Between March 2012 and February 2013, seven U.S. geothermal projects came on-line.

U.S. installed geothermal capacity grew by 147.05 megawatts in 2012, a 5 percent growth rate.

According to the newest Geothermal Energy Association (GEA) Production and Development Report, “up to fourteen plants could become operational in 2013, [with] nine new plants in 2014 and ten more plants in 2015, by over 20 different companies and organizations -- making 2013, 2014, and 2015 three of the most significant boom years for geothermal in decades.”

Findings reported by GEA suggest this could be the beginning of extended new growth for the industry. “Geothermal companies in the US are also acquiring and developing early stage geothermal resources,” the report noted.

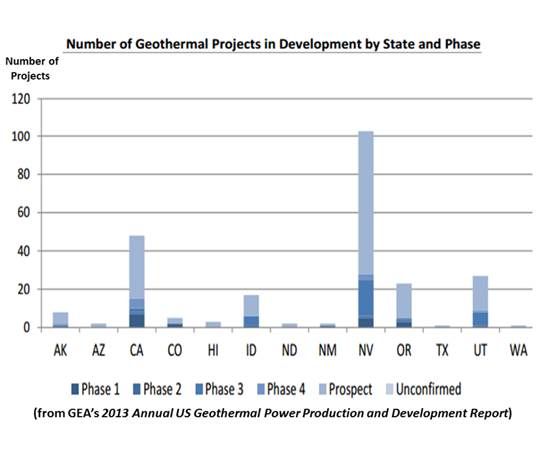

This year the industry is developing 175 geothermal projects and prospects in thirteen states. And of those 175 projects, according to the GEA, 148 (84 percent) are conventional hydrothermal resources in “unproduced” areas where plants have not been developed before.

An improving economy and the recent revision of the production tax credit (PTC) allowing it to be applied to projects that go into construction (instead of production) by the end of this year are two factors behind the growth, according to the report.

“The policies and technologies are there to move the industry forward,” GEA Executive Director Karl Gawell said. “The change to the PTC showed a general trend of support at the federal level for geothermal. Past that, growth depends on state policies.”

Geothermal projects are in various phases of development in thirteen states. “The majority of advanced-stage projects are currently located in Nevada and California,” the report said, but “utility-scale projects are also nearing completion and production in Oregon, Utah, Idaho, and Alaska.”

The reported new growth excluded detailed consideration of the potential for enhanced geothermal systems (EGS), a budding technology which made an important advance in 2012.

41

41

15

15

9

9