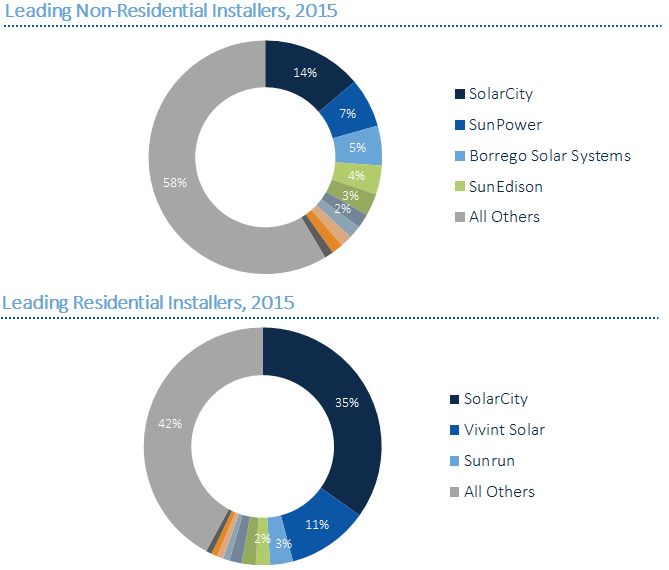

According to GTM Research’s latest report, U.S. Commercial Solar Landscape 2016-2020, the top 10 developers account for just 42 percent of the U.S. commercial solar market. This contrasts with the much more consolidated residential market, where the top three companies installed nearly half of the segment’s total in 2015.

“The fragmented commercial developer landscape is largely the result of bottlenecks in the customer origination process that make it difficult for any individual player to consistently grow,” according to Senior Solar Analyst and report author Nicole Litvak. “There are therefore no dominant players driving the overall market growth, as SolarCity does in residential.”

Source: U.S. Commercial Solar Landscape 2016-2020

This isn’t to say that there aren’t large players in the market. The report highlights 13 of the leading national commercial solar developers and identifies a number of common criteria for their success. These include an emphasis on originating large deals for Fortune 500 customers, a captive source of low-cost capital, and the ability to offer ancillary products and services such as energy storage.

The report notes that regional players are generally more successful than national developers in originating local customers due to their knowledge of the local markets and regulations. However, those systems are often more difficult to finance.

“The commercial market has struggled to efficiently match individual projects with financing,” added Litvak. “Furthermore, there is almost a complete lack of tax equity financing available for systems with non-creditworthy customers.”

FIGURE: Selected Regional Developers

Source: U.S. Commercial Solar Landscape 2016-2020

Though the commercial segment has been stagnant since 2012, GTM Research anticipates a rebound over the next five years. This growth will be driven by the extension of the federal Investment Tax Credit, the growing adoption of solar among national corporations, the increasing availability of financing for small commercial systems, and an expanding market for community solar.

The report forecasts the segment to grow 30 percent this year, with over 1.3 gigawatts installed. By 2020, the U.S. non-residential segment will reach 3 gigawatts and a valuation of $3.8 billion.

For more information, visit http://www.greentechmedia.com/research/report/us-commercial-solar-landscape-2016-2020.

41

41

15

15

9

9