U.S. utilities see both threat and opportunity in the rise of customer-owned solar systems. Sure, all that new distributed generation could help them avoid building new power plants in the future. But it could also threaten utility business models, unless they’re able to “flip the DG equation” to make it work for them.

These are some of the top-line findings of Black & Veatch’s Strategic Directions: U.S. Electric Industry report released Tuesday. In its eighth installment of its annual survey of more than 500 utility executives, the engineering and consulting firm took a close look at just how utilities are incorporating distributed generation (DG) into their future plans.

First, the good news. Black & Veatch found that 64 percent of respondents with an opinion on the matter cited natural gas and/or renewable generation, including distributed resources, as a likely replacement energy source for increasing demand or capacity lost to retiring coal or nuclear power plants. And in some cases, utilities can expect to build less central generation than what they’re losing, because distributed generation -- mostly rooftop solar -- is making up the difference.

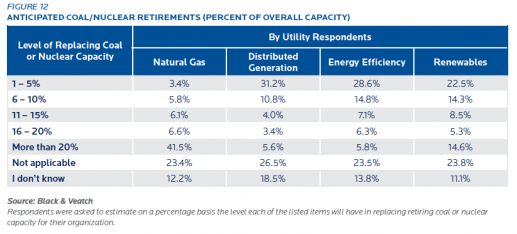

But that benefit won’t come evenly to all utilities. As the chart below indicates, utilities that must replace less than 20 percent of their current generation mix being lost to coal or nuclear plant retirements see renewables, DG and energy efficiency as their first choice. But those at replacement levels greater than 20 percent favor natural gas.

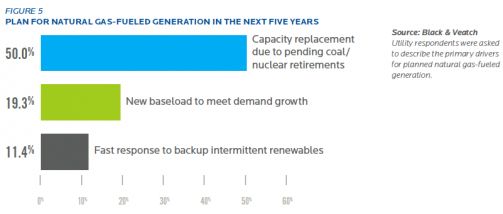

At the same time, a significant minority of utilities that are planning new natural gas-fired power plants said they were doing so to back up intermittent renewables like solar and wind, as the chart below indicates.

This highlights the fact that for many utilities, “the anticipated adoption of distributed generation and renewables does not come without costs,” the report stated. Electric utilities have to keep serving all their customers, even those that may be paying little or nothing in monthly utility bills because of their rooftop solar. At the same time, distributed generation brings “additional complexity to the system” that utilities will need to manage, at an uncertain cost, as they integrate it into their long-range plans.

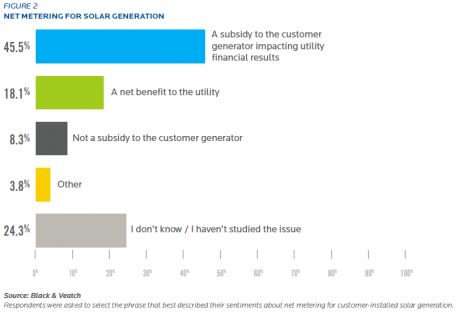

These adaptations to a DG-rich grid aren’t coming without their share of conflict, of course. In particular, when asked whether net energy metering (NEM) represents a subsidy from utilities to customers, a plurality (45 percent) responded yes, while 18 percent called it a net benefit to the utility, and 8 percent were neutral on the subject.

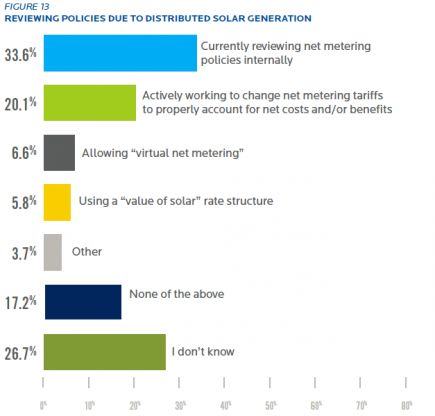

This point is hotly argued between utilities and solar advocates, and examples of net metering as a customer subsidy exist alongside examples where that’s not the case. Still, a majority of respondents said that their utility was either reviewing their net metering policies or actively working to change them, as is happening in states from California and Arizona to Massachusetts and Minnesota.

“It’s the end users, the customers who are driving distributed energy right now, not utilities,” Ryan Pletka, associate vice president of renewable energy at Black & Veatch and one of the report’s contributors, said in an interview. “We think there are lots of things utilities could be doing to be more proactive.”

For instance, utilities can own and control solar PV inverters as a distribution grid asset, offer community solar programs to customers who live in apartments or homes that aren’t well suited for rooftop solar, or create on-bill financing for customer DG, he said.

Utilities can also strive to incentivize solar installations in areas where it will reduce line losses, help defer infrastructure upgrades, and otherwise serve as a benefit to the utility, he noted. While the regulatory structures to allow these kinds of “locational” incentives don’t yet exist, California regulators have begun a process to create them, and the state’s big three investor-owned utilities will be required to create plans that incorporate these factors into their distribution grid plans.

“The analytic capabilities to be able to ascertain where those hot spots are, as it were, are only now coming to the fore,” he said. But as they emerge, it will be possible to identify “where DG makes the most sense for the customers and where DG makes the most sense for the utilities -- and that overlap is where DG makes the most sense for both.”

That’s the process that Black & Veatch has dubbed “flipping the DG equation,” and while it hasn’t actually happened yet, the company is working with utility clients to start analyzing the potential for identifying the spots where DG best supports their economic and technical needs, and creating restructured customer rates or incentives to encourage DG adoption at those locations.

“Even if utilities aren’t trying to own distributed generation assets and control them,” as utility Arizona Public Service is proposing to do, “they need to have a better understanding of the market,” he said. “At the very least, they need to understand where their customers are more likely to adopt DG.”

41

41

15

15

9

9