demand and generation are high. Summer days in Texas are a recipe for scarcity pricing due to strong growth in electric demand when the temperature rises and the sun is shining. ERCOT has set midday demand records, nearing price maximums of $7,000 per megawatt-hour in 2018 as the summer heat broke state records.

This creates tremendous opportunity for solar to capture this upside value because the solar shape matches load in Texas. Wind generation, meanwhile, tend to slow down during hot summer days in Texas.

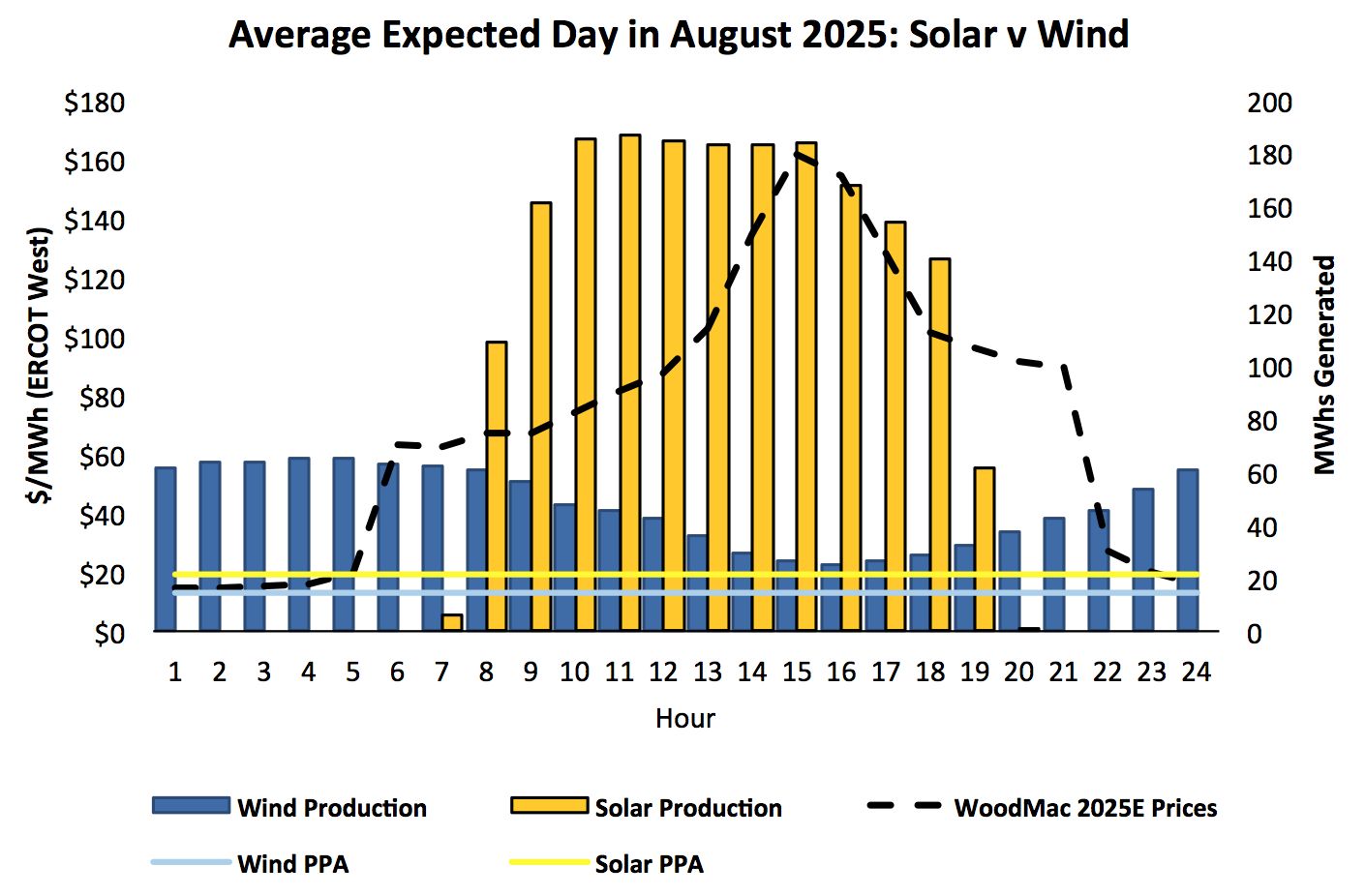

The below graphic represents a typical day in August comparing the solar and wind shape (based on same annual generation) in West Texas, versus Wood Mackenzie’s forecasted 2025 West zone prices. Solar’s peak production correlates with higher market prices, contrary to the wind shape, which produces when prices are low.

