Large national solar installers may have better brand recognition and the backing of Wall Street banks, but they lag in one crucial area: pricing.

In fact, quotes from big installers are 10 percent higher than those generated by mid- and small-sized installers in the U.S., according to a new analysis from NREL. That amounts to 37 cents per watt on average -- more than the cost of an inverter and racking combined.

That can mean thousands of dollars in additional cost to the homeowner.

So what gives? Why are large installers pricing their installations so much higher than their smaller, local competitors?

It's a complicated question to answer. The NREL researchers mostly speculate about competitive forces and consumer education. However, customer acquisition and overhead costs also play a role (more on that below).

First, it's helpful to understand how the data was collected and analyzed. The quotes came from EnergySage, an online marketplace that compares offers for homeowners considering solar. The researchers collected 1,588 quotes on the platform from a range of installers. They classified "large" installers as companies that have deployed more than 1,000 systems in a year between 2013 and 2015. (According to GTM Research's calculation, installers of that size make up 39 percent of total U.S. residential market volume.)

They also narrowed in on the type of transaction. Many of the largest national installers provide leases and power-purchase agreements, while local installers tend to rely more on cash purchases and loans. The researchers only focused on quotes for purchase prices in order to make a direct comparison between installers.

Large installers accounted for 176 quotes and "non-large" installers accounted for 1,412 quotes. Many of the price quotes from large installers came from outside the EnergySage platform and were later uploaded by customers.

"Because EnergySage prompts customers to voluntarily upload quotes they received from installers outside of EnergySage (e.g., the large installers), NREL was able to compare large installer quotes vs. non-large installer quotes given to the same customer and rooftop. That is what makes this study so special and unique -- NREL was able to keep all factors constant, other than the installer size," said Nick Liberati, the communication manager at EnergySage, in an email.

