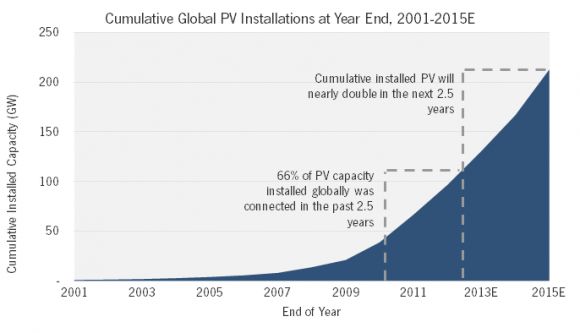

If you want to understand why people so often compare deployment trends in solar photovoltaics (PV) to Moore's law in computing, consider this statistic: two-thirds of all solar PV capacity in place worldwide has been installed since January 2011.

Let's put that into perspective. It took nearly four decades to install 50 gigawatts of PV capacity worldwide. But in the last 2 1/2 years, the industry jumped from 50 gigawatts of PV capacity to just over 100 gigawatts. At the same time, global module prices have fallen 62 percent since January 2011.

Even more amazingly, the solar industry is on track to install another 100 gigawatts worldwide by 2015 -- nearly doubling solar capacity in the next 2 1/2 years.

Those statistics and the chart below, courtesy of GTM Research Senior Analyst MJ Shiao, illustrate the exponential growth in the global PV market.

Source: GTM Research

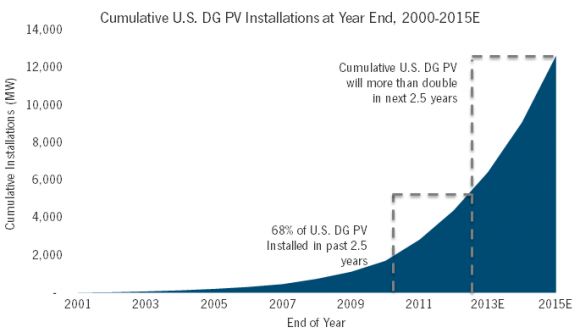

And as Shiao's second chart below shows, the U.S. distributed solar market is on pretty much the same growth trajectory. More than two-thirds of America's distributed PV (everything except for utility-scale projects) has been installed since January 2011. And by 2015, the country's distributed PV market is expected to jump by more than 200 percent.

Chart: GTM Research/SEIA U.S. Solar Market Insight

There are a few key takeaways from these figures.

First, utilities still dismissing solar as inconsequential or "cute" may soon be in for a rude awakening. According to the Solar Market Insight report from GTM Research and SEIA, the national average for residential system prices fell another 18 percent last year; non-residential prices fell 13.3 percent.

The falling cost and price of installation is starting to open up new markets without incentives. As Shayle Kann, vice president of GTM Research, pointed out recently, roughly 3,000 residential solar systems were installed in California without the use of any state incentives in the first quarter of this year.

"This is emblematic of a sea change in the solar industry, and even more importantly, in the energy industry," wrote Kann.

But this rapid increase in installations won't create challenges for just utilities -- it will also create challenges for the solar industry itself. Since the solar market is still at the beginning of a steep growth curve, it's hard to say whether the business models and technologies we know today are going to be successful in the future.

This will likely mean more bankruptcies and more consolidation. It will also test the reliability of products operating in the field.

Because two-thirds of PV capacity in the field today was only installed in the last couple of years, a majority of the products are still very new. Solar is a multi-decade investment, and there is uncertainty around how new hardware will perform over the long term, explained Shiao.

"We're really at the beginning stages of understanding PV in terms of products in the field, viable business models, and effects on the grid, especially when you consider that PV is being sold many times as a twenty-year asset. Now is the time to look deeper into issues surrounding product reliability, market sustainability and O&M business models."

The boom in distributed solar is underway. And we've only just begun to understand the implications.

For more on product performance, check out the PV module reliability scorecard from GTM Research and PV Evolution Labs. And for more on U.S. solar trends, read the U.S. Solar Market Insight report.

41

41

15

15

9

9