Solar PV costs are still falling rapidly in the United States, but further cost reductions will depend largely on policymakers.

Those are the conclusions of a new paper from the Lawrence Berkeley National Laboratory, Tracking the Sun VI [PDF].

The analysis covers more than 200,000 residential, commercial, and utility-scale PV systems in 29 states, representing 72 percent of all grid-connected PV capacity in the United States as of 2012, and tracks installed prices before any incentives or tax credits, in 2012 dollars, from 1998 through 2012, with some preliminary 2013 data.

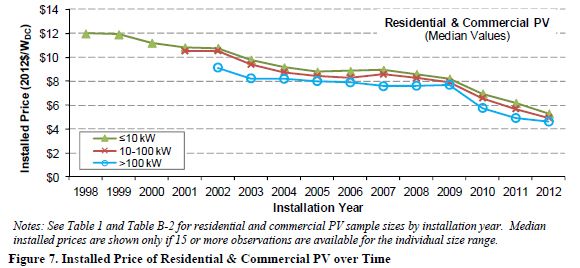

In 2012, the median installed price was $5.30/watt for residential (under 10 kilowatts) systems, $4.90/watt for larger (10 to 100 kilowatts) residential and commercial systems, $4.60/watt for commercial systems over 100 kilowatts, and $2.50 to $4.00/watt for utility-scale systems (over 2,000 kilowatts).

The authors carefully distinguish between various system-size categories throughout the paper, but for simplicity I will refer to systems under 10 kilowatts as residential, 10 to 2,000 kilowatts as commercial, and over 2,000 kilowatts as utility scale.

Prices in 2012 fell 6 percent to 14 percent (depending on the size) from the prior year. “This marks the third year in a row of significant price reductions for PV systems in the U.S.,” explained Galen Barbose of Berkeley Lab’s Environmental Energy Technologies Division, one of the report’s co-authors. Prices in California fell another 10 percent to 15 percent over the first half of 2013, suggesting that prices in 2013 will fall at least as much as they have in recent years.

Prior to 2005, installed prices fell mainly due to non-module cost reductions. Then those cost reductions stalled, as supply struggled to keep up with demand. But starting in 2008, supply exploded as new manufacturing capacity was built. From 2008 to 2012, 80 percent of the decline in total system cost was a result of falling module prices. The costs of non-module hardware also declined slightly, including "soft costs" like marketing, customer acquisition, design, installation, permitting and inspection. But they did not fall as rapidly as module costs.

Whereas module prices declined as a result of global market factors -- particularly the rapid build-up of supply in China, and strong feed-in tariff (FIT) incentives ensuring demand in Europe -- reducing soft costs will require public policy changes aimed at removing market barriers and accelerating deployment. “There simply are limits to how much further module prices can fall, and so it stands to reason that continued reductions in PV system prices will need to come primarily from the soft-cost side,” Barbose observed.

Soft costs are the main reason why small residential PV systems installed in 2012 cost far less in Germany, Italy and Australia than they did in the United States. Excluding sales or VAT taxes, Germany's median installed system price ($2.60/watt) was half the U.S. price ($5.20/watt). At $5.90/watt, Japan was the only major market with a higher cost than the U.S. Unsurprisingly, residential system size has increased as prices fell. The median system size in 1998 was 2.4 kilowatts; by 2012 it had grown to 5.2 kilowatts.

The cost difference is even more pronounced with larger systems. Utility-scale systems in Germany were quoted at $1.90/watt in 2012, while they were installed for $4.50/watt in the U.S.

Prices can vary substantially from state to state, depending on factors like market size, competition, labor costs, sales tax exemptions for PV, and administrative and regulatory compliance. The median installed price for small (10 kilowatts or less) systems is lowest in Texas, at $3.90/watt, and highest in Wisconsin, at $5.90/watt. Commercial (10 to 100 kilowatts) systems ranged from $3.70/watt in Colorado to $5.90/watt in Wisconsin. And utility-scale systems ranged from $3.20/watt in Colorado to $6.10/watt in Arizona.

Prices in California, the solar leader in the U.S. with 2,902 megawatts of capacity, were the fourth highest for residential systems, the third highest for commercial systems, and the second highest for utility-scale systems.

Variability in prices from state to state owes partially to some of the same soft-cost issues mentioned above, but other factors also play a role. Prices can be lower in larger and more mature markets, due to more competition, efficiency, bulk purchasing, and availability of lower-cost products. In states where grid power prices and incentives are high, installers can charge a higher price for a system based on its value, rather than on their direct costs.

Variables such as system size, a preference for higher-cost tracking systems over fixed-tilt systems, and the type of customer also play a role. For example, the authors note that about half the non-residential systems installed in California in 2012 were at tax-exempt facilities, which typically cost more due to a variety of factors, including labor wage requirements, domestic manufacture requirements, greater module shading, more parking structure installations, additional permitting requirements, and more complex procurement processes.

Sales taxes, which range from zero in Oregon and New Hampshire to more than 9 percent in California, can account for as much as a $0.40/watt difference in installed prices across states.

