There's been a wave of positive earning reports from U.S. solar companies, and SolarCity rode that wave in its third-quarter call. SolarCity CEO Lyndon Rive spoke of another "record quarter."

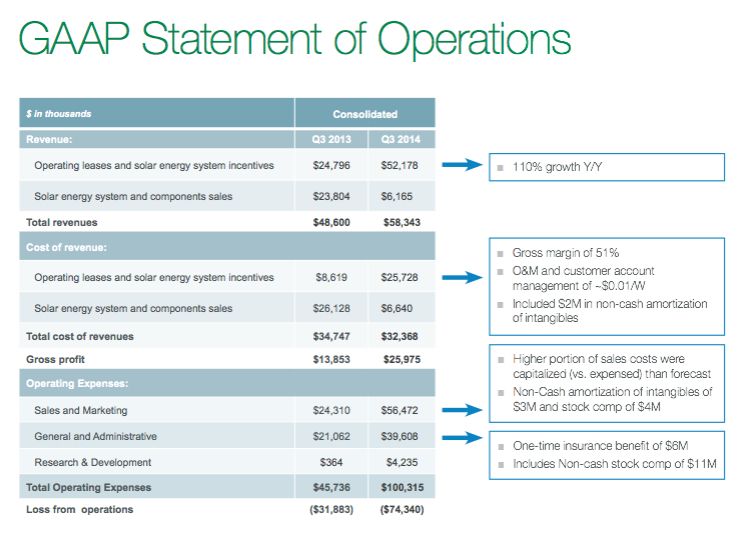

It used to be that one could look at revenue, margin, backlog and costs and get a reasonable idea of the health of a company. With SolarCity, one needs to be a ninja-level forensic accountant.

Q3 financial highlights

-

Retained value: $2.2 billion

-

Bookings: 230 megawatts, up 154 percent year-to-year

-

Deployed: 137 megawatts, up 77 per year-to-year with residential up 100 percent year-to-year

-

Nominal contracted payments remaining up 137 percent year-to-year to $4.1 billion

-

Fifth consecutive quarter of year-over-year revenue gains

New product launches in Q3

-

ZS Peak mounting and installation product for commercial segment

-

ZS Beam carport market product

-

MyPower loan product

-

Solar Bonds product

- ZS Peak mounting and installation product for commercial segment

- ZS Beam carport market product

- MyPower loan product

- Solar Bonds product

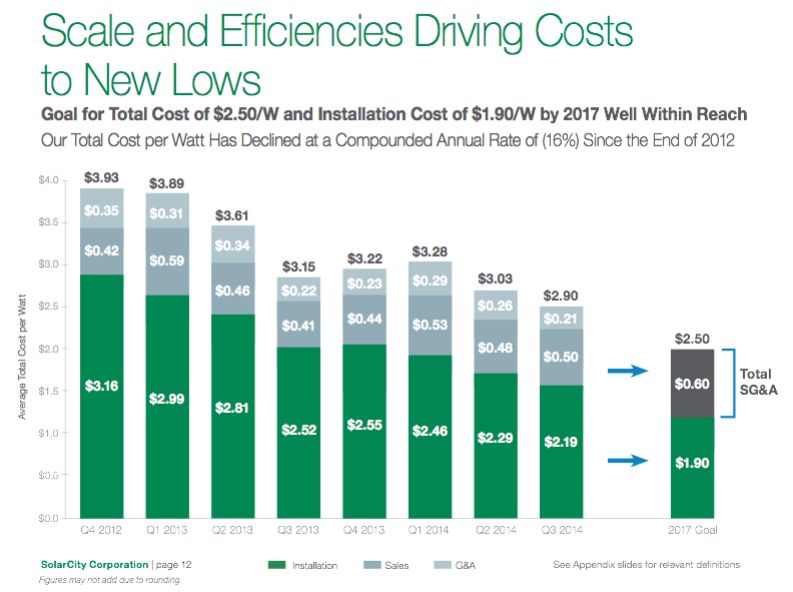

SolarCity's investor letter noted that grading was complete and foundation pre-drilling had begun at the Silevo 1-gigawatt RiverBend factory, with completion targeted for the first quarter of 2016 on "what is expected to be the largest solar manufacturing facility in the Western Hemisphere." SolarCity plans for the factory to be operating at full capacity in 2017. The investor letter also cited "unprecedented demand in the quarter," with residential megawatts deployed up 100 percent year-to-year. Total blended cost dropped 11 percent year-to-year to $2.90 per watt, with a target of $2.50 per watt by 2017.

