The S-1 IPO Registration Statement for solar electronics builder SolarEdge's $125 million initial public offering has landed. (Renaissance Capital reports the figure at $125 million. Last year, Bloomberg suggested a target of more than $100 million.)

It's a positive (and not unexpected) event for the solar electronics sector and the solar industry as a whole. (We recently named SolarEdge as a company that could make it through the IPO window in 2015 -- here's our recent forecast of IPO hopefuls.)

Founded in 2006, SolarEdge has raised more than $40 million from Norwest Venture Partners, Opus Capital Venture Partners, Walden International, Genesis Partners, Vertex Venture Capital, Lightspeed Venture Partners, ORR Partners, JP Asia Capital Partners and General Electric’s GE Energy Financial Services. One of its largest customers is SolarCity.

SolarEdge takes a different, distributed approach to conditioning the power from rooftop solar modules, and its business is growing rapidly. Atypical of many recent pre-IPO hopefuls, SolarEdge had $5.9 million in profit in the last six months of 2014.

MJ Shiao's list of notable stats from the S-1

GTM's Director of Solar Research has perused the document and extracted some salient stats.

- SolarEdge has shipped 601 megawatts of inverters.

- "The U.S. residential market has really carried SolarEdge full steam ahead, accounting for 72 percent of its revenues."

- In the last six months of 2014, a single customer, identified as "Customer B," accounted for 32.3 percent of the company's revenues. Shiao figures that's in the neighborhood of 125 megawatts and suggests that the only U.S. residential solar installer with that kind of heft is, of course, SolarCity. That's a great customer for SolarEdge -- as well as a lot of exposure to a single player.

SolarEdge at IPO versus already-public Enphase

The leader in the module-level power electronics industry is publicly traded Enphase, which essentially created the microinverter market, and which shipped $105 million in product last quarter.

- SolarEdge has shipped 4.5 million power optimizers and 201,000 inverters. Enphase has shipped more than 7.2 million microinverters but had shipped 1.55 million microinverters when it went public three years ago.

- Shiao notes that SolarEdge is considerably smaller than Enphase -- $139.8 million in revenues for CY 2014 versus Enphase's $343.9 million. But when Enphase went public, it had revenue of $149.5 million in its most recent revenue year.

- Shiao suggests that SolarEdge is "slightly less exposed to the U.S. residential space -- 72 percent versus Enphase's 85 percent. But at this point, both are heavily invested in a U.S. residential market that's growing at a 50 percent year-on-year clip."

- Shiao adds, "We believe that SolarEdge's transition into the commercial space will be smoother. The firm is leveraging the 3-phase string inverter architecture, which is ubiquitous in Europe and is taking off in the U.S., and is able to offset the power optimizer premium through internal savings via its fixed-voltage inverter, as well as with electrical BOS savings via string-stretching."

- In the S-1, SolarEdge suggests that levelized cost of energy (LCOE) is lower for SolarEdge's optimizers, at 8.5 cents per kilowatt-hour versus Enphase at 10.5 cents per kilowatt-hour, in a model of a 90-kilowatt system installation.

Some more key numbers from the SolarEdge S-1

-

SolarEdge shipped 1.3 million power optimizers in fiscal 2014.

-

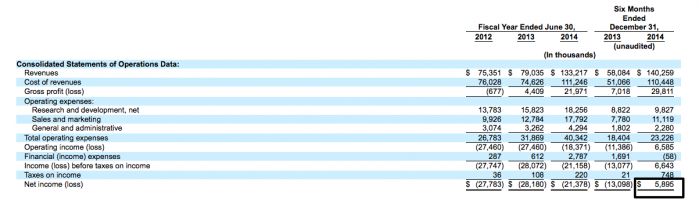

Revenue grew from $58.1 million in the first six months of fiscal 2014 to $140.3 million in the first six months of fiscal 2015.

-

Gross margin increased from 5.6 percent in fiscal 2013 to 16.5 percent in fiscal 2014. GM is 21.3 percent in the first six months of SolarEdge's fiscal 2015.

-

Although the company had net income for the first six months of fiscal 2015 of $5.9 million, the VC-funded startup has an accumulated deficit of $135.2 million and incurred net losses of $28.2 million in fiscal 2013 and $21.4 million in fiscal 2014.

MJ Shiao notes, "A successful IPO would give SolarEdge a significant war chest to tackle traditional inverter manufacturers weakened by European market woes and global pricing pressure. In the past year, SolarEdge has gained tremendous traction in the U.S. residential market, where its market share was 26 percent in the third quarter of 2014 according to GTM Research's latest U.S. PV Leaderboard." Shiao added, "SolarEdge will have to go head-to-head with Enphase, which is still fresh from a record quarter and year, as well as ABB, SMA and newcomers to the module-level power electronics (MLPE) space like LG."

He continued, "Globally, we see a huge opportunity for MLPE, growing from less than 4 percent of global annual inverter shipments in 2014 to more than 11 percent by 2018. In 2015, we expect total combined MLPE shipments to well exceed 2 gigawatts. Furthermore, we expect the U.S. residential market to continue growing at 50 percent to 55 percent year-over-year ahead of the federal Investment Tax Credit cliff in 2017 -- a strong foundation and growth opportunity for MLPE vendors."

41

41

15

15

9

9