Given the strong positive correlation between sunlight, demand and rising peak power prices, the solar shape proves to be much more valuable to the customer than wind, despite the higher PPA price.

Source: Sarah Krulewitz/Wood Mackenzie

The solar shape captures hours where operating reserve demand curves are applied. An ORDC, which is a price adder, is put in place to ensure that electricity prices accurately reflect shortage conditions. The ORDC adder is active when ERCOT’s operating reserves decrease below 6 gigawatts, with the maximum adder applied when reserves drop to 2 gigawatts.

In anticipation of approximately 4 gigawatts of coal plant retirements in ERCOT, buyers are working to execute solar deals that come online as soon as possible to capture the expected upside during the summer months. In ERCOT’s recently released capacity report, summer reserve margin forecasts decline from 10.7 percent in 2020 to 7.5 percent in 2023, opening the door for more than 3 gigawatts of additional capacity needed. These tightening reserve margins leave solar plants well equipped to capture high margins in the summer when wind cannot.

A solar PPA may be more profitable by $24 million

With renewable PPAs clearing below the forward curves, buyers are expected to earn a margin on their renewable purchase and enable developers to hit their rate of return. Renewable PPAs are currently priced at a $5-$20 discount to the levelized on-peak forward contracts, which are trading in the mid $30s.

Today, wind PPAs in ERCOT are priced between $12 and $17 per megawatt-hour, compared to solar PPAs, which are priced between $20 and $28, varying by project location. Wind developers are offering rock-bottom PPA prices in hopes of contracting and building their projects prior to the sunset of the Production Tax Credit in 2019. When this $24 per megawatt-hour (post-tax) government subsidy expires, wind developers are not able to depend on a reliable revenue stream that allows them to still recoup their upfront capital investment in a roughly seven to nine years time frame.

For corporate customers with little to no load in deregulated markets, the low sticker price of wind PPAs appear to offer the best value. But this is not always the case.

In a hypothetical scenario, when comparing a standard, unit-contingent contract for differences, a $13 per megawatt-hour wind PPA and $20 per megawatt-hour solar PPA in ERCOT, settling against Wood Mackenzie forecasted West Hub prices, the generation-weighted value of the solar production shape is roughly $4 higher than wind’s.

In this scenario, the expected customer profit for a 12-year solar PPA is approximately $110 million, versus a wind PPA’s expected profit of $86 million. Under this Wood Mackenzie forecast, a solar PPA may potentially be more profitable by $24 million.

|

|

Solar |

Wind |

|

PPA Rate ($/MWh) |

$20 |

$13 |

|

Term (Years) |

12 |

12 |

|

Commercial Operation Date |

1/1/2019 |

1/1/2019 |

|

Annual MWh |

~585,000 |

~585,000 |

|

Avg Generation Weighted Value per MWh ($/MWh) |

$16.54 |

$12.31 |

|

Customer expected profit (CFD) over life of the contract (Wood Mackenzie ERCOT West Expected Prices) |

$110 MM |

$86 MM |

Corporates may be missing out on a bargain with solar

Between rising forecasted on-peak power prices, increasing load growth, and declining reserve margins, the solar shape continues to become more valuable in ERCOT. The value proposition is high for solar, while wind has reached a point of diminishing returns. Due to the dynamic of the ERCOT market, solar will not suffer the same repercussions as severely as wind.

Corporate customers may be taking unwarranted risk by continuing to chase the low-priced wind PPAs in ERCOT. While the face value of the product is lower than that of solar, customers must evaluate the value of the shape of the product they wish to procure. By purchasing wind, corporates may continue to leave tens of millions of dollars on the table.

***

Sarah Krulewitz is an analyst at Recurrent Energy and a Fall 2018 Clean Energy Leadership Institute fellow.

41

41

15

15

9

9