SolarCity COO Tanguy Serra said, “We are starting to double some really big numbers now.” He noted that market share had grown from 11 percent to 36 percent in less than three years.

Serra noted, "Last quarter, we set ourselves a goal of $1.90 per watt installed cost by 2017. In light of our recent performance, we are ready to reach this number, but we also want to communicate a conservative goal of an all-in cost of $2.50 per watt. As you can see, this assumes marginal reduction costs of acquisition overhead. Jonathan Beamer and the entire marketing and sales organizations are all over transforming how solar is sold at significantly lower cost, and we hope to be able to update this number as our efforts kick in."

With regards to the loss of the 30 percent ITC, Serra said SolarCity's goal is to "ultimately make solar affordable on an unsubsidized basis."

SolarCity CEO Lyndon Rive suggested that loans would be making up an increasingly large portion of overall business and said, "Our residential megawatt installations exceeded the next 50 competitors combined in Q2 2014." He also said loans could reach a run rate of 40 percent to 50 percent of the firm's business in coming quarters.

Canaccord Genuity analyst Josh Baribeau said, “We are...not immediately concerned with fears of lower electricity pricing given the recent energy-related sell-off, or political implications on energy or solar from this week’s election.” Baribeau added, “We are inclined to like SolarCity’s new loan product, as it provides additional visibility to longer-term revenue streams, helps de-risk the tax equity requirements, and can be priced with similar NPV characteristics as the company’s leases/PPAs but will need more color from the company as the product is rolled out.” Baribeau lowered his 2014 and 2015 annual revenue estimates to $254.2 million and $470.2 million, respectively.

Investment bank Baird highlighted SolarCity's "strong bookings, installations at the low end of guidance, tightened-down full-year deployment guidance, and very [slight increase in the] low end of next year’s installation guidance. Although SCTY continued its rapid growth as the leading residential installer in the U.S., we believe shares could face pressure from concerns over the steep ramp needed to meet installation targets and potential pressure on its NPV/MW." The bank added, " Financing innovations continue, but tax-equity capacity could be another metric that causes pressure on shares. SCTY continues to expand its financing arm with products such as MyPower, and will likely continue to raise capital through ABSs. Its tax equity capacity, however, was light at 125 megawatts."

New SolarCity CFO Brad Buss was the more animated participant in today's earnings call. He said, "Buckle up, it's going to be an amazing ride."

Buss continued, "So one of the first questions I get from people is what happens to the business post the planned ITC step-down in 2017. My answer is, it's really business as usual. Pete and Lyndon have built this company from day one on driving to a cost structure that is very profitable -- and more importantly, in a non-incentivized world. As Tanguy has shown you, we have a strong cost discipline, which I'm very grateful for as a CFO. And our target of $2.50 in 2017 will allow us to drive very healthy profits and return through the long run with NPVs greater than $1 per watt. In addition, I think the competition will struggle to be anywhere near this cost target. And more importantly, this overhang that many of you get hung up on will be gone, and you'll be able to model the business in the long term with even greater confidence."

He added, "Retained value is a very strong indicator for the long-term value that we're creating, and it really isn't apparent from reading our financial statements. The Q3 increase in retained value grew 104 percent year-over-year and we ended the quarter with a cumulative value of $2.2 million. The quarterly increases will continue to grow materially each quarter as the law of large numbers and rapid growth work in concert. Go do the math like I did before I joined for the next three to five years, and I think your jaw will drop regardless of the assumptions that you will use."

Buss continued, "And more importantly, we're just in the infancy of a long ride. So if you take a look at the retained value that we're talking about and look at growth rates in the future, it's pretty amazing."

Q4 2014 and 2015 guidance

Guidance for Q4: 179 megawatts to 194 megawatts deployed.

- Operating lease and solar energy systems incentive revenue $47 million to $52 million

- Solar energy systems and component sales revenue $20 million to $24 million

Guidance for 2014: 505 megawatts to 520 megawatts deployed

Guidance for 2015: 920 megawatts to 1,000 megawatts deployed

****

Here are last quarter's highlights, according to the CEO and COO:

-

218 megawatts booked in Q2, a 216 percent jump. Rive said that this volume of bookings wasn't expected until the fourth quarter.

