Biobutanol producer Gevo just filed its S-1 registration statement with the SEC for its IPO. The company is looking to raise up to $150 million led by underwriters UBS Investment Bank, Goldman Sachs, and Piper Jaffray. Here's a link to the S-1.

Gevo has raised more than $40 million in funding from Burrill & Co., Malaysian Life Sciences Capital Fund, Khosla Ventures, Lanxess and Virgin Green Fund. Khosla Ventures is the leading share holder at more than 40 percent.

Gevo had a mere $660,000 in revenue in 2010 -- hardly IPO material. Until this month that is, when Gevo acquired 18-million-gallon-per-year ethanol producer Agri-Energy. With that acquisition, Gevo suddenly has $40.7 million in revenue, with losses of $18.2 million.

Gevo is working on a fermentation process to produce isobutanol from the fermentable sugars in cellulosic biomass. Isobutanol is a building block for making biodiesel, jet fuel and other materials. The S-1 estimates the global market for isobutanol as more than a trillion gallons per year.

We'll bring you more info in the coming days, but for now, here are some highlights from the S-1:

Highlights from the S-1

Gevo is "a renewable chemicals and advanced biofuels company. Our strategy is to commercialize biobased alternatives to petroleum-based products using a combination of synthetic biology and chemical technology. In order to implement this strategy, we are taking a building block approach. We intend to produce and sell isobutanol, a four carbon alcohol. Isobutanol can be sold directly for use as a specialty chemical or a value-added fuel blendstock. It can also be converted into butenes using simple dehydration chemistry deployed in the refining and petrochemicals industries today. Butenes are primary hydrocarbon feedstocks that can be employed to create substitutes for the fossil fuels used in the production of plastics, fibers, rubber, other polymers and hydrocarbon fuels. Customer interest in our isobutanol is primarily driven by its potential to serve as a building block to produce alternative sources of raw materials for their products at competitive prices. We believe products made from biobased isobutanol will be subject to less cost volatility than the petroleum-derived products in use today. We believe that the products derived from isobutanol have potential applications in approximately 40% of the global petrochemicals market, representing a potential market for isobutanol of approximately 67 BGPY, based upon volume data from SRI, CMAI and Nexant, and substantially all of the global hydrocarbon fuels market, representing a potential market for isobutanol of approximately 900 BGPY, based upon volume data from IEA. When combined with a potential specialty chemical market for isobutanol of approximately 1.1 BGPY, based upon volume data from SRI, and a potential fuel blendstock market for isobutanol of approximately 40 BGPY, based upon data from the IEA, the potential global market for isobutanol is approximately 1,008 BGPY.

We also believe that the raw materials produced from our isobutanol will be drop-in products, which means that customers will be able to replace petroleum-derived raw materials with isobutanol-derived raw materials without modification to their equipment or production processes. In addition, the final products produced from our isobutanol-based raw materials will be chemically identical to those produced from petroleum-based raw materials, except that they will contain carbon from renewable sources. We believe that at every step of the value chain, renewable products that are chemically identical to incumbent petrochemical products will have lower market adoption hurdles, as the infrastructure and applications already exist.

Strategy

Our strategy is to commercialize our isobutanol for use directly as a specialty chemical and value-added fuel blendstock and for conversion, into plastics, fibers, rubber, other polymers and hydrocarbon fuels. We intend to drive further adoption of our isobutanol in multiple US and international chemicals and fuels end-markets by offering a renewable product with superior properties at a competitive price. In addition, we intend to leverage existing and potential strategic partnerships with hydrocarbon companies to accelerate the use of isobutanol as a building block for drop-in hydrocarbons. This strategy will be implemented through direct supply agreements with leading chemicals and fuels companies, as well as through alliances with key technology providers.

Markets

Relative to petroleum-based products, we expect that chemicals and fuels made from our isobutanol will provide our potential customers with the advantages of lower cost volatility and increased supply options for their raw materials. Our isobutanol, and the products produced from it will also offer our potential customers the additional benefit of being able to market their products as environmentally sensitive.

Our initial commercialization efforts are focused on the following markets:

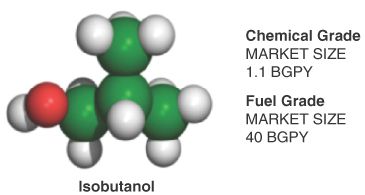

Isobutanol. Without any modification, isobutanol has applications as a specialty chemical and a fuel blendstock. In the fuel blendstock market, isobutanol can be used to replace high value blendstocks such as alkylate and can be blended in conjunction with, or as a substitute for, ethanol and other widely-used fuel oxygenates. Our estimate of the global market for isobutanol as a gasoline oxygenate is approximately 40 BGPY, based upon data from the IEA. While isobutanol can be used as a replacement for ethanol, its product properties are significantly differentiated from ethanol. As a gasoline blendstock, isobutanol’s low vapor pressure, high energy content and low water solubility versus ethanol make it a valuable product that can be sold directly to refiners and is expected to be compatible with existing engine and industry infrastructure, including pipeline assets. Isobutanol can also be sold for immediate use as a solvent. This global market for butanol represents approximately 1.1 BGPY, based upon volume data from SRI. Combined, the total global market for isobutanol as a fuel blendstock and specialty chemical represents approximately 41.1 BGPY.

