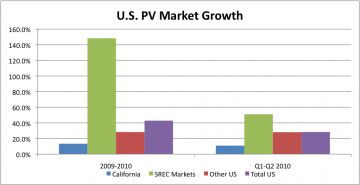

California may be the America’s reigning Little Germany for PV installations, but states with Solar Renewable Energy Credit (SREC) markets may be where new solar dreams are made. Results from the inaugural SEIA/GTM Research U.S. Solar Market Insight™ (recently launched at Solar Power International) show that the seven states with SREC markets have installed a combined 110 MWdc in the first half of 2010. If second-half installations continue at a similar pace, year-on-year growth will be over 148% in these states, dwarfing a 28% year-on-year growth for the overall U.S. market’s pace. In actuality, growth rates for all markets will be higher, as SEIA/GTM Research forecasts close to 870 MW due to uniformly strong second-half surges.

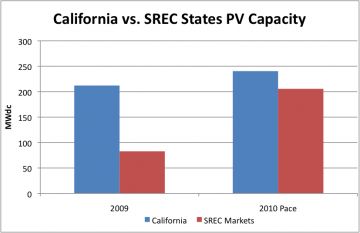

New Jersey clearly leads SREC states with a phenomenal 59 MWdc installed in the first half of 2010 -- already surpassing last year’s total installed capacity. However, the remaining SREC states of Delaware, Maryland, Massachusetts, North Carolina, Ohio and Pennsylvania are also rocketing off with over 51 MW installed in the same period. As covered in the October issue of PV News, Pennsylvania installations this year have surpassed a stellar 14 MW, despite the lack of any new utility solar projects, in the first half of 2010 from just 3.9 MW in 2009.

SRECs are specialized tradable renewable/alternative energy credits (measured in MWh) created by generation portfolio standards that require a certain percentage of the utilities' electricity to be generated from solar. Due to this PV “carve-out,” SRECs have a built-in premium in comparison to RECs from other sources. The price of SRECs is determined by the supply of solar generation and the demand to meet state RPS requirements, with a price ceiling created by the Solar Alternative Compliance Payment (SACP) -- the penalty that electricity suppliers must pay if they fail to acquire the requisite SRECs.

Meanwhile, U.S. Solar Market Insight™ (in agreement with others) shows that California’s PV market may be slowing; it is only on pace for a disappointing 13.5% year-on-year growth from last year’s 212 MW. While second-half installations should pick up, California’s decelerating market significantly contrasts with the rest of the U.S. state markets, inciting some hope that North America will no longer be referred to as "California, Ontario, and everyone else. "

This news comes as European FIT programs continue to announce cuts and U.S. states struggle to find funding for their rebate programs. Florida’s legislature has been unwilling to allocate $13.9 million in unspent ARRA stimulus funds to the Florida Energy and Climate Commission, which is currently facing a $52 million backlog in its solar rebate program. States like Colorado, Connecticut and New York have also had to boost their rebate programs with ARRA funding in previous years.

Of course, not everything is rosy in state SREC markets. Maryland’s commercial market is “struggling” because utilities are failing to commit to long-term SREC contracts. While spot market prices have hovered around a respectable price of $325, project financing for larger projects has been difficult to secure without any long-term incentive visibility. Furthermore, every SREC state still offers some form of up front cash rebate, though with tight limits that are typically restricted to residential and small non-residential systems. Nevertheless, U.S. Solar Market Insight™ asserts that more than 20% of installed capacity in Pennsylvania did not capture up-front rebates from the PA Sunshine program, indicating that SRECs have a strong potential to drive growth on their own. Continued growth in SREC markets will require either long-term visibility of SREC prices leading to or from long-term SREC contracts or a continued short supply of SRECs to prop up spot market prices.

41

41

15

15

9

9