Until recently, Mexico represented the most promising market for solar in Latin America. But the strong growth expected for the country is now much less certain.

In fact, solar installation figures in 2016 could be 36 percent smaller than projected last year. What happened?

As we've documented, solar developers and financiers are dealing with a completely new set of rules for selling solar electricity into Mexico's energy market. Those new rules are causing some confusion and, thus, slowing activity.

For the first time ever, the country actually has a competitive market to sell into. Over the last couple of years, the Mexican government has been working on a plan to overhaul the state-owned electricity provider and build a wholesale market to encourage competition. The new market launched this month, and auctions will take place over the coming months.

Almost everyone sees Mexico's transition to a competitive market as necessary to meet growing demand for power in the country. But as energy suppliers grapple with the brand new rules (some of which haven't been finalized, or are confusing), there are a lot of eager solar companies and investors sitting on the sidelines, trying to figure out how and when to bid into the market.

"It will take a long time to digest. We have to write all new history and not rely on what was written before," said Hector Olea, president and CEO of the project developer Gauss Energia, speaking about the market reforms at GTM's Solar Summit in Mexico this week.

That conference (which GTM Squared members can stream live) is happening just weeks after the reforms went into place. Everyone at the event has been trying to figure out where solar will fit into a largely unsubsidized competitive market that is still in its infancy.

Mohit Anand, a senior solar analyst at GTM Research, called the reforms "rapid and drastic change" for developers. "It will still be the same game, but under completely different rules."

No one knows exactly what's going to happen in Mexico. Installations will most certainly drop this year, but the competitive landscape could evolve to benefit PV in 2017 and beyond. Below is a compilation of GTM Research's best projections for what will happen in the country.

First, the downside. A lot of projects that were planned for 2016 -- most of them utility-scale -- have been delayed as developers figure out how the market will work. Falling residential and commercial electricity prices (which are still highly subsidized) are also impacting the economics of distributed solar. "There will be short-term pain," said Anand.

Source: GTM Research

Eventually, the competitive market will provide more opportunities for utility-scale solar, and the industry will get back on track. There will be more offtakers in the market that can buy solar. And a wider range of auctions, spot markets and capacity markets will be created. As solar costs continue to fall, the technology is better positioned to compete head-to-head with any resource in these markets.

Between 2016 and 2020, GTM Research expects 84 percent compound annual growth for solar in Mexico. "That short-term pain will make for long-term gain," said Anand.

