GTM Research forecasts that total smart grid expenditure for rural co-op utilities in the U.S. will reach $4.1 billion through 2017, accounting for approximately 10 percent of the country’s cumulative smart grid market over the next five years. GTM’s latest report, The Rural Smart Grid 2013: A Survey of Utility Deployment, Expenditure and Strategy, anticipates that rural utilities will continue to focus on advanced metering infrastructure (AMI), followed closely by distribution automation (DA) technologies.

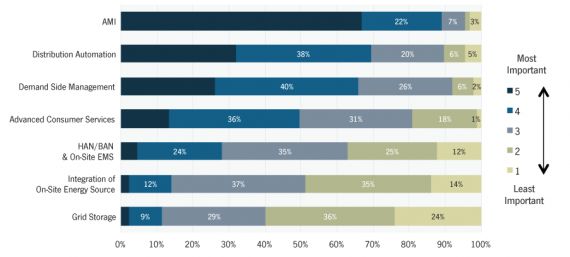

FIGURE: What Do You Consider to Be the Most Important Applications of a Smart Grid?

Source: The Rural Smart Grid 2013: A Survey of Utility Deployment, Expenditure and Strategy

Each year, GTM Research, in collaboration with the Rural Smart Grid Summit (RSGS), conducts a survey of key decision-makers from a diverse group of rural utilities in order to provide insight into this emerging market segment. This 41-question survey, which GTM Research publishes today in the form of a nearly 50-page report, provides unprecedented insight into the smart grid planning of executives and decision-makers at leading rural utilities across North America. With rural co-ops owning over 40 percent of the nation's distribution lines and their collective service territories covering approximately three-quarters of the nation's landmass, it has never been more important to understand this smart grid submarket.

FIGURE: Selected Large Rural Co-Ops’ AMI Deployments

Source: The Rural Smart Grid 2013: A Survey of Utility Deployment, Expenditure and Strategy

“As large expenditure decreases in the U.S., vendors will need to examine new utility demographic opportunities outside of the investor-owned sector,” said Zach Pollock, Analyst at GTM Research. “Despite being early adopters of technologies like advanced meter reading (AMR), cooperative utilities will spend the least amount of money on smart grid investment over the next five years when compared to municipal and investor-owned utilities. In addition, the pace of deployments will be much slower and more fragmented than the rapid deployments which we witnessed post-stimulus. The relatively small cooperative market will have a polarizing effect on the vendor landscape, and we expect vendors deeply entrenched in the co-op space to strengthen offerings, while new entrants will likely focus on recognizing high growth opportunities in new geographies."

GTM Research analyzed responses from nearly 100 top rural co-op utility executives in this report and identified the following smart grid applications as their primary areas of focus:

- Advanced metering infrastructure (AMI)

- Distribution automation (DA)

- Demand-side management

- Advanced consumer services

- HAN/BAN & on-site EMS

- Integration of on-site energy sources

- Grid storage

To learn more about The Rural Smart Grid 2013, visit www.greentechmedia.com/research/report/the-rural-smart-grid-2013.

41

41

15

15

9

9