-

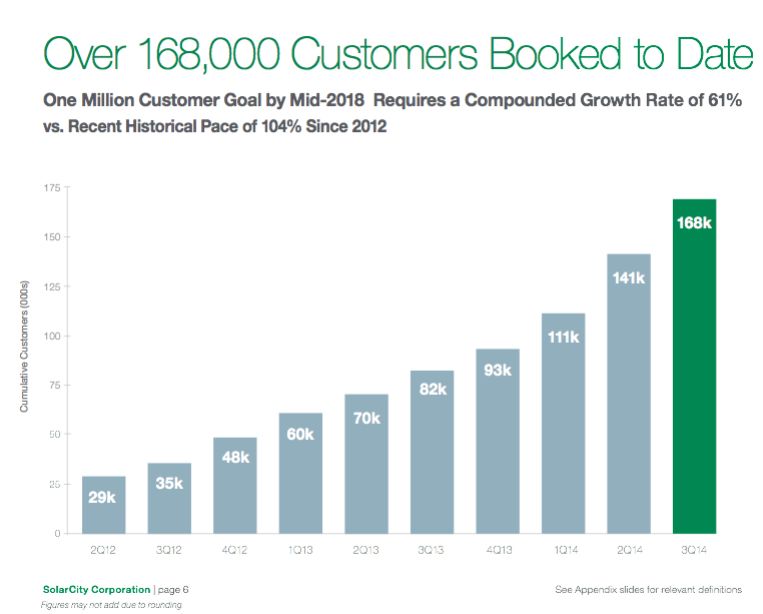

SolarCity "added 30,000 customers in one quarter."

-

The installer/financier grew its Q2 installed capacity to 107 megawatts

-

"The third securitization highlights the depth of available low-cost capital," according to the firm. The third securitization raised $201 million with $160 million at 4.03 percent and was rated BBB+ by S&P.

Rive said that the company has more than "$3.3 billion of customer payments coming to us in the next twenty years. We've added $800 million in one quarter. This growth, and the demand for the product, has really exceeded any of our previous forecasts." He said, "We find ourselves in a very exciting situation," adding, "Now's the time to capture the market and grow as fast as we can."

SolarCity installed 1.2 megawatts of rooftop solar per day "every day of the quarter" in Q2, according to COO Tanguy Serra. He contrasted that to the ten days it used to take SolarCity to install the same 1 megawatt in 2010. He said the 102 percent improvement is due to an "increase in the productivity of our crews." He attributed that improvement to the Zep mounting hardware, more efficient scheduling and more attractive incentive structures.

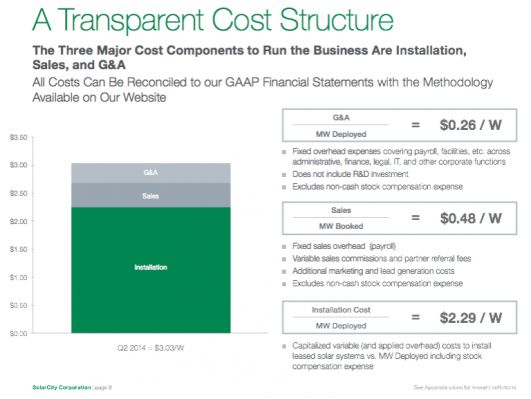

Some good stuff on SolarCity's cost structure from COO Tanguy Serra (prices in dollar per watt)

-

The COO noted that the firm is "reducing cost twice as fast as our goal."

-

"In an effort to increase the transparency of our cost structure, we have reconciled the GAAP numbers from our 10-Q to our unit costs."

-

"On average we spend $2.29 [per watt] to build a solar system -- this includes the panels, the inverters, our proprietary Zep mounting hardware, the balance of system, the labor cost, the call centers, the processing and engineering functions, as well as all the infrastructure, vehicles and warehouses necessary to install a solar asset. So $2.29 installed cost."

-

"We are currently at 48 cents [per watt] acquisition costs."

-

Adding installed cost plus acquisition cost yields $2.77 per watt, "the total marginal cost of growing the asset base."

-

It typically takes less than a day to get a job installed.

-

The goal is to get installation cost down to $1.90 per watt.

-

The company currently has an installation cycle, the time from contract signing to interconnection, of 60 days.

41

41

15

15

9

9