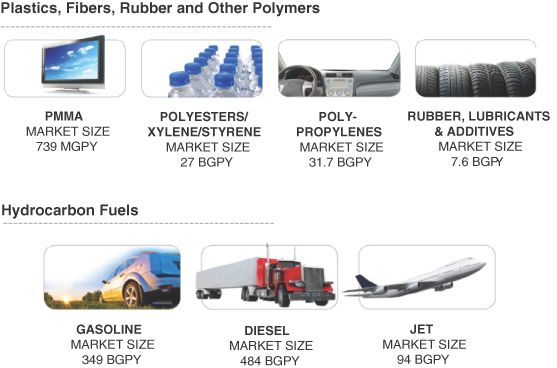

Plastics, Fibers, Rubber and Other Polymers. Isobutanol can be converted by our potential customers into a wide variety of hydrocarbons, which form the basis for the production of many products, including: rubber, lubricants, additives, methyl methacrylate, polypropylenes, polyesters and polystyrene, representing an aggregate potential market for isobutanol of approximately 67 BGPY, based upon volume data from SRI, CMAI and Nexant.

Hydrocarbon Fuels. The hydrocarbons that can be produced from isobutanol can be used to manufacture specialty gasoline blendstocks, jet and diesel fuel, as well as other hydrocarbon fuels. The hydrocarbon fuels that can be produced from isobutanol collectively represent a potential market for isobutanol of over 900 BGPY, based upon volume data from IEA.

Partners include Lanxess, Total, Toray Industries, United Air Lines and CDTECH.

Competitive strengths

The Gevo Integrated Fermentation Technology (GIFT) demonstrated at commercially relevant scale. “We have completed the retrofit of a 1 MGPY ethanol facility and successfully produced isobutanol at this facility using our first-generation biocatalyst, achieving our commercial targets for concentration, yield and productivity…Also, we believe that our entry into the acquisition agreement with Agri-Energy demonstrates the readiness of our technology for commercial deployment and supports our plan to commence initial commercial-scale isobutanol production in the first half of 2012.”

Competitors

Significant competitors in these areas include Codexis, Inc., which is engaged with Equilon Enterprises LLC dba Shell Oil Products US, or Shell, in a research and development collaboration under which they are developing biocatalysts for use in producing advanced biofuels; Novozymes A/S, which has partnered with a number of companies and organizations on a regional basis to develop or produce biofuels, and recently opened a biofuel demonstration plant with Inbicon A/S of Denmark; Danisco A/S/Genencor, which has formed a joint venture with E.I. Du Pont De Nemours and Company, or DuPont, called DuPont Danisco Cellulosic Ethanol LLC, and is marketing a line of cellulases to convert biomass into sugar; Royal DSM N.V., which received a grant from the US Department of Energy to be the lead partner in a technical consortium including Abengoa Bioenergy New Technologies, Inc., and is developing cost-effective enzyme technologies; Mascoma Corporation, which has entered into a feedstock processing and lignin supply agreement with Chevron Technology Ventures, a division of Chevron USA., Inc.; and BP, p.l.c., or BP, which has purchased Vercipia Biofuels, LLC and technology from Verenium Corporation to develop a commercial-scale cellulosic ethanol facility. Range Fuels, Inc. is also focused on developing non-biocatalytic thermochemical processes to convert cellulosic biomass into fuels, and Coskata, Inc. is developing a hybrid thermochemical-biocatalytic process to produce ethanol from a variety of feedstocks.

In the production of cellulosic biofuels, key competitors include Shell Oil, BP, DuPont-Danisco Cellulosic Ethanol LLC, Abengoa Bioenergy, S.A., POET, LLC, ICM, Mascoma, Range Fuels, Inbicon A/S, INEOS New Planet BioEnergy LLC, Coskata, Archer Daniels Midland Company, BlueFire Ethanol, Inc., KL Energy Corporation, ZeaChem Inc., Iogen Corporation, Qteros, Inc., AE Biofuels, Inc. and many smaller start-up companies. If these companies are successful in establishing low cost cellulosic ethanol or other fuel production, it could negatively impact the market for our isobutanol as a gasoline blendstock.

Additionally, DuPont has announced plans to develop and market isobutanol through Butamax Advanced Biofuels LLC, or Butamax, a joint venture with BP. A number of companies including Cathay Industrial Biotech, Ltd., Green Biologics Ltd., METabolic Explorer, S.A., TetraVitae Bioscience, Inc. and Cobalt Technologies, Inc. are developing n-butanol production capability from a variety of renewable feedstocks. Academic and government institutions may also develop technologies which will compete with us in the blendstock market.

***

More analysis in the days to come as we peruse the S-1. Stay tuned.

42

42

15

15

9

9