GTM Research's just-released white paper looks at the impact of utility rate design on distributed solar project economics and shows that tariff design can to make or break PV project economics.

Solar is particularly susceptible to rate design as the industry begins its transition to a post-subsidy reality.

Though less frequently discussed than net metering, rate design is an equally important issue in the brewing battle between PV advocates and utilities. Yet one important piece of this debate that we’ve yet to discuss is the capacity caps placed on “solar-friendly” tariffs in California.

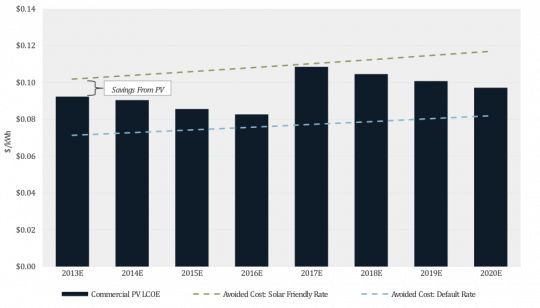

As highlighted in the free report, Rate Design Matters: The Impact of Utility Tariff Structure on Solar Project Economics, solar-friendly tariffs currently available in Southern California Edison (SCE) and San Diego Gas & Electric (SDG&E) territory allow commercial solar to be cost-competitive with retail rates even without any state-level incentives. Considering only the 30 percent Investment Tax Credit (ITC) and accelerated depreciation, SCE customers who opt in to the solar-friendly Option R tariff (TOU-GS-3-R), instead of the default commercial rate (TOU-GS-3-B), can avoid an additional $0.03 per kilowatt-hour -- enough to push installed PV over the grid-parity tipping point to positive project economics.

Figure: Commercial PV Economics in Southern California Edison Territory

In a recent settlement of the California IOU's 2012 General Rate Case, SCE and SDG&E agreed to continue to offer solar-specific tariffs. However, the California Public Utilities Commission did not require the megawatt cap for these programs to be lifted, which essentially closed the programs to new entrants. It’s estimated that the 150-megawatt cap for SCE’s Option R program will be met before the end of the year (it currently stands at just 21 megawatts); once that occurs, the next best rate structure significantly reduces the economic value of commercial solar. Though commercial customers may be able to capture attractive project returns now thanks to the California Solar Initiative, as state-level incentives are phased out, an average SCE customer on the default rate is not likely to achieve parity in the near term.

As evidenced in recent studies, distributed generation and net metering have the potential to benefit all utility customers, not just those with installed solar. Yet the debate surrounding rooftop solar will continue as PV penetration increases and utilities and consumers continue to search for an equitable solution.

41

41

15

15

9

9