Source: GTM Research

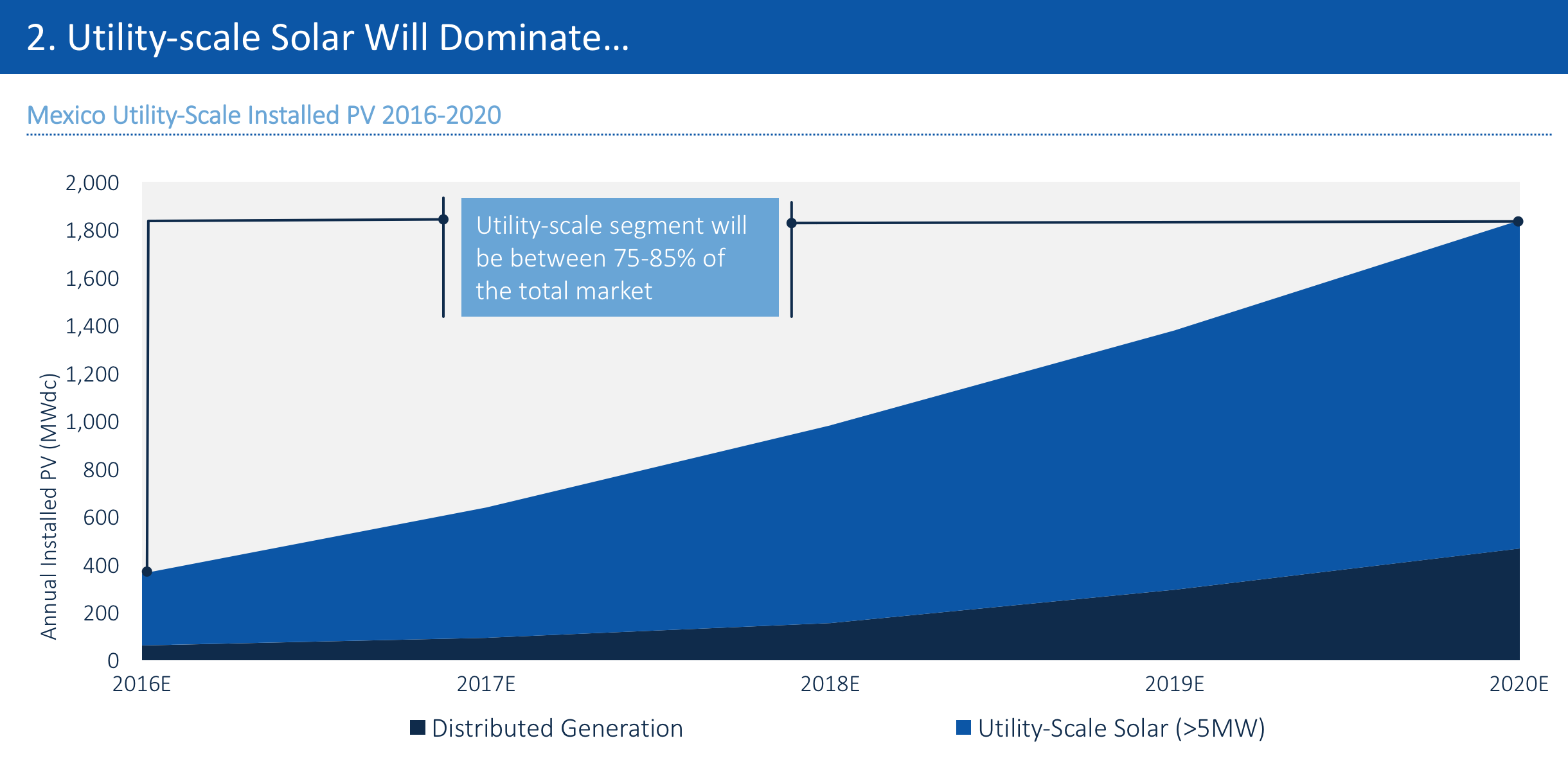

Utility-scale solar will be the biggest sector, by far. The reason: system costs are falling faster in that sector, and there will be far more opportunities to bid into the market.

"The offtaker landscape has become far more diverse. Developers need to find their niche in which they can be successful. You can now sell energy, capacity and clean energy certificates," said Anand.

Source: GTM Research

Distributed solar will see incremental growth through 2018, and then accelerate through 2020 as system pricing falls and new financing options get introduced. Residential will dominate the distributed solar market through 2018. But commercial solar will start to play a bigger role in the following years as developers sign contracts directly with corporate offtakers -- a market that could benefit from the new rules.

"Distributed generation continues to experiment with business models," said Anand.