Surprising findings

The study found some unsurprising results (for example, tracking systems cost more than fixed-tilt systems), but uncovered a few interesting observations as well:

- Systems owned by non-integrated third-party providers (companies that provide system financing but buy the system from licensed contractors) cost roughly the same as systems obtained via cash sales, except in the small residential market, where third-party systems cost about $0.10/watt less than customer-owned systems. Systems supplied by integrated third-party providers (which supply both financing and installation) could only be priced on an appraisal basis, and were excluded from the study.

- Microinverters added about $0.40/watt to the cost of a residential system, but reduced the cost of a commercial system by about $0.20/watt.

- Because they are more expensive, more efficient modules generally amount to higher overall system prices, despite the reduced need for additional hardware and installation. Systems using modules of 14 percent efficiency or less were cheaper than systems using modules of 18 percent efficiency or better in both the residential and small commercial categories.

- The installed price of Chinese vs. non-Chinese modules was roughly the same for any given module efficiency. Somewhat surprisingly, residential systems using average efficiency (14 percent to 16 percent) modules of non-Chinese manufacture were slightly ($0.10/watt) cheaper in 2012.

- Residential systems are cheaper when installed during new construction than when installed as retrofits. Building-integrated systems (BIPV) are more expensive in new residential construction systems than rack-mounted systems.

- Small (under 1,000 kilowatts) ground-mounted systems are more expensive than similarly sized roof-mounted systems. For systems of 10 kilowatts or fewer, the price differential was significant: $0.70/watt.

Rapid growth

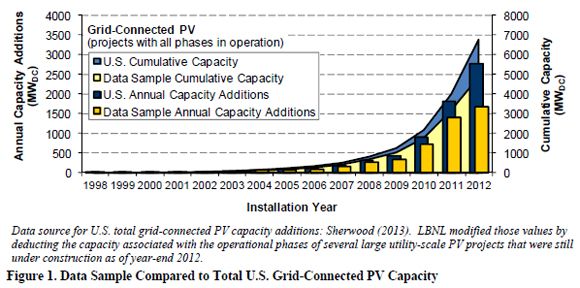

This report focused on price, not the rate of growth in installations. But it did include this chart, showing that U.S. grid-connected PV is now on the steep up-slope of the "S" curve, even if a certain analyst on Bill Gates' reading list won't acknowledge it.

That growth rate is happening globally, as Stephen Lacey pointed out earlier this week. In the last 2 1/2 years, the world added as much solar capacity (50 gigawatts) as it did the previous four decades. In the next 2 1/2 years, capacity will double again.

What policymakers need to do

Still, the authors conclude that maintaining the growth of the U.S. PV industry depends on continuing cost reductions, and that depends on significantly reducing soft costs.

How can we do that? Another LBNL report [PDF] issued earlier this year found that soft costs for residential PV in Germany are just 19 percent of those in the U.S., and tried to explain why that is.

First, it costs about one-tenth as much to acquire a customer in Germany. That's primarily because Germany has a national FIT, and the U.S. doesn't. I've said it before and I'll say it again: America needs a national FIT.

Second, costs for permitting, interconnection and inspection in Germany are also nearly one-tenth of those in the U.S. Part of that is because it takes much less time: about 5.2 hours per system in Germany, versus 22.6 hours in the U.S. Based on my experience as a system designer and salesperson in California, I know why that is. It takes an extraordinary amount of labor to create extremely burdensome, redundant, and oftentimes totally unnecessary permit packages to satisfy the requirements of building and planning authorities, which are different in every little town and county.

The best way to reduce those costs is to standardize building and planning requirements for PV systems nationwide, and make it as easy and as cheap as possible to pull a permit. Local authorities should follow the example of Lancaster, California, where mayor Rex Parris directed city staff to clear away obstacles in the building and planning approval process to encourage the growth of PV. Contractors can now pull a simple permit for a residential solar system in Lancaster in fifteen minutes, over the counter, for just $61.

Third, it's vital to cut the cost of installation labor. It takes almost twice as long to install a system in the U.S. as it does in Germany, partly because German installers rarely use the roof-penetrating mounting systems that are usually required in U.S. building codes. U.S. wiring practices should also be harmonized and standardized to reduce the amount of time installers have to spend trying to satisfy nitpicky and unnecessary requirements in certain jurisdictions (I've got some horror stories about that, but I won't bore you with them now).

Fourth, we should exempt solar PV systems from state sales taxes. Those taxes accounted for a median $0.21/watt in the U.S. in 2011, whereas in Germany, residential solar systems are exempt from revenue, sales, or value-added taxes.

Finally, U.S. markets could be more open to competition in installation labor. Too many customers (particularly tax-exempt entities) are subject to restrictions requiring them to use union labor, or to allow only electrical contractors with certain licenses to install solar systems. Liberalizing installation rules could cut prices further.

The U.S. solar industry needs policymakers, regulators, code jockeys (electrical, building, and planning), and elected officials to step up and keep its growth momentum going. Wisconsin and Arizona need to take a long look in the mirror and ask themselves why they can't do what Texas and Colorado can. Federal officials need to start asking how they can implement a national FIT, instead of protesting why they can't.

***

Chris Nelder is an energy analyst and consultant who has written about energy and investing for more than a decade. He is the author of two books (Profit From the Peak and Investing in Renewable Energy) and hundreds of articles, and has been published by Scientific American, Slate, the Harvard Business Review blog, Financial Times' Alphaville, Quartz, the Economist Intelligence Unit, and many other publications.

41

41

15

15

9

9