Despite a handful of gigawatt-scale players, the third-party asset manager landscape is very fragmented.

According to GTM Research and Solichamba's new report on the topic, the top 25 third-party asset managers account for 15.6 gigawatts of managed capacity. In comparison, the top 25 investors hold 26.9 gigawatts of net capacity (corresponding to 31.8 gigawatts of gross capacity).

This gap in scale reflects the fact that third-party asset managers usually serve clients with small to mid-size portfolios, while the largest investors usually self-perform this function. Only the top 11 service providers managed more than 500 megawatts of solar assets in operation at the end of 2016.

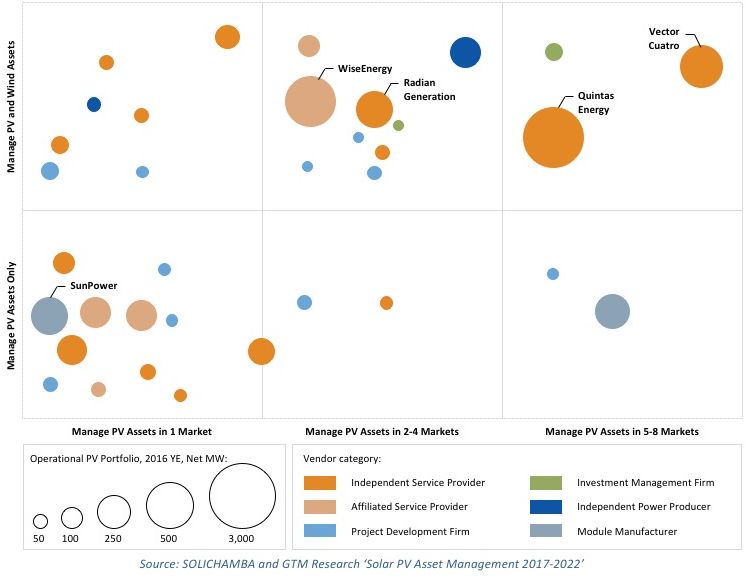

Below is a map of the competitive landscape where the horizontal axis measures each player’s level of internationalization (defined as the number of countries in which they currently manage PV assets), and the vertical axis indicates whether they manage wind plants in addition to solar. The area of the bubble representing a vendor is proportional to its managed portfolio at the end of 2016 (counting only operational solar PV assets).

Currently there are only five gigawatt-scale third-party asset managers in the global landscape: Quintas Energy, Vector Cuatro, WiseEnergy, SunPower and Radian Generation. Outside of these players, the market is extremely fragmented.

Market forces point to imminent consolidation

In a market where the budget for asset management activities is set by large independent power producers (IPPs) benefiting from the scale of very large portfolios, the only way for third-party asset managers to remain price-competitive is to aggregate smaller portfolios -- and to do so faster than in the past.

The global PV market is diversifying geographically at a quick pace, so third-party asset managers will have to enter a variety of emerging markets (especially in Asia and Latin America) if they want to achieve long-term growth and limit dependency on any single market. Because many investors are diversifying their portfolios, third-party asset managers will also be asked to operate in multiple markets and provide a consistent and consolidated view of assets across a variety of countries.

As the overlap between the wind and solar investor landscape increases, the same investors may also want a consistent and consolidated view of assets across technologies. Asset management software providers are aware of this trend, and all 10 players analyzed in the new GTM Research report are either already supporting wind assets or planning to do so in 2017 to 2018.

For asset management service providers, this kind of expansion into new markets and new technologies (for those players not yet active in wind) demands a large amount of time and resources. The quickest path would be mergers and acquisitions.

GTM Research and Solichamba expect that several M&A transactions will occur in the next 12 months, allowing third-party asset management service providers to grow in scale, geography coverage and technology expertise.

***

For more information about asset management markets, service providers, and software, check out the new report, Solar PV Asset Management 2017-2022: Markets, Investors, Asset Managers and Software.

41

41

15

15

9

9