Source: GTM Research

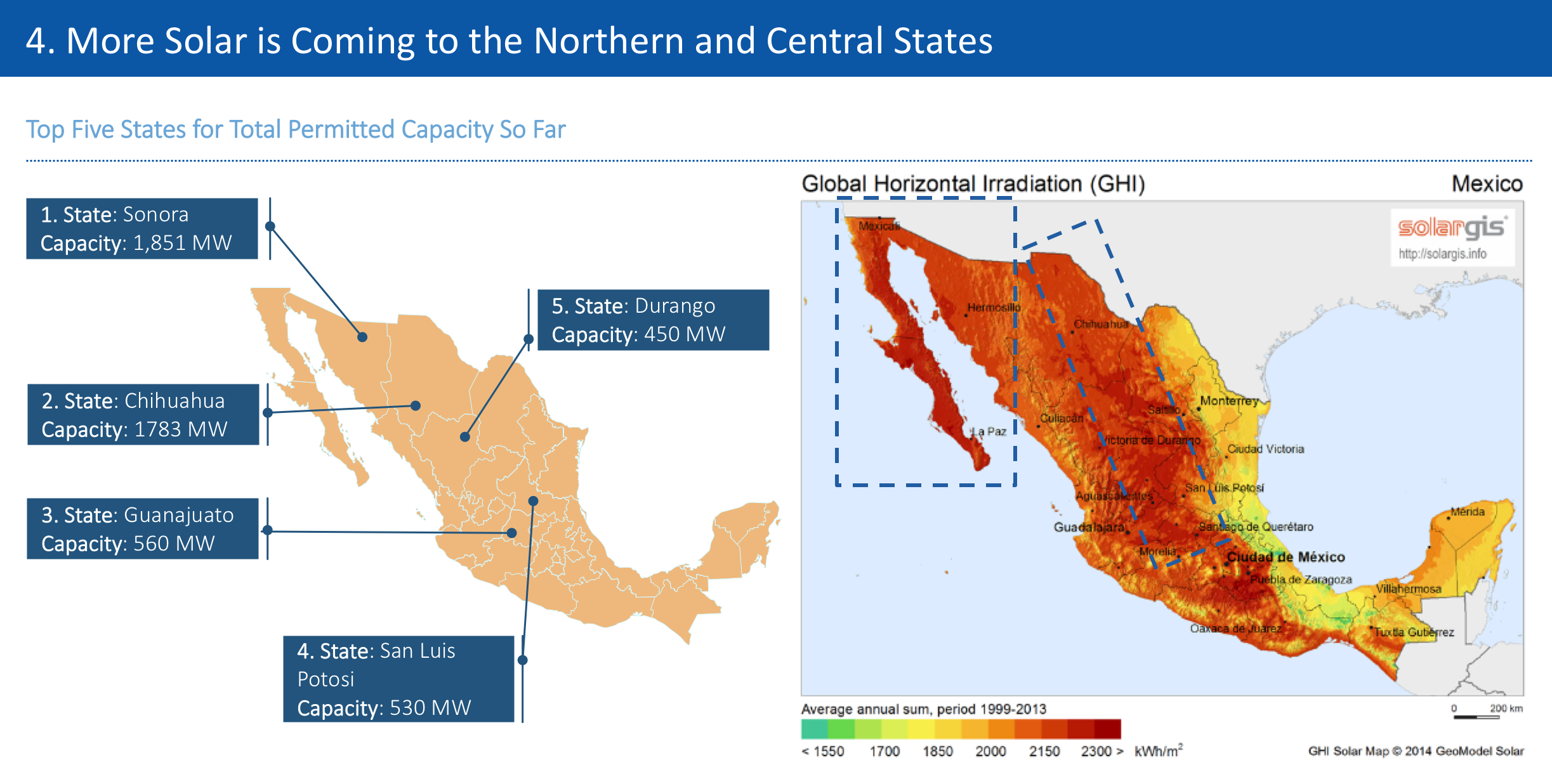

Forced to compete at very low prices, most of the expected utility-scale capacity will be built in locations with the best solar resources. So project development will largely be clustered in north and central Mexico.

