Behind-the-meter batteries are going to become a much larger part of the energy storage landscape over the next five years -- and that means that this infant industry will be doing a lot of growing up in that time.

So says GTM Research’s latest report, The Behind-the-Meter Energy Storage Landscape 2016-2021, which lays out the factors that will contribute to a gigawatt-scale market for batteries in buildings by decade's end. This growth will bring opportunity for companies in the field, ranging from startups to industrial giants, all serving different portions of the behind-the-meter value chain.

In particular, we’ve seen a rapid expansion of interest in batteries for commercial and industrial buildings for demand-charge management and grid services, a use case that’s expected to become cost-competitive in a growing number of U.S. states over the course of the decade.

But this growing field will also reveal which combinations of financing models, go-to-market approaches, and vertical and horizontal integration strategies are viable and which aren’t, according to GTM Research energy storage analyst and report author Brett Simon. This will become increasingly apparent as the incentives and subsidies that have helped boost deployments in a few key states give way to market-based forces.

This pressure will certainly apply to different models for behind-the-meter battery system financing, which has been critical in lowering the up-front cost of behind-the-meter battery systems for C&I customers. Through the first three quarter of 2016, the United States has seen a boom in project finance with $645 million raised for the sector, according to GTM Research.

“Energy storage financing, which still lacks standardized formats, particularly for the residential segment, is expected to undergo an evolution as the technology becomes better understood and financiers gain greater comfort,” Simon noted. "In particular, financiers are still hesitant to back residential projects, given a lack of monetizable value streams, along with higher customer acquisition and system costs compared to the non-residential segment."

To date, three different financing models have dominated the market -- shared savings, leases, and models based on the power-purchase agreements (PPAs) common to solar projects. Shared savings, used by startups such as Green Charge and Demand Energy, offer the advantage of reducing customers’ commitment to fixed payments, compared to leasing arrangements from companies like Stem and Advanced Microgrid Solutions. But they also lack the clear and predictable customer pricing and revenue streams for financing partners that lease models provide.

The PPA-esque model, which generally combines solar with storage, “offers customers familiarity, as PPAs have seen success in the solar PV market,” Simon noted. “However, solar-plus-storage PPAs are still relatively new and require the proper structure in order to offer a clear value proposition.”

The coming years will also shine light on which of several go-to-market strategies best suit an expanding market, Simon noted. Out of the 40 companies covered in the report, “each is exploring a different business model and varying suites of product and service offerings."

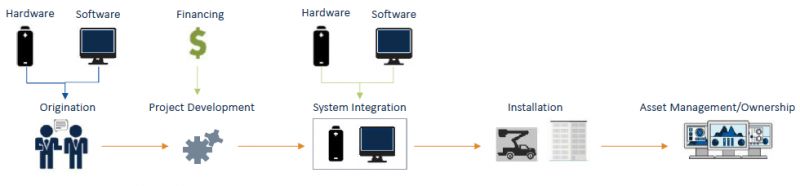

Early entrants like Stem and Green Charge have adopted a direct-to-end-customer strategy, managing everything from customer origination and project development to system integration and asset management. Meanwhile, companies like Enphase, Sunverge and Tabuchi Electric have worked largely through solar distributors and installers, while companies like Schneider Electric, ABB, NEC and S&C Electric are bringing integrated battery systems to market through various channels.

But these demarcations can be expected to shift in coming years, Simon noted. This will include companies looking for vertical integration opportunities by integrating systems and services or moving into project development roles, as well as horizontal moves by solar developers or energy management service providers into the storage space.

41

41

15

15

9

9