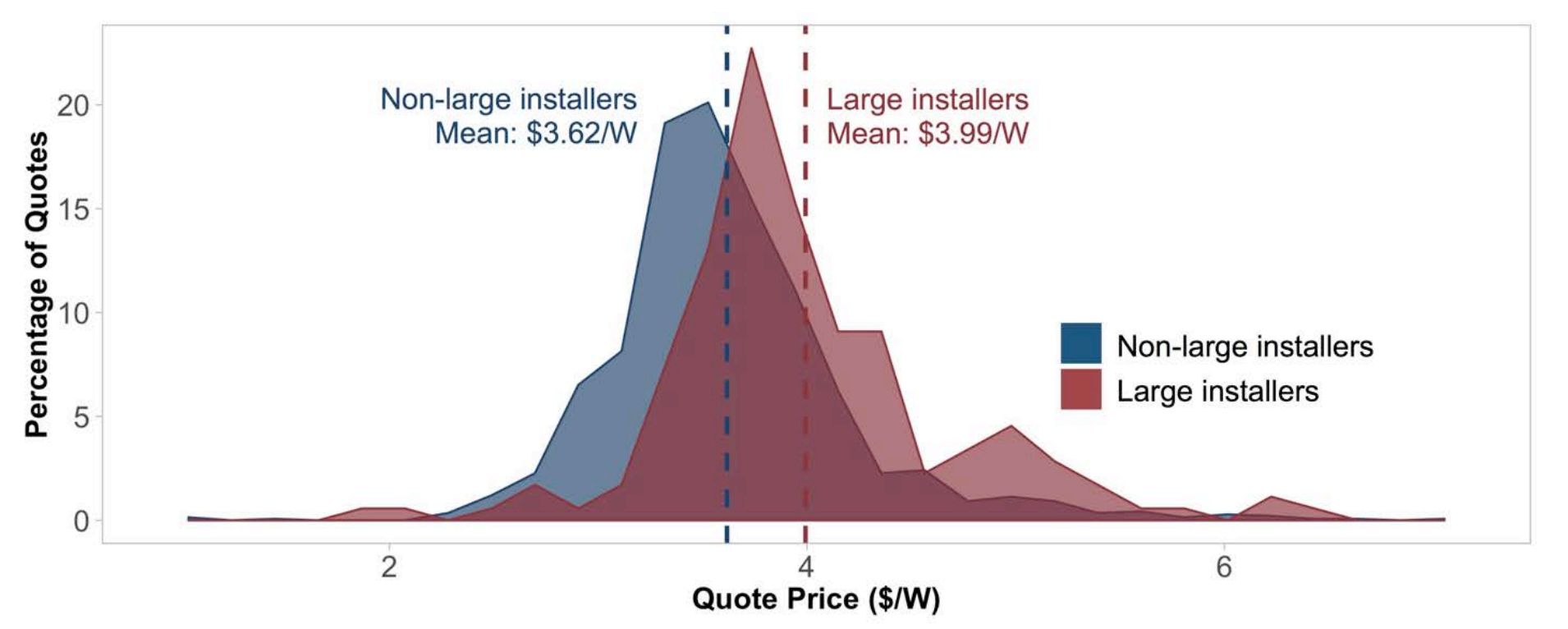

Here's what the researchers, Eric O’Shaughnessy and Robert Margolis, found after comparing pricing: "Large installer quotes are, on average, about $0.37/W higher than non-large installer quotes in the full data set. Large installer quotes also exhibit greater price variation, with a span of $1.61/W between the 10th and 90th percentile of large installer prices, compared with a span of $1.25/W for non-large installer prices."

(Source: NREL)

The researchers also paired quotes directly against each other: "For example, suppose a customer receives three quotes. Quotes 1 and 2 from non-large installers are $3.30/W and $3.70/W, respectively. Quote 3 from a large installer is $3.50/W. The customer has two possible pairings of large and non-large installer quotes: quote 3 (the large installer quote) with quote 1, and quote 3 with quote 2."

This approach yielded 707 pairs of quotes from 142 customers. This method showed that large installers are quoting system prices 33 cents per watt higher than their smaller competitors.

While helpful, these two comparisons don't take into account differences in equipment and system sizing. So O’Shaughnessy and Margolis controlled for these factors to find the residual value.

"Large installer quotes are associated with smaller system sizes, earlier quote dates, and they are more likely to be external. The model results also suggest premiums of about $0.08/W and $0.14/W for microinverters and optimizers, respectively," they wrote.

The differences between installers aren't as wide under this approach, but they are still significant.

"On average, large installer quotes are $0.19/W higher than predicted by the model, while non-large installer quote prices are $0.02/W lower than predicted by the model. The average difference in residual values between paired large and non-large installer quotes is about $0.17/W , or about $0.21/W when controlling for hardware."

(Source: NREL)

O’Shaughnessy and Margolis illustrated quite clearly (using this single data set at their disposal) that smaller installers offer better pricing than bigger installers for purchased systems. But they didn't answer why. They could only speculate. Mostly, they focused on the competitiveness of markets and product differentiation -- two important, but still incomplete, explanations.

Here's what they wrote about competition: "In markets where at least one large installer is active, small installers are more likely to compete against at least one other installer (the large installer) than are large installers. In other words, large installers may expect to compete against fewer rival bidders for any given customer than small installers. Consistent with the bidding literature, this fact would incentivize large installers to bid higher prices than small installers."

They also considered branding advantages: "Large installers with larger customer acquisition budgets and longer established reputations may be able to more successfully differentiate their products than non-large installers. A perceived quality of large installer systems, whether real or illusory, could allow large installers to bid higher prices."

Both of these factors do play a role. But there are other structural challenges associated with the national residential solar model.

Customer acquisition costs are stubbornly high for top national installers -- hovering between 58 cents per watt and 62 cents per watt. In the first quarter of last year, SolarCity and Sunrun saw their customer acquisition costs rise to 90 cents per watt.

Operating across different states also raises the cost of business. Although national installers avoid distributors and buy equipment directly, their overhead costs are still much higher than localized firms.

Finally, financing costs are a factor. Smaller installers tend to rely on cash purchases. Bigger installers tend to offer loans, which raise the price tag because of dealer fees.

While the reasons for pricing differences between different sizes of installers are complex, the study's broader conclusion study is simple. Consumers should be comparing more quotes -- because a big brand name won't necessarily be the cheapest.

"Our results suggest that customers could benefit from obtaining more quotes before making a decision, and all customers could benefit from increased competition," wrote O’Shaughnessy and Margolis.

Join GTM for the 10th Annual Solar Summit & 2nd Annual S3 Solar Software Summit in Arizona May 16-18. We’ve got the biggest names in the solar industry confirmed to attend and speak. And we've got a packed agenda of topics including solar software, energy storage, finance, community solar, corporate procurement, balance of systems, and much more. Check out the event site here.

41

41

15

15

9

9