Source: GTM Research and GeoModel Solar

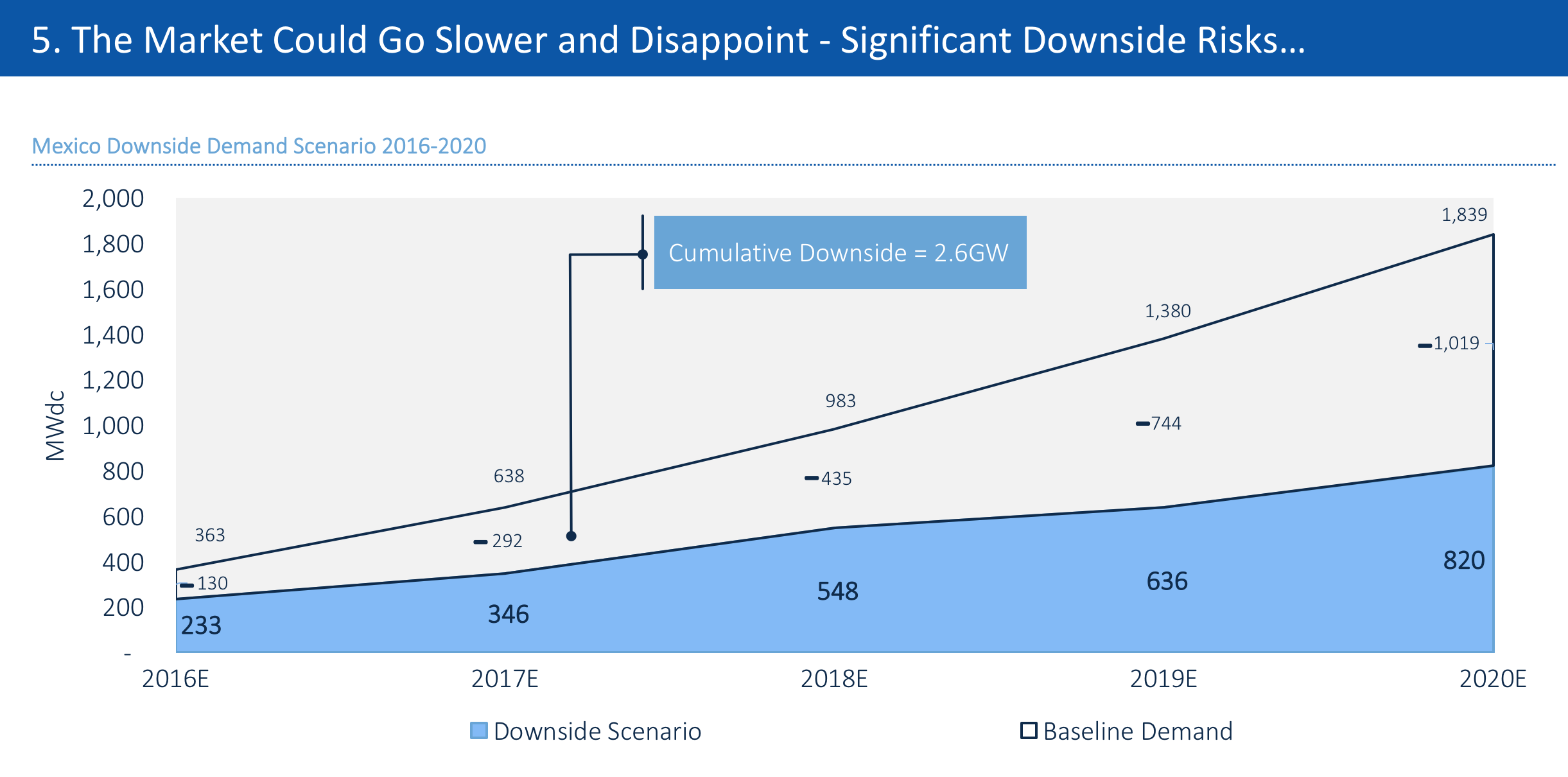

There are significant downsides to the Mexican market, however. What if banks are not comfortable with the rate of return for projects trying to compete at low prices in an unsubsidized market? What if development costs don't come down as expected? What if net metering isn't extended for residential projects? These are all scenarios that everyone is grappling with.

The end result could very well be a market dominated by cheap natural gas. Assuming solar is disadvantaged by the new market, development could be 2.6 gigawatts lower than expected by 2020.

Source: GTM Research

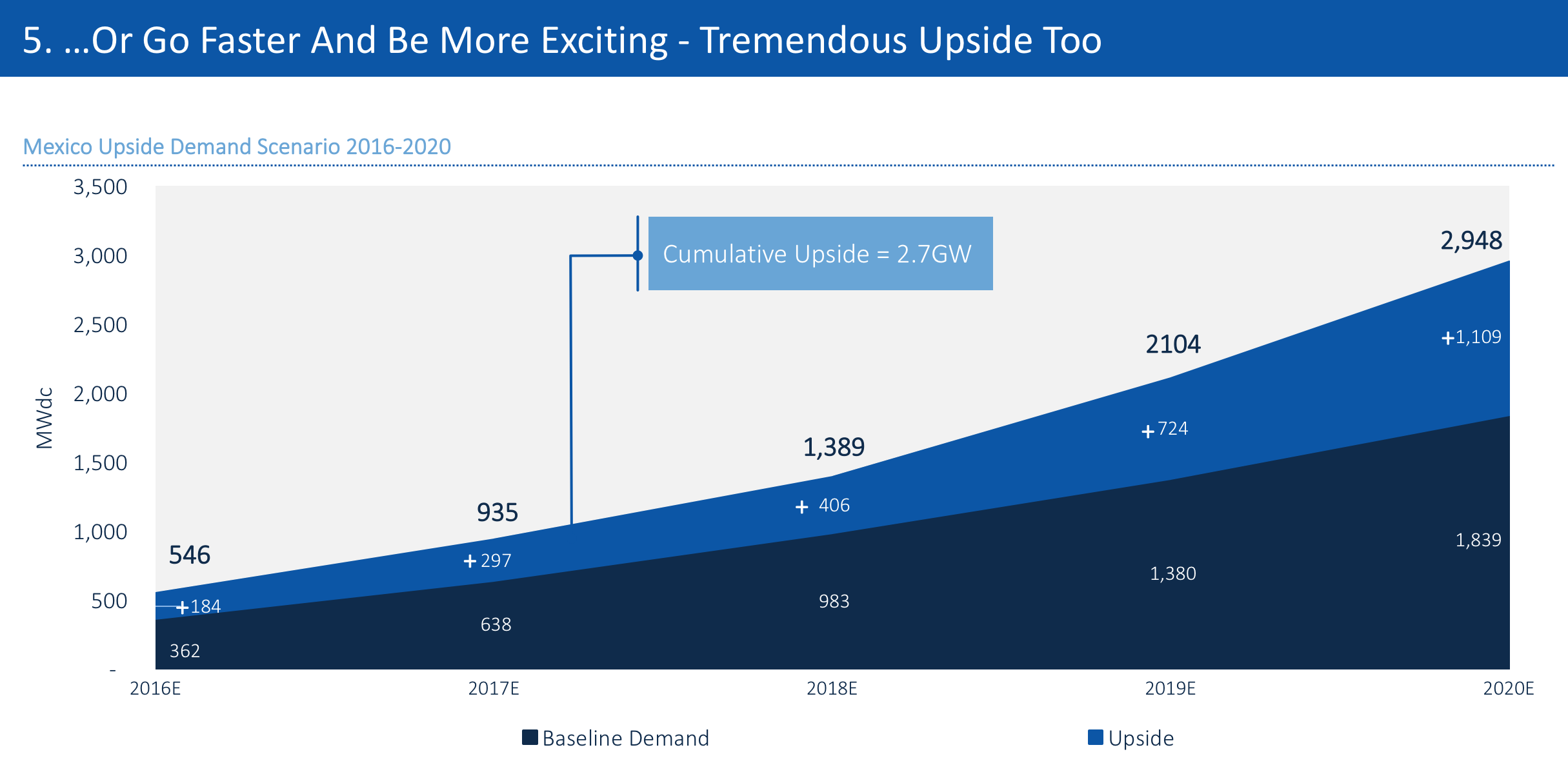

But the upside is significant. If development costs continue their downward trend, net metering remains in place, and bankers get more comfortable with supporting solar projects, "the market could be very exciting," said Anand.

The trouble is that it's still too early to say which scenario is more likely.

Howard Wenger, the president of SunPower's business units, put it succinctly: "We’re learning in real time."

So is everyone else. Keep your eyes on Mexico. It'll be one of the most dynamic markets to watch in the next few years.

Source: GTM Research

41

41